📈 Derivatives

introduction to Derivatives.

Derivatives

Derivatives are among the most important financial instruments used by banks, corporations, and investors for managing risk. Understanding derivatives is essential for banking exams as they appear in questions related to forex, treasury operations, and risk management.

Definition & Concept

-

Derivatives are financial instruments that:

- Are settled in the future (not immediately like spot transactions).

- Derive their value from some underlying variable (stock index, forex rate, commodity price, interest rate, etc.).

-

Purpose: Primarily used to hedge (protect against) risk. For example, an importer can lock in future exchange rates to protect against currency fluctuations. However, derivatives can also be used for speculation (betting on price movements) and arbitrage (exploiting price differences).

-

Example: Understanding the "Derivative" Concept

- Spot Rate: 1 USD = Rs. 89.10 (today's rate)

- Forward Rate (Spot + Premium): 89.10 + 0.50 = Rs. 89.60 (rate for future delivery)

- The Forward rate derives its value from the Spot rate. If the Spot rate changes, the Forward rate will also change. Hence, a forward contract is a derivative.

Market Structure

Derivatives can be traded in two types of markets:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Derivatives

Derivatives are among the most important financial instruments used by banks, corporations, and investors for managing risk. Understanding derivatives is essential for banking exams as they appear in questions related to forex, treasury operations, and risk management.

Definition & Concept

-

Derivatives are financial instruments that:

- Are settled in the future (not immediately like spot transactions).

- Derive their value from some underlying variable (stock index, forex rate, commodity price, interest rate, etc.).

-

Purpose: Primarily used to hedge (protect against) risk. For example, an importer can lock in future exchange rates to protect against currency fluctuations. However, derivatives can also be used for speculation (betting on price movements) and arbitrage (exploiting price differences).

-

Example: Understanding the "Derivative" Concept

- Spot Rate: 1 USD = Rs. 89.10 (today's rate)

- Forward Rate (Spot + Premium): 89.10 + 0.50 = Rs. 89.60 (rate for future delivery)

- The Forward rate derives its value from the Spot rate. If the Spot rate changes, the Forward rate will also change. Hence, a forward contract is a derivative.

