🏗️ Structured Finance Options

Structured finance concepts, securitization, SPE, bankruptcy remoteness, SF products (syndicated loans, CDOs, CBOs, CLOs, CDS, TRS, hybrid securities, CMOs, synthetic instruments), returns distribution, and risks.

Structured Finance Options

Introduction

- Conventional loan products like cash credit or term loans have been prevalent in banking for a long time.

- However, the modern world demands more unique financing solutions to match unique borrower needs.

- Structured Finance (SF) is a contemporary approach to financing tailored to specific borrower requirements.

- SF focuses on creating customized structures rather than just securitizing receivables.

- It aims to diminish risk by designing financing solutions that are non-flow in nature.

- SF structures are designed to mitigate inherent risks and sometimes transfer them altogether.

Structured Finance Explained

- Securitization is central to structured finance, allowing the creation of asset pools and complex financial instruments.

Key Terminologies

| Term | Meaning |

|---|---|

| Special Purpose Entity (SPE) | An entity organized for a specific purpose, isolated from the credit risk of the originator |

| Originator | A lender transferring assets to an SPE as part of a securitization transaction |

| Securitization | Transferring a pool of assets to an SPE, with cash flows used to service securitization exposures of different tranches |

| Securitization Exposures | Various financial instruments like asset-backed securities, mortgage-backed securities, credit enhancements, etc. |

| Mortgage-backed Securities | Securitization notes backed by real estate mortgages |

| Credit Enhancement Facilities | Enhance the credit profile of structured financial transactions by providing additional security or financial support to cover losses on securitized assets |

| Derivative | Financial instrument settled in the future, deriving value from changes in interest rates, exchange rates, credit ratings, securities prices, or a combination |

| Interest Rate Swap | Derivative where two parties exchange future interest payments on a notional principal amount over a specified period |

| Currency Swap | Derivative where two parties exchange streams of interest payments and/or principal amounts in different currencies at a pre-agreed exchange rate |

- Additional details can be found in the Master Direction issued by RBI.

Nature of Structured Finance Products

- SF offers structured methods for borrowers and lenders to achieve timely finance with minimal risk, enabling financing solutions without free cash flow and addressing diverse asset classes.

- SF products originated in Europe in the mid-1980s, later gaining popularity in the United States and becoming accessible to retail investors.

- SF typically involves multiple optional transactions to fulfill financing needs and mitigate risks.

- SF products are complex and involve higher-than-ordinary risk levels, making them difficult to understand.

- They were made accessible to retail investors through official platforms in regulated ecosystems.

- SF products act as a link between common investors and otherwise inaccessible asset classes.

- These investments are pre-wrapped or pre-packaged, often comprising assets linked to interest and derivatives.

- SFs are designed to tightly tailor risk-return objectives by substituting traditional bond characteristics with non-traditional payoffs derived from underlying assets.

- They are called non-cash flow-based financial solutions because they derive payoffs from asset performance rather than issuer cash flow.

Importance of Structured Finance

- SF involves corporate entities, business conglomerates, financial institutions, and banks.

- It deals with enormous amounts of money, impacting the larger economy.

- SF plays a significant role in restructuring large debts through non-cash-flow-based instruments.

- SF products are used to save on repayment by decoupling cash flow from underlying obligations.

- They free up cash flow for more effective use in working capital needs.

- SF is particularly beneficial for organizations with global operations and diverse business interests.

Advantages of Structured Finance

- SF investors face limitations in interchanging between different types of debt compared to standard loans — this creates risk unbundling.

- Borrowers increasingly utilize SF products for risk management, market development, and expanding business reach.

- SF initiatives contribute to designing new funding instruments for emerging markets.

- Investors experience risk unbundling when engaging in structured financing.

- SF transforms cash flows and reshapes the liquidity of financial portfolios.

- Risks are transferred from sellers to buyers of structured products, and specific assets are removed from balance sheets through packaging.

SF and Securitization

- Structured finance utilizes securitization to create asset pools for sale.

- These asset pools are used to construct complex financial instruments.

- These instruments cater to borrowers and investors with unique requirements.

