📜 Money Market Instruments

Detailed overview of CD, CP, NCD, TREPS, Repo, and Government Securities like T-Bills and Dated Securities.

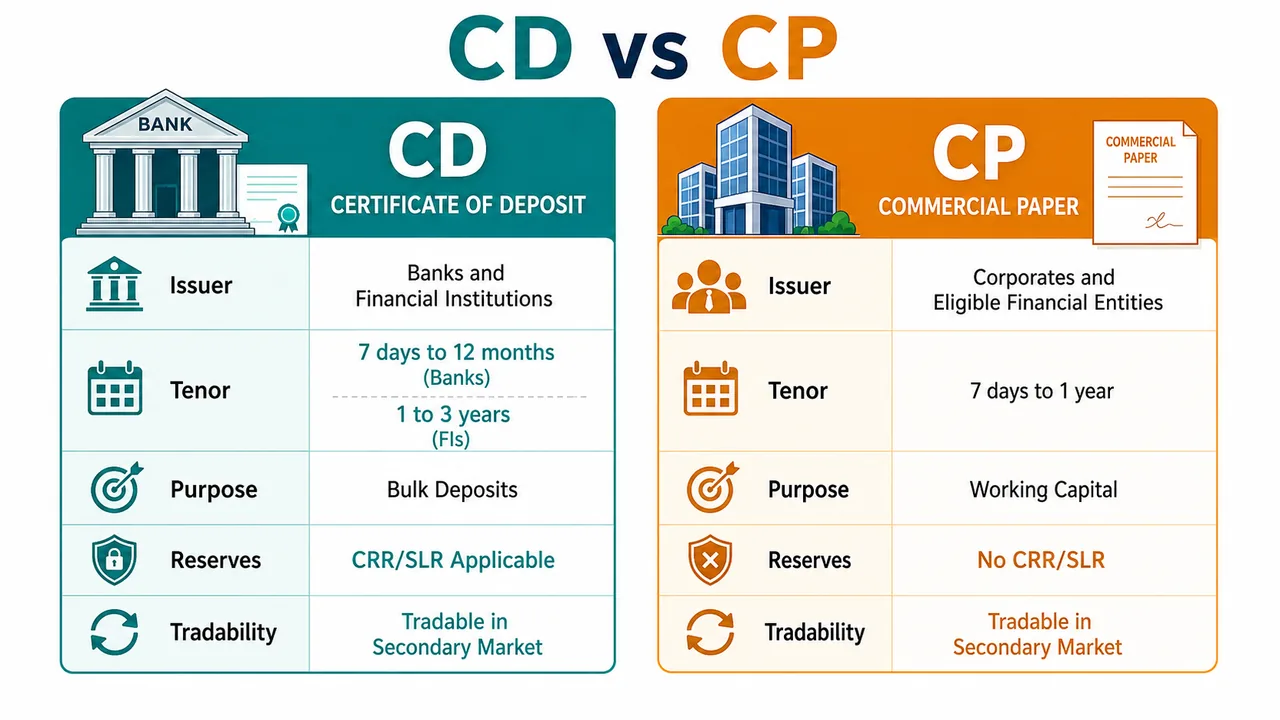

Certificate of Deposit (CD)

A Certificate of Deposit (CD) is a money market instrument that allows banks and financial institutions to raise bulk deposits from the market. It is essentially a receipt issued by a bank acknowledging that a sum of money has been deposited for a specified period at a specified interest rate.

Regulated by RBI CD Directions 2021

-

Definition: An unsecured usance promissory note. "Usance" means it has a fixed maturity period, and "unsecured" means it is not backed by any collateral—the investor relies on the creditworthiness of the issuing bank.

-

Issuers: Can be issued by Scheduled Commercial Banks (SCB), Regional Rural Banks (RRBs), Small Finance Banks (SFB), and Financial Institutions (FIs) for raising bulk deposits. This provides banks with an alternative source of funds beyond regular savings/current accounts.

-

Form: Issued in Demat format (electronic, no physical certificate), at a discount to face value (like T-Bills—you pay less than face value and receive face value at maturity). Settlement happens on T+1 day basis.

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Certificate of Deposit (CD)

A Certificate of Deposit (CD) is a money market instrument that allows banks and financial institutions to raise bulk deposits from the market. It is essentially a receipt issued by a bank acknowledging that a sum of money has been deposited for a specified period at a specified interest rate.

Regulated by RBI CD Directions 2021

-

Definition: An unsecured usance promissory note. "Usance" means it has a fixed maturity period, and "unsecured" means it is not backed by any collateral—the investor relies on the creditworthiness of the issuing bank.

-

Issuers: Can be issued by Scheduled Commercial Banks (SCB), Regional Rural Banks (RRBs), Small Finance Banks (SFB