🔄 Securitisation

Comprehensive guide to Securitisation, Factoring, Forfaiting, and TReDS.

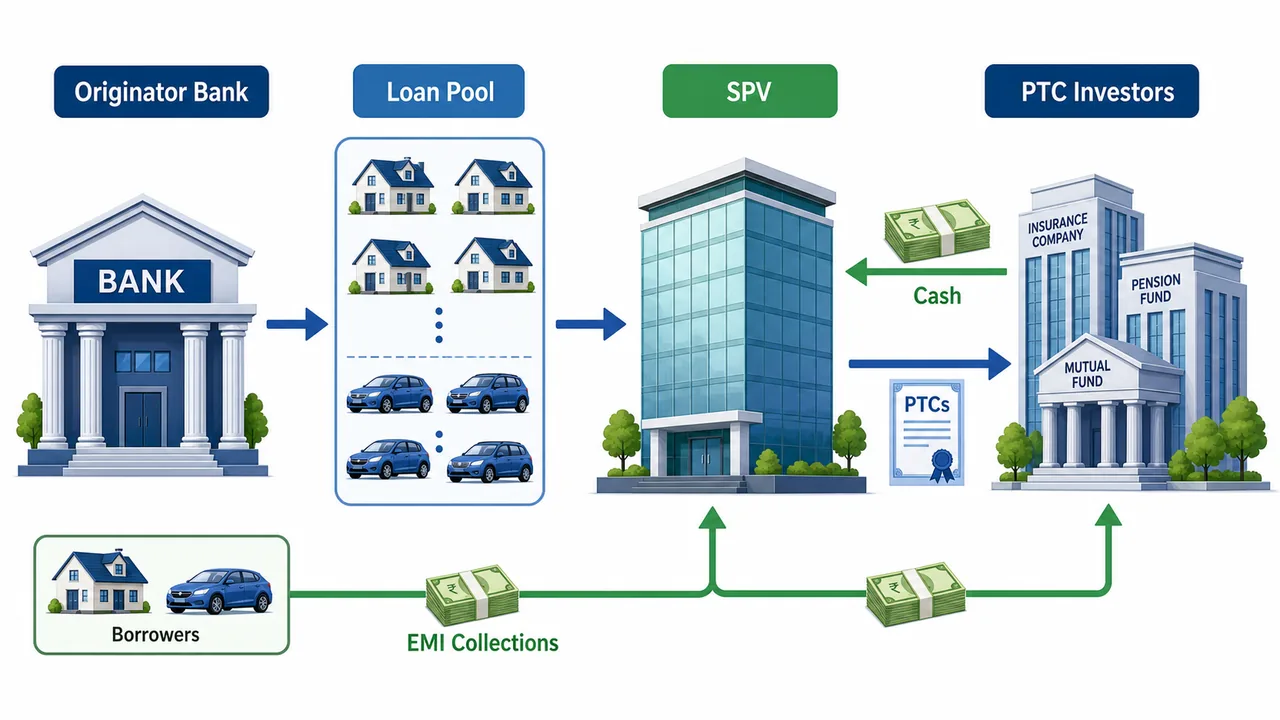

Securitization

Securitization is the process of converting homogeneous loans & loan receivables into marketable securities. These securities are typically called Pass Through Certificates (PTC).

In simpler terms, a bank takes a pool of similar loans (like home loans or car loans), bundles them together, and sells them to investors as securities. This clears the bank's balance sheet and provides funds to lend again.

Parties Involved

- Originator (assigns receivable to SPV): The bank or financial institution that originally lent the money (e.g., gave the home loans). They "originate" the assets and then assign (sell) the receivables to the SPV.

- Special Purpose Vehicle (SPV): An entity created specifically for this transaction. It buys the loans from the originator and issues securities to investors. It acts as an intermediary to isolate the assets from the originator's bankruptcy risk.

- Rating agency: They assess the quality of the pooled assets and assign a credit rating to the securities (PTCs). A higher rating helps attract investors.

- Underwriters (credit enhancer): They may guarantee the sale of the securities or provide credit enhancement (like a guarantee) to improve the credit rating and protect investors against defaults.

- Investor (QIB) gets PTC pays cash: The final buyers of the securities, typically Qualified Institutional Buyers (QIBs) like mutual funds, insurance companies, or pension funds. They pay cash to the SPV and receive the Pass Through Certificates (PTC).

Types of Securitization

- Asset Backed (Auto Loans): When the underlying assets are short-term loans like car loans, credit card receivables, etc.