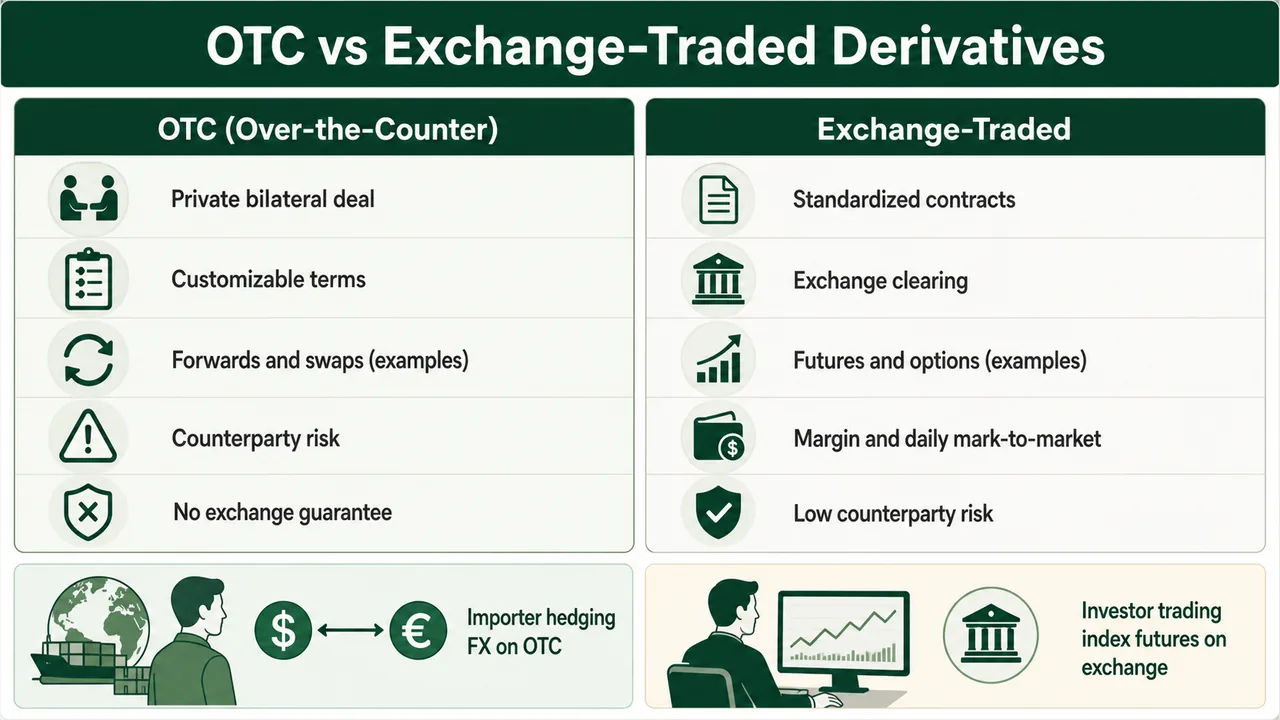

Market Structure

Derivatives can be traded in two types of markets:

-

Over the Counter (OTC):

- Private dealings between two parties directly (no exchange involvement).

- Customizable—parties can negotiate terms (amount, date, price).

- Examples: Forwards, Swaps.

- Counterparty Risk: Since there's no exchange guarantee, there's a risk that one party may default.

-

Exchange Traded:

- Standardized contracts traded on recognized exchanges (NSE, BSE).

- The exchange acts as the counterparty to both buyer and seller, eliminating counterparty risk.

- Examples: Futures (e.g., Nifty Futures, Reliance Futures on NSE), Options.

- Requires margin deposits and has daily settlement (Mark-to-Market).