1. Debtor-Creditor Relationship

- Securitization allows lenders to transfer risk.

- The debtor-creditor relationship between borrower and original lender remains unchanged.

- Borrowers continue to make repayments to the originator.

- Borrowers may not be aware of the transfer of risk.

2. Bankruptcy Remoteness Clause

- "Bankruptcy remote" means unlikely to face bankruptcy proceedings.

- Originator's insolvency doesn't affect repayment obligations.

- Repayment obligations are escrowed to the SPV.

- Pass-Through Certificates are insulated from originator's bankruptcy.

- Mitigates solvency risk for investors.

- Ring-fencing mechanism of cash flows is called bankruptcy remoteness.

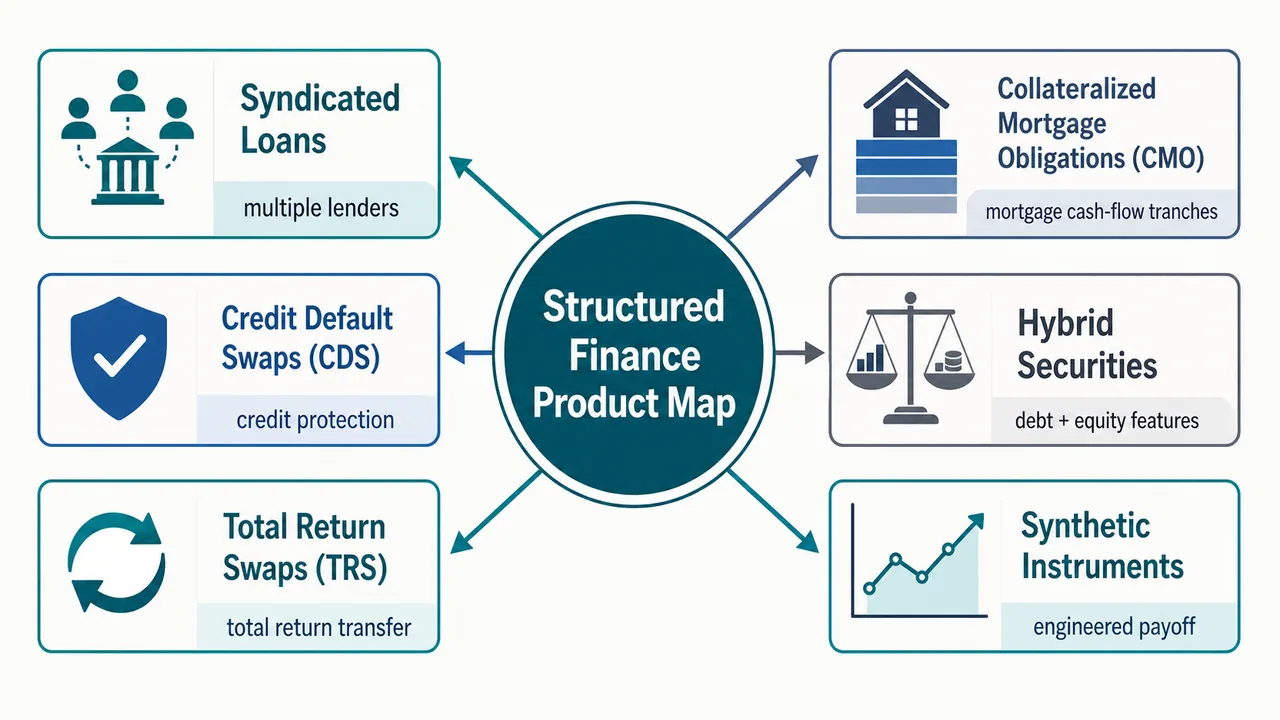

Different Structured Finance Products

a. Syndicated Loans

- Syndicated loans are credit facilities for large, high-cost projects.

- They involve multiple lenders sanctioning loans to a single borrower.

- Syndicates comprise banks, financial institutions, insurance companies, etc.

- Lenders can sell all or part of their share of the loan.

- Secondary markets exist in some countries for trading syndicated loan shares.