- Mortgage Backed (Home Loans): When the underlying assets are mortgages (housing loans). These are often called Mortgage-Backed Securities (MBS).

Benefits

- Management of credit concentration risk by originator bank: By selling off loans, the bank reduces its exposure to a specific sector or type of borrower.

- Recycling of funds by originator bank: The bank gets immediate cash for its future receivables, which it can use to issue fresh loans.

- Opportunity to investor to participate in good quality assets: Investors gain access to a pool of diversified lending assets that they couldn't lend to directly.

FACTORING (Domestic & Export)

Factoring is a financial service involving the financing of short-term receivables of a seller (Client) by a "Factor" for collection on the due date. It typically involves short-term domestic receivables arising from the sale of goods and services, with maturities usually 90 days or less.

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Securitization

Securitization is the process of converting homogeneous loans & loan receivables into marketable securities. These securities are typically called Pass Through Certificates (PTC).

In simpler terms, a bank takes a pool of similar loans (like home loans or car loans), bundles them together, and sells them to investors as securities. This clears the bank's balance sheet and provides funds to lend again.

Parties Involved

- Originator (assigns receivable to SPV): The bank or financial institution that originally lent the money (e.g., gave the home loans). They "originate" the assets and then assign (sell) the receivables to the SPV.

- Special Purpose Vehicle (SPV): An entity created specifically for this transaction. It buys the loans from the originator and issues securities to investors. It acts as an intermediary to isolate the assets from the originator's bankruptcy risk.

- Rating agency: They assess the quality of the pooled assets and assign a credit rating to the securities (PTCs). A higher rating helps attract investors.

- Underwriters (credit enhancer): They may guarantee the sale of the securities or provide credit enhancement (like a guarantee) to improve the credit rating and protect investors against defaults.

- Investor (QIB) gets PTC pays cash: The final buyers of the securities, typically Qualified Institutional Buyers (QIBs) like mutual funds, insurance companies, or pension funds. They pay cash to the SPV and receive the Pass Through Certificates (PTC).

Types of Securitization

- Asset Backed (Auto Loans): When the underlying assets are short-term loans like car loans, credit card receivables, etc.

- Mortgage Backed (Home Loans): When the underlying assets are mortgages (housing loans). These are often called Mortgage-Backed Securities (MBS).

Benefits

- Management of credit concentration risk by originator bank: By selling off loans, the bank reduces its exposure to a specific sector or type of borrower.

- Recycling of funds by originator bank: The bank gets immediate cash for its future receivables, which it can use to issue fresh loans.

- Opportunity to investor to participate in good quality assets: Investors gain access to a pool of diversified lending assets that they couldn't lend to directly.

FACTORING (Domestic & Export)

Factoring is a financial service involving the financing of short-term receivables of a seller (Client) by a "Factor" for collection on the due date. It typically involves short-term domestic receivables arising from the sale of goods and services, with maturities usually 90 days or less.

- Parties Involved: Factoring typically involves 3 parties — the seller (client), the debtor (buyer), and the factor.

- Trade Instrument: Factoring uses invoices as the underlying instrument.

- Regulation: Governed by the rules of the factoring agreement between parties and the Factoring Regulation Act, 2011.

Functions of Factors

- Credit function (Advance): Advancing typically 80% of the invoice value immediately to the seller upon bill of exchange acceptance.

- Sales ledger administration: Maintaining the accounts of the receivables and managing the sales ledger.

- Collection of dues: Following up with the buyer to collect payment on the due date.

- Credit control: Providing management of receivables and credit risk assessment.

Key Limits in Factoring

| Parameter | Limit |

|---|---|

| Advance Amount | Typically 80% of invoice value |

| Maximum Grace Duration | 60 days |

| Maximum Debt Outstanding | 150 days |

Types of Recourse (Risk)

- Without Recourse Factoring (बिना किसी अधिकार या दावे के): The non-payment risk is borne by the Factor. If the buyer defaults, the Factor takes the loss.

- With Recourse Factoring (अधिकार या दावे के साथ): The non-payment risk remains with the Client (Seller). If the buyer defaults, the seller must refund the money to the Factor.

Factoring can be for short-term domestic sales or export receivables. It is the more common of the two services due to its flexibility and shorter tenor.