Types of Derivatives

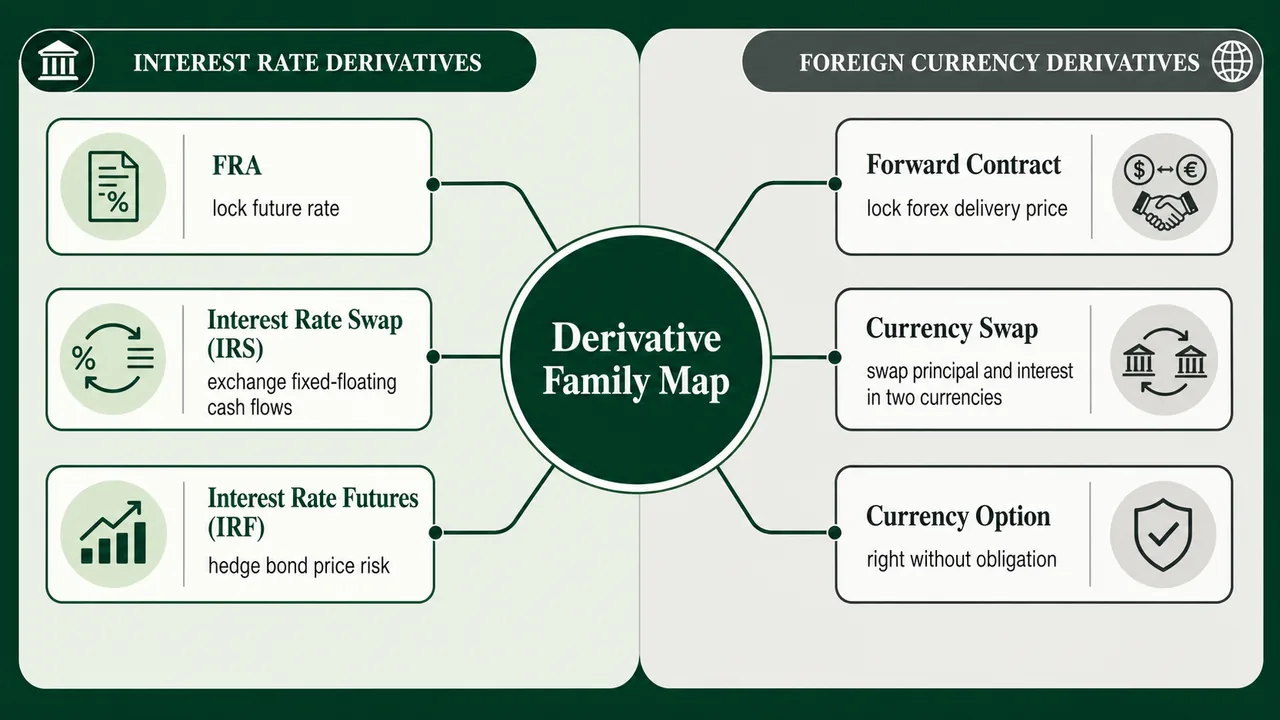

A. Interest Rate Derivatives

These derivatives help manage interest rate risk—the risk that changes in interest rates will affect the value of assets/liabilities or cash flows.

-

Forward Rate Agreement (FRA):

- A contract between two parties to exchange interest payment for a notional principal amount, on a single settlement date, for a specified period.

- How it works: Parties agree today on an interest rate to be applied on a future date. On settlement, only the cash difference is exchanged (no actual principal changes hands).

- Use Case: A company expecting to borrow ₹10 crore in 3 months can lock in today's interest rate using an FRA.

-

Interest Rate Swaps (IRS):

- A contract between two parties to exchange streams of interest payments for a notional amount, on multiple occasions (e.g., quarterly), during a specified period.

- Common Type: "Fixed-for-Floating" swap—one party pays a fixed rate, the other pays a floating rate (linked to MIBOR/SOFR).

- Use Case: A bank with floating-rate deposits and fixed-rate loans can use IRS to convert its fixed receipts to floating, matching its liability structure.

Example: Understanding Interest Rate Swap

The Scenario:

- State Bank of India (SBI) has given a loan of ₹100 crore at a fixed rate of 10% (earns ₹10 crore/year)

- SBI's deposits are linked to MIBOR (floating rate), currently at 8% (pays ₹8 crore/year)

- Problem: If MIBOR rises to 12%, SBI pays ₹12 crore but still earns only ₹10 crore → Loss!

The Solution: Enter into an IRS

- SBI enters a swap with ICICI Bank for a notional principal of ₹100 crore

- Swap Terms:

- SBI pays ICICI a fixed 9% (₹9 crore/year)

- ICICI pays SBI a floating rate (MIBOR) (currently ₹8 crore/year)

How the Cash Flows Work (Quarterly Settlements):

| Quarter | MIBOR Rate | SBI Receives from ICICI | SBI Pays to ICICI | Net Payment |

|---|---|---|---|---|

| Q1 | 8% | ₹2 cr | ₹2.25 cr | SBI pays ₹0.25 cr |

| Q2 | 9% | ₹2.25 cr | ₹2.25 cr | No exchange |

| Q3 | 11% | ₹2.75 cr | ₹2.25 cr | SBI receives ₹0.50 cr |

| Q4 | 12% | ₹3 cr | ₹2.25 cr | SBI receives ₹0.75 cr |

Result:

- When MIBOR rises, SBI receives more from the swap, offsetting its higher deposit costs

- SBI has effectively converted its fixed-rate loan income into floating-rate income that moves with its floating-rate liabilities

- Risk is hedged! No matter what happens to MIBOR, SBI's margin is protected

Key Points:

- The ₹100 crore principal is never exchanged—it's just a reference ("notional") for calculating interest

- Only the net difference is settled each quarter

- Both parties benefit: SBI hedges risk, ICICI Bank earns a spread

- Interest Rate Futures (IRF):

- A standardized, exchange-traded contract with actual or notional interest-bearing instruments (like G-Secs or T-Bills) as the underlying asset.

- Unlike FRA/IRS (which are OTC), IRF is traded on exchanges with daily MTM settlement.

- Use Case: Banks can hedge their G-Sec portfolio against interest rate movements.