- Syndicated loans are not specifically identified in lenders' accounts and are part of their regular loan portfolios.

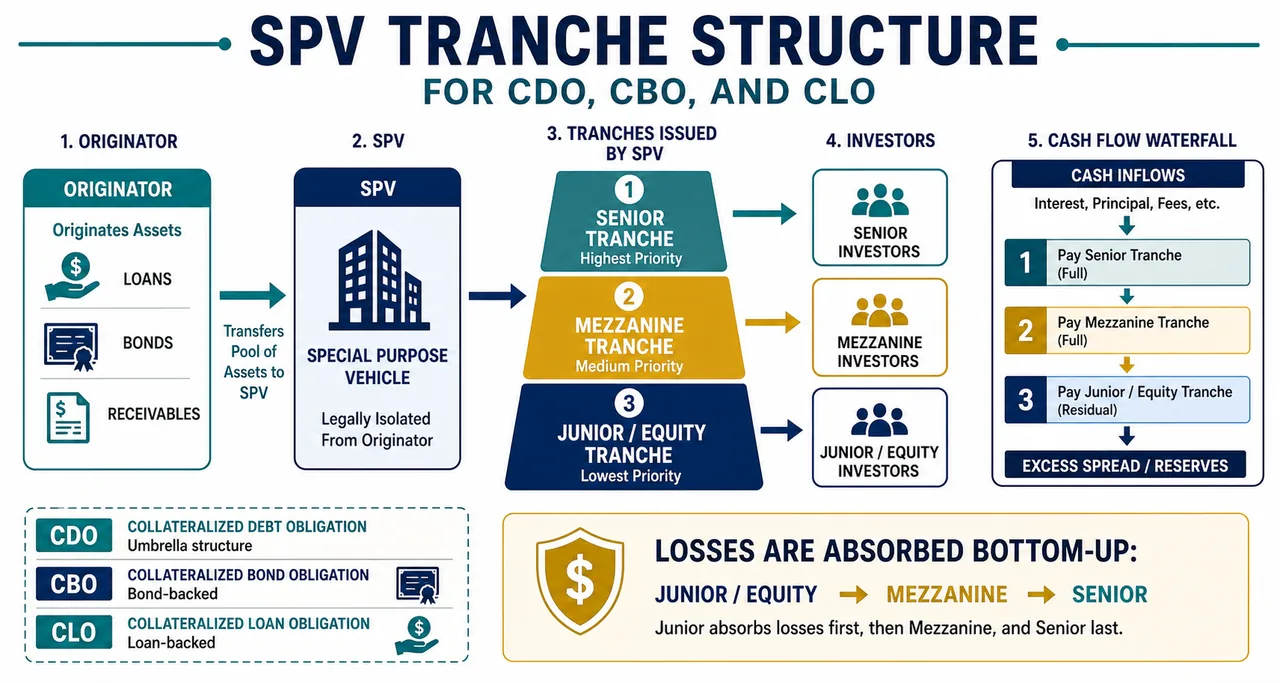

b. Collateralized Debt Obligations (CDOs)

- CDOs are repackaged offerings containing a substantial credit portfolio.

- Both CDOs and repackaged offerings involve debt issuance by a Special Purpose Vehicle (SPV).

- In repackaging, all risk from underlying collateral is transferred to investors.

- CDOs split risk horizontally, categorizing investors into senior, mezzanine, and junior debt.

- CDOs may have additional classifications based on funding structure.

c. Collateralized Bond Obligations / Collateralized Loan Obligations

- Collateralized Bond Obligations (CBOs) involve raising funds through bond issuance.

- Collateralized Loan Obligations (CLOs) involve raising funds through loans.

CDO/CBO/CLO Ecosystem

The flow works as follows:

🔐

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

Pro

Popular Save ₹100/mo

₹ 99 /mo

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Structured Finance Options

Introduction

- Conventional loan products like cash credit or term loans have been prevalent in banking for a long time.

- However, the modern world demands more unique financing solutions to match unique borrower needs.

- Structured Finance (SF) is a contemporary approach to financing tailored to specific borrower requirements.