Example: Factoring Transaction

Scenario: You run a business, ABC Apparel, that supplies shirts to a large retail chain called MegaMart. After delivering the shirts, MegaMart will pay you in 60 days, but you need the money now to pay your suppliers.

| Step | Detail |

|---|---|

| Total Invoice Value | ₹1,00,000 |

| Factor Advance (90%) | You receive ₹90,000 immediately |

| Collection | After 60 days, FastCash Factors collects ₹1,00,000 from MegaMart |

| Factor Fee (2%) | ₹10,000 – ₹2,000 = ₹8,000 returned to you |

| Total You Receive | ₹90,000 + ₹8,000 = ₹98,000 (₹2,000 is the factoring fee) |

FORFAITING for Export Receivables

Forfaiting is a form of financing specifically used for international trade. It primarily concerns medium to long-term international (export) receivables, often with maturities up to 5 years.

- Definition: A factoring type arrangement involving 2 main parties — the exporter (seller) and the forfaiter.

- Advance Amount: Often 100% of the export value, but at a discount (the forfaiter deducts its fee/discount upfront).

- Trade Instrument: Uses bills of exchange or promissory notes (not invoices like factoring).

- Regulation: Governed by international rules, e.g., UCP (Uniform Customs and Practice) for documentary credits.

- Scope: Exclusively used for international transactions (unlike factoring which is commonly domestic).

- Services: Primarily focused on the financing aspect without additional services like ledger maintenance or credit control.

- Risk: It is almost always without recourse to the exporter — the forfaiter bears the risk of non-payment by the buyer. Once the exporter sells the receivables, they have zero liability if the importer defaults.

Example: Forfaiting Transaction

Scenario: You're an Indian exporter who has shipped goods worth ₹10,00,000 to an overseas buyer with a 1-year credit period. You're unsure about the creditworthiness of the buyer and don't want to wait a year.

| Step | Detail |

|---|---|

| Export Value | ₹10,00,000 |

| Discount Rate | 5% |

| You Receive Immediately | ₹9,50,000 (95% of ₹10,00,000) |

| After 1 Year | SureCash Forfeiters collects ₹10,00,000 from the overseas buyer |

| Your Cost | ₹50,000 discount is the fee for the forfaiting service |

| If Buyer Defaults? | The forfaiter bears the loss — no recourse to you |

Factoring vs Forfaiting — Key Differences

| Criteria | Factoring | Forfaiting |

|---|---|---|

| Definition | Financial service where a business sells its receivables to a third party (factor) to get immediate cash | Financial service where an exporter sells its medium to long-term receivables at a discount to obtain cash |

| Number of Parties | 3 parties: seller, debtor, and factor | 2 main parties: exporter (seller) and the forfaiter |

| Nature of Receivables | Short-term domestic receivables | Medium to long-term international (export) receivables |

| Tenor | Short-term, usually up to 90 days (max 150 days) | Medium to long-term, often up to 5 years |

| Advance Amount | Typically 80% of invoice value | Often 100% of export value, but discounted |

| Coverage | Usually domestic transactions (can be used internationally) | Exclusively international transactions |

| Risk | Depends on type — with recourse (seller bears risk) or without recourse (factor bears risk) | Forfaiter bears the risk of non-payment (always without recourse) |

| Services | Receivables management, credit control, collection of debt, sales ledger maintenance | Primarily focused on financing aspect without additional services |

| Trade Instrument | Invoices | Bills of exchange or promissory notes |

| Regulation | Factoring agreement between parties | International rules, e.g., UCP for documentary credits |

| Popularity | More common (flexibility & shorter tenor) | Less common, used for specific medium to long-term international deals |

TIP

Quick Gist: In both services, you get money immediately by sacrificing a portion of the total value. However, factoring is typically for shorter domestic receivables, whereas forfaiting is for longer-term export-based transactions.

Trade Receivables Discounting System (TReDS)

TReDS is an institutional mechanism set up by the RBI to facilitate the discounting of trade receivables (invoices) of MSMEs from corporate and other buyers, including Government Departments and Public Sector Undertakings (PSUs), through multiple financiers.

-

Purpose: To address the liquidity challenges and working capital cycles of MSMEs by facilitating the discounting of invoices or bills of exchange.

-

Platform: It serves as an electronic auction platform where receivables are traded, ensuring a transparent and competitive price discovery mechanism.

-

Mechanism (Step-by-Step):

- Sellers (MSMEs) deliver goods on credit to buyers, issue invoices (called Factoring Unit or FU), and upload them on TReDS.

- Buyers (Corporates/PSUs) log in to TReDS and flag the FU as "accepted".

- On acceptance, TReDS sends information to the buyer's bank—the buyer's account is linked to the FU.

- Financiers view accepted FUs and place competitive bids at different discount rates.

- Sellers can opt for the best bid quoted by a financier.

- Funds are credited to the Seller's account on T+1 day basis.

- On the due date, TReDS sends a message for payment of the due amount from the buyer's account.