Example: Understanding Interest Rate Futures

The Scenario:

- Punjab National Bank (PNB) holds ₹500 crore of 10-year Government Securities (G-Secs) with a coupon rate of 7%

- PNB is concerned that RBI may hike interest rates in the upcoming policy meeting

- If rates rise, bond prices will fall, causing MTM losses on PNB's AFS/HFT portfolio

The Solution: Sell IRF on NSE

- PNB decides to sell IRF contracts on NSE to hedge its G-Sec portfolio

- Underlying: 10-year G-Sec Futures

- Contract size: ₹2 lakh face value per lot

- PNB sells 2,500 lots (₹500 crore ÷ ₹2 lakh = 2,500 contracts)

- Current futures price: ₹102 (G-Sec trading at premium)

What Happens When RBI Hikes Rates:

| Event | G-Sec Portfolio | IRF Position | Net Effect |

|---|---|---|---|

| Before Rate Hike | Value: ₹510 cr | Sold at ₹102 | — |

| After Rate Hike (+0.5%) | Value drops to ₹490 cr (Loss ₹20 cr) | Futures price falls to ₹98, PNB buys back (Profit ₹20 cr) | Hedged! |

How the Hedge Works:

- When interest rates rise, G-Sec prices fall

- Since PNB sold futures, falling prices mean PNB can buy back cheaper → Profit

- The profit on futures offsets the loss on the actual G-Sec portfolio

Key Differences from IRS:

| Feature | IRS | IRF |

|---|---|---|

| Trading | OTC (private deal) | Exchange (NSE) |

| Counterparty Risk | Yes | No (exchange guarantee) |

| Settlement | Periodic cash flows | Daily MTM |

| Standardization | Customizable | Fixed contract size |

Why Banks Use IRF:

- No counterparty risk (exchange guaranteed)

- Easy to enter and exit positions

- Transparent pricing

- Useful for hedging large G-Sec portfolios quickly

B. Foreign Currency Derivatives

These derivatives help manage currency/forex risk—the risk arising from exchange rate fluctuations.

1. Foreign Exchange Forward

- A contract between two parties where the buyer agrees to purchase and the seller agrees to sell a fixed amount of foreign currency to be delivered at a future date, at a pre-agreed rate.

- OTC Contract: Customizable terms (amount, date, rate).

- Delivery is mandatory on the settlement date.

- Use Case: An importer who has to pay $1 million in 3 months can book a forward contract today at ₹85/USD to lock in the rate, protecting against rupee depreciation.

2. Currency Swaps

- An interest rate swap where the two streams of payments are in different currencies.

- In addition to exchanging interest payments, the parties may also agree to swap the principal amounts at the beginning and end of the contract at pre-agreed rates.

- Use Case: An Indian company with USD borrowings but INR revenues can swap its USD interest payments to INR payments, reducing currency mismatch.

Example: Currency Swap — Tata Motors & HDFC Bank

The Scenario:

- Tata Motors raised a $100 million loan from a foreign bank at 5% USD interest for 5 years

- Tata Motors earns revenues primarily in INR (from domestic car sales)

- Problem: Every year, Tata needs to pay $5 million interest in USD. If the rupee depreciates from ₹80 to ₹90, the cost in INR increases significantly!

The Solution: Currency Swap with HDFC Bank

| At Start (Day 1) |

|---|

| Tata gives $100 million to HDFC Bank |

| HDFC Bank gives ₹8,000 crore to Tata (at ₹80/USD) |

| Every Year (Interest Payments) |

|---|

| Tata pays HDFC Bank: ₹640 crore (8% on ₹8,000 cr) |

| HDFC Bank pays Tata: **100M) |

| Tata uses the $5M received to pay its foreign lender |

| At Maturity (Year 5) |

|---|

| Tata returns ₹8,000 crore to HDFC Bank |

| HDFC Bank returns $100 million to Tata |

| Tata repays the $100M to its foreign lender |

Result:

- Tata's loan effectively becomes an INR loan at 8% instead of a USD loan

- Currency risk eliminated! Even if USD rises to ₹100, Tata's payments remain fixed in INR

- HDFC Bank earns 3% spread (receives 8% INR, pays 5% USD)

Key Points:

- Both principal and interest are swapped

- Exchange rate is locked at the start (₹80/USD in this case)

- Tata gets certainty in its cash flows

3. Currency Options

- A contract giving the buyer the right (but not the obligation) to buy or sell an agreed amount of foreign currency at a pre-agreed rate (strike price).

- The buyer pays a premium (fee) to the seller to acquire this right.

- Use Case: An exporter expecting $1 million in 3 months can buy a Put option to sell USD at ₹85. If the rate falls to ₹82, the exporter exercises the option and still gets ₹85. If the rate rises to ₹88, the exporter doesn't exercise and sells in the spot market at ₹88.

What are Options?

Options are unique derivatives that provide asymmetric payoff—the buyer's loss is limited to the premium paid, but profit potential is unlimited.

- An Option is a right purchased by the buyer to buy or sell a pre-fixed quantity, at a pre-determined price (strike price), during a pre-fixed period (expiry).

- No obligation to exercise—the buyer can choose whether or not to use the right.

- Option Seller (Writer): Undertakes the obligation to buy or sell if the buyer exercises.

- Option Buyer: Obtains the right to buy or sell by paying a fee (premium).

Example: Call Option on Reliance Industries

The Players:

- Priya (Retail Investor) — Option Buyer

- Zerodha Trading Desk — Option Seller (Writer)

- Underlying: 1000 shares of Reliance Industries

The Trade:

- Priya is bullish on Reliance (currently trading at ₹1,150)

- She buys a Call Option on NSE with:

- Strike Price: ₹1,200

- Expiry: 31st December 2024

- Lot Size: 250 shares × 4 lots = 1000 shares

- Premium: ₹20 per share (Total: ₹20,000)

What Priya Gets:

- The right to buy 1000 Reliance shares at ₹1,200 anytime before expiry

| Scenario | Reliance Price at Expiry | Priya's Action | Profit/Loss |

|---|---|---|---|

| Bullish | ₹1,500 | Exercises option, buys at ₹1,200, sells at ₹1,500 | (₹1,500 - ₹1,200) × 1000 = ₹3,00,000 Minus Premium: ₹2,80,000 Profit ✅ |

| Neutral | ₹1,220 | Exercises option (still ITM) | (₹1,220 - ₹1,200) × 1000 = ₹20,000 Minus Premium: Break-even |

| Bearish | ₹1,000 | Does NOT exercise (why buy at ₹1,200?) | ₹20,000 Loss (only premium) ❌ |

Key Insight:

- Maximum Loss for Priya: ₹20,000 (the premium paid) — even if Reliance falls to ₹0

- Maximum Profit: Unlimited — the higher Reliance goes, the more she earns

- Risk-Reward: Asymmetric — limited downside, unlimited upside

Types of Options

| Type | Description |

|---|---|

| American Option | Can be exercised any time before or on the expiry date |

| European Option | Can be exercised only on the expiry date. In India, all stock/index options are European. |

| Call Option | Right to buy the underlying asset |

| Put Option | Right to sell the underlying asset |

Moneyness of Options:

| Status | Meaning | Example (Call at ₹100 strike) |

|---|---|---|

| In the Money (ITM) | Buyer gains by exercising | Stock at ₹120 (buy at ₹100, gain ₹20) |

| At the Money (ATM) | Buyer neither gains nor loses | Stock at ₹100 (strike = market) |

| Out of the Money (OTM) | Buyer would lose by exercising | Stock at ₹80 (why buy at ₹100?) |

Understanding ITM/ATM/OTM

In Stock Terms (Call Option on Reliance at ₹100 Strike):

| Stock Price | Status | What Happens |

|---|---|---|

| ₹120 | ITM ✅ | Exercise! Buy at ₹100, immediately worth ₹120 → Profit ₹20 |

| ₹100 | ATM | No gain. Buy at ₹100, worth ₹100 |

| ₹80 | OTM ❌ | Don't exercise. Why pay ₹100 for something worth ₹80? Option expires worthless. |

The Key Insight:

"In the Money" = Your option has real value right now

- For a Call (right to buy): ITM when Market > Strike (you can buy cheap!)

- For a Put (right to sell): ITM when Market < Strike (you can sell high!)

Forwards vs Futures

| Parameter | Forwards | Futures |

|---|---|---|

| Trading Venue | OTC (between two parties) | Exchange Traded |

| Contract Terms | Customizable (any amount, date) | Standardized (fixed lot size, expiry) |

| Counterparty Risk | Yes (risk of default) | No (exchange guarantees settlement) |

| Delivery | Mandatory | Not mandatory (can square off) |

| Settlement | On maturity date | Daily MTM settlement |

| Example | Forward contract in forex | Nifty Futures on NSE |

1. Forwards:

- A private contract between two parties (OTC) for a pre-determined quantity, at a pre-determined price.

- Delivery is compulsory on the settlement date.

- Example: A bank books a forward contract with an importer to sell $1 million at ₹85/USD after 3 months.

2. Futures:

- A standardized contract traded on an exchange, for a fixed lot size, at a pre-determined price.

- Delivery is not compulsory—most futures are squared off (closed) before expiry.

- The exchange acts as counterparty, requiring margin deposits from both parties.

- Example: Trading Nifty Futures on NSE with a lot size of 25 units.

Summary Cheat Sheet

Quick Reference: Derivative Types

| Derivative Type | OTC or Exchange | Underlying | Key Feature |

|---|---|---|---|

| Forward | OTC | Forex, Commodity | Customizable, Delivery mandatory |

| Future | Exchange | Stock, Index, Commodity | Standardized, Delivery optional |

| Option | Both | Stock, Index, Forex | Right (not obligation), Premium paid |

| Swap | OTC | Interest Rate, Currency | Exchange of payment streams |

| FRA | OTC | Interest Rate | Single settlement date |

Interest Rate Derivatives at a Glance

| Instrument | Parties | Settlement | Exchange/OTC |

|---|---|---|---|

| FRA | Two parties | Single date, cash difference | OTC |

| IRS | Two parties | Multiple dates, interest streams | OTC |

| IRF | Via Exchange | Daily MTM | Exchange |

Currency Derivatives at a Glance

| Instrument | Key Feature | Delivery | Use Case |

|---|---|---|---|

| Forex Forward | Fixed rate for future | Mandatory | Importer/Exporter hedging |

| Currency Swap | Exchange interest + principal | As per contract | Managing currency mismatch |

| Currency Option | Right to buy/sell at strike | Optional | Protection with upside potential |

Options: Key Terms

| Term | Call Option | Put Option |

|---|---|---|

| Buyer's Right | To BUY | To SELL |

| Seller's Obligation | To SELL if exercised | To BUY if exercised |

| Buyer Profits When | Market Price > Strike | Market Price < Strike |

| Max Loss for Buyer | Premium paid | Premium paid |

Option Moneyness

| Status | Call Option (Strike ₹100) | Put Option (Strike ₹100) |

|---|---|---|

| ITM | Market > ₹100 | Market < ₹100 |

| ATM | Market = ₹100 | Market = ₹100 |

| OTM | Market < ₹100 | Market > ₹100 |

American vs European Options

| Feature | American | European |

|---|---|---|

| Exercise | Any time before expiry | Only on expiry date |

| Flexibility | More flexible | Less flexible |

| Premium | Generally higher | Generally lower |

| In India | Not common | All stock/index options |

Forwards vs Futures: Quick Comparison

| Feature | Forward | Future |

|---|---|---|

| Trading | OTC (Private) | Exchange |

| Standardization | Customizable | Fixed lot, expiry |

| Counterparty Risk | ✅ Yes | ❌ No (exchange guarantee) |

| Margin | Not required | Required (Initial + Variation) |

| Delivery | Compulsory | Optional (can square off) |

| Settlement | At maturity | Daily MTM |

| Regulation | Less regulated | Highly regulated |

Key Exam Points

| Concept | Remember |

|---|---|

| Derivative Value | Derived from underlying (stock, forex, commodity, interest rate) |

| Hedging | Primary purpose of derivatives |

| OTC Market | Forwards, Swaps, FRA, IRS (Counterparty risk exists) |

| Exchange Traded | Futures, Options (No counterparty risk) |

| Premium | Fee paid by option buyer to seller |

| Strike Price | Pre-agreed price in option contract |

| Notional Principal | Reference amount for calculating payments (no actual exchange) |

| MTM | Mark-to-Market — daily settlement in futures |

| India Options | All stock/index options are European style |

Lesson Doubts

Ask questions, get expert answers