- SF focuses on creating customized structures rather than just securitizing receivables.

- It aims to diminish risk by designing financing solutions that are non-flow in nature.

- SF structures are designed to mitigate inherent risks and sometimes transfer them altogether.

Structured Finance Explained

- Securitization is central to structured finance, allowing the creation of asset pools and complex financial instruments.

Key Terminologies

| Term | Meaning |

|---|---|

| Special Purpose Entity (SPE) | An entity organized for a specific purpose, isolated from the credit risk of the originator |

| Originator | A lender transferring assets to an SPE as part of a securitization transaction |

| Securitization | Transferring a pool of assets to an SPE, with cash flows used to service securitization exposures of different tranches |

| Securitization Exposures | Various financial instruments like asset-backed securities, mortgage-backed securities, credit enhancements, etc. |

| Mortgage-backed Securities | Securitization notes backed by real estate mortgages |

| Credit Enhancement Facilities | Enhance the credit profile of structured financial transactions by providing additional security or financial support to cover losses on securitized assets |

| Derivative | Financial instrument settled in the future, deriving value from changes in interest rates, exchange rates, credit ratings, securities prices, or a combination |

| Interest Rate Swap | Derivative where two parties exchange future interest payments on a notional principal amount over a specified period |

| Currency Swap | Derivative where two parties exchange streams of interest payments and/or principal amounts in different currencies at a pre-agreed exchange rate |

- Additional details can be found in the Master Direction issued by RBI.

Nature of Structured Finance Products

- SF offers structured methods for borrowers and lenders to achieve timely finance with minimal risk, enabling financing solutions without free cash flow and addressing diverse asset classes.

- SF products originated in Europe in the mid-1980s, later gaining popularity in the United States and becoming accessible to retail investors.

- SF typically involves multiple optional transactions to fulfill financing needs and mitigate risks.

- SF products are complex and involve higher-than-ordinary risk levels, making them difficult to understand.

- They were made accessible to retail investors through official platforms in regulated ecosystems.

- SF products act as a link between common investors and otherwise inaccessible asset classes.

- These investments are pre-wrapped or pre-packaged, often comprising assets linked to interest and derivatives.

- SFs are designed to tightly tailor risk-return objectives by substituting traditional bond characteristics with non-traditional payoffs derived from underlying assets.

- They are called non-cash flow-based financial solutions because they derive payoffs from asset performance rather than issuer cash flow.

Importance of Structured Finance

- SF involves corporate entities, business conglomerates, financial institutions, and banks.

- It deals with enormous amounts of money, impacting the larger economy.

- SF plays a significant role in restructuring large debts through non-cash-flow-based instruments.

- SF products are used to save on repayment by decoupling cash flow from underlying obligations.

- They free up cash flow for more effective use in working capital needs.

- SF is particularly beneficial for organizations with global operations and diverse business interests.

Advantages of Structured Finance

- SF investors face limitations in interchanging between different types of debt compared to standard loans — this creates risk unbundling.

- Borrowers increasingly utilize SF products for risk management, market development, and expanding business reach.

- SF initiatives contribute to designing new funding instruments for emerging markets.

- Investors experience risk unbundling when engaging in structured financing.

- SF transforms cash flows and reshapes the liquidity of financial portfolios.

- Risks are transferred from sellers to buyers of structured products, and specific assets are removed from balance sheets through packaging.

SF and Securitization

- Structured finance utilizes securitization to create asset pools for sale.

- These asset pools are used to construct complex financial instruments.

- These instruments cater to borrowers and investors with unique requirements.

1. Debtor-Creditor Relationship

- Securitization allows lenders to transfer risk.

- The debtor-creditor relationship between borrower and original lender remains unchanged.

- Borrowers continue to make repayments to the originator.

- Borrowers may not be aware of the transfer of risk.

2. Bankruptcy Remoteness Clause

- "Bankruptcy remote" means unlikely to face bankruptcy proceedings.

- Originator's insolvency doesn't affect repayment obligations.

- Repayment obligations are escrowed to the SPV.

- Pass-Through Certificates are insulated from originator's bankruptcy.

- Mitigates solvency risk for investors.

- Ring-fencing mechanism of cash flows is called bankruptcy remoteness.

Different Structured Finance Products

a. Syndicated Loans

- Syndicated loans are credit facilities for large, high-cost projects.

- They involve multiple lenders sanctioning loans to a single borrower.

- Syndicates comprise banks, financial institutions, insurance companies, etc.

- Lenders can sell all or part of their share of the loan.

- Secondary markets exist in some countries for trading syndicated loan shares.

- Syndicated loans are not specifically identified in lenders' accounts and are part of their regular loan portfolios.

b. Collateralized Debt Obligations (CDOs)

- CDOs are repackaged offerings containing a substantial credit portfolio.

- Both CDOs and repackaged offerings involve debt issuance by a Special Purpose Vehicle (SPV).

- In repackaging, all risk from underlying collateral is transferred to investors.

- CDOs split risk horizontally, categorizing investors into senior, mezzanine, and junior debt.

- CDOs may have additional classifications based on funding structure.

c. Collateralized Bond Obligations / Collateralized Loan Obligations

- Collateralized Bond Obligations (CBOs) involve raising funds through bond issuance.

- Collateralized Loan Obligations (CLOs) involve raising funds through loans.

CDO/CBO/CLO Ecosystem

The flow works as follows:

- Loan / RMBS / Asset → transferred to SPV

- SPV issues Note to Investors (Senior, Mezzanine, Junior classes)

- Administration / Trustee / Servicer manages the structure

- Swap Counterparty provides hedging

- Cash proceeds flow from SPV to originator; principal and interest flow from SPV to investors

d. Credit Default Swaps (CDS)

- CDS is a derivative contract involving two parties: the Protection Buyer and the Protection Seller.

- The Protection Buyer pays a fee (premium) throughout the contract's life.

- The Protection Seller provides a credit event payment if a credit-default event occurs.

- The Protection Buyer typically makes quarterly payments to the Protection Seller, expressed in annualized basis points of the transaction's notional amount.

- If no credit event occurs, the Protection Seller receives periodic payments as compensation for assuming credit risk.

- If a credit event happens, the Protection Buyer receives a credit event payment based on whether the contract calls for physical or cash settlement.

- The legal structure and documentation of a CDS are based on ISDA standards.

Settlement Types

| Type | Mechanism |

|---|---|

| Physical Settlement | Protection Buyer delivers the Deliverable Obligations to the Protection Seller for a pre-agreed amount |

| Cash Settlement | Protection Seller pays the Protection Buyer the difference between face value and market value of the Deliverable Obligations |

- Market value of Deliverable Obligations is determined based on ISDA guidelines or terms specified in the confirmation document.

- Alternatively, a pre-determined amount agreed upon by both parties may be paid at the start of the transaction.

e. Total Return Swaps (TRS)

- Total Return Swaps (TRS), also known as Total Rate of Return Swaps (TROR), are bilateral financial contracts.

- TRS aims to replicate the monetary returns of an underlying asset or portfolio for a predetermined period.

- One counterparty (TR payer) pays the total return of a specified asset to the other counterparty (TR receiver), who makes regular variable payments in return.

- TRS allows the TR receiver to gain financial returns without holding the assets on its balance sheet.

- If the underlying asset's value declines beyond the coupon payment, the TR receiver must pay the negative total return and funding cost to the TR payer.

- TRS is an off-balance sheet financing tool, unlike credit default swaps.

- TRS transfers both credit risk (issuer's credit quality movements) and market risk (general market price instabilities).

- Payments in TRS occur upon credit events and changes in the market valuation of the underlying, similar to CDS contracts.

f. Hybrid Securities

- A hybrid security combines features from multiple financial instruments into one.

- Convertible debentures are a common example of hybrid securities.

- They possess characteristics of both debt (like a bond) and equity (like a stock).

- While resembling a bond, they are affected by the price fluctuations of the stock they can be converted into.

g. Collateralized Mortgage Obligations (CMOs)

- CMO is a type of mortgage-backed security.

- It consists of a pool of mortgage loans packaged together and sold as investments.

- The loans are primarily secured by immovable assets like houses.

- CMOs receive cash flows from borrowers' loan repayments, which act as collateral.

- Investors receive principal and interest payments based on agreed terms and conditions.

h. Synthetic Financial Instruments

- Synthetic Financial Instruments are created to fulfill needs not met by conventional instruments.

- They aim to minimize risk, maximize diversification, and offer higher returns.

- Examples include:

- Combining a fixed-rate bond with an interest rate swap to create a synthetic floating rate instrument.

- Purchasing a call option and simultaneously selling a put option on the same share to create an asset with similar risks and rewards as the underlying share.

Returns Distribution

- SF product returns are typically paid by issuers upon maturity.

- Pay-offs depend on actual returns, with amounts determined accordingly.

- Structured products are modeled similarly to traditional options pricing but include various derivatives like futures, forwards, and swaps.

- They may also feature upside leverages or downside buffers.

Risks Involved in Structured Finance

- Liquidity Risk: Customized SF products often lack liquidity, posing a common risk.

- Complexity Risk: SFs typically offer complex performance features, making frequent entry and exit impractical.

- Time Horizon Risk: Longer time horizons associated with SFs entail higher risk.

- Understanding Risk: Complexity of SF products makes them challenging for lay investors to understand.

- Issuer Credit Risk: SFs are liabilities of the issuer until maturity, exposing investors to issuer's financial position and credit quality.

- Loss Risk: During economic downturns, SFs can result in partial or full loss of original investment, akin to options risks.

- Transparency Risk: Lack of transparency hinders the development of uniform pricing standards, complicating market comparison.

- Embedded Pricing Risk: Some SF issuers embed pricing into option structures in a non-transparent manner, obscuring fees from investors.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Structured Finance | Customized financing tailored to specific borrower requirements |

| Nature | Non-cash flow-based; payoffs from asset performance |

| Origin | Europe, mid-1980s; later popular in USA |

| SPE | Special Purpose Entity — isolated from originator's credit risk |

| Originator | Lender transferring assets to SPE |

| Securitization | Pooling assets into SPE; cash flows service different tranches |

| Credit Enhancement | Additional security/support to cover losses on securitized assets |

| Bankruptcy Remoteness | SPV insulated from originator's insolvency; PTCs protected |

| Debtor-Creditor | Relationship unchanged after securitization |

| Syndicated Loans | Multiple lenders → single borrower; for large projects |

| CDOs | Repackaged credit portfolio via SPV; risk split into senior/mezzanine/junior |

| CBOs | CDO variant — funds raised through bond issuance |

| CLOs | CDO variant — funds raised through loans |

| CDS | Protection Buyer pays premium; Seller pays on credit event |

| CDS Settlement | Physical (deliver obligations) or Cash (pay difference) |

| CDS Documentation | Based on ISDA standards |

| CDS Payments | Quarterly; expressed in annualized basis points |

| TRS (TROR) | TR payer pays total return; TR receiver pays variable amounts |

| TRS Nature | Off-balance sheet; transfers both credit & market risk |

| TRS vs CDS | TRS transfers market risk too; CDS only credit risk |

| Hybrid Securities | Combine debt + equity features (e.g., convertible debentures) |

| CMOs | Pool of mortgage loans; secured by immovable assets |

| Synthetic Instruments | Created for needs unmet by conventional instruments |

| Synthetic Example | Fixed bond + IRS = synthetic floating rate instrument |

| Returns | Paid upon maturity; based on actual returns |

| Pricing Model | Similar to options pricing; includes futures, forwards, swaps |

| Risk — Liquidity | Customized products often lack liquidity |

| Risk — Complexity | Complex features; difficult entry/exit |

| Risk — Time | Longer horizons → higher risk |

| Risk — Issuer Credit | SF is issuer's liability until maturity |

| Risk — Loss | Partial/full loss possible in economic downturns |

| Risk — Transparency | No uniform pricing standards; non-transparent fee embedding |

Lesson Doubts

Ask questions, get expert answers