- The MSME seller bears the interest (discounting) cost. The buyer pays the full amount at maturity.

-

Default & Recourse:

- Non-payment by the buyer is treated as a default on the buyer (not the seller).

- The financier has no recourse against the MSME seller—this is crucial as it protects MSMEs from being held liable if their buyer defaults.

-

Legal Framework: The Factoring Unit (FU) is legally similar to a physical instrument under the Negotiable Instruments Act and the Factoring Regulation Act, 2011.

-

Parties:

- Sellers: Only Micro, Small, and Medium Enterprises (MSMEs) as defined under the MSMED Act, 2006, are eligible to participate as sellers on the TReDS platform.

- Buyers: Corporates, PSUs, Govt departments, etc. It is mandatory for companies with a turnover of > Rs. 250 crore and all CPSEs (Central Public Sector Enterprises) to register on TReDS.

- Financiers: Banks, NBFC-Factors, and other eligible financial institutions.

-

TReDS Platforms: To set up a TReDS platform (e.g., RXIL - Receivables Exchange of India Ltd, M1xchange, Invoicemart), the minimum paid-up equity capital required is Rs. 25 crore. ⭐

Example Scenario: TReDS Transaction (BrightSteel & Reliance)

BrightSteel is an MSME vendor for Reliance Industries which accepts the invoice of Rs. 20,00,000 for payment in 60 days. SBI bids at 7.5% p.a. and accepts the bid. BrightSteel receives ₹19,75,343 immediately, and Reliance pays ₹20,00,000 to SBI after 60 days.

Participants & Terms

- Seller (MSME): "BrightSteel Co."

- Buyer (Large Corp): "Reliance Industries" (Mandated to register)

- Financier: "State Bank of India" (SBI)

- Platform: RXIL (Receivables Exchange of India Ltd)

- Invoice: ₹20,00,000 | Credit Period: 60 days | Rate: 7.5% p.a.

The Transaction Flow

- Invoice Upload: BrightSteel uploads the ₹20,00,000 invoice to RXIL.

- Buyer Acceptance: Reliance digitally accepts the invoice, confirming payment in 60 days.

- Financier Bidding: SBI views the invoice and places a bid at 7.5% p.a.

- Seller Accepts (Day 2): BrightSteel accepts SBI's bid.

- Funds Disbursed: SBI transfers the discounted amount to BrightSteel immediately.

- Interest Calculation: (20,00,000 × 7.5% × 60/365) ≈ ₹24,657

- Amount Received: 20,00,000 - 24,657 = ₹19,75,343

- Benefit: BrightSteel gets working capital instantly instead of waiting 60 days.

- Final Settlement (Day 60): Reliance pays the full ₹20,00,000 to SBI. SBI earns the ₹24,657 as profit.

Summary Cheat Sheet

| Concept / Topic | Key Details |

|---|---|

| Securitization | Converting loans into marketable securities (PTCs) via an SPV |

| SPV Role | Buys loans from originator, issues PTCs to QIB investors |

| Securitization Types | Asset-Backed (Auto) and Mortgage-Backed (Home Loans) |

| Factoring — Definition | Financing of short-term receivables by a Factor |

| Factoring — Parties | 3 parties: seller, debtor (buyer), factor |

| Factoring — Advance | Typically 80% of invoice value |

| Factoring — Maturity | Short-term, usually 90 days or less |

| Factoring — Max Grace | 60 days |

| Factoring — Max Outstanding | 150 days |

| Factoring — Instrument | Invoices |

| With Recourse | Non-payment risk on seller |

| Without Recourse | Non-payment risk on factor |

| Forfaiting — Definition | Financing of medium to long-term export receivables |

| Forfaiting — Parties | 2 main parties: exporter and forfaiter |

| Forfaiting — Advance | Often 100% of export value (discounted) |

| Forfaiting — Maturity | Up to 5 years |

| Forfaiting — Recourse | Always without recourse (forfaiter bears risk) |

| Forfaiting — Instrument | Bills of exchange / promissory notes |

| Forfaiting — Regulation | International rules, UCP for documentary credits |

| Forfaiting — Scope | Exclusively international transactions |

| TReDS — Purpose | MSME invoice discounting |

| TReDS — Sellers | MSMEs only |

| TReDS — Buyers | Corporates > ₹250 cr turnover (mandatory) |

| TReDS — Min Capital | ₹25 crore for platform |

| TReDS — Settlement | T+1 day |

| TReDS — Recourse | No recourse against MSME seller |

Lesson Doubts

Ask questions, get expert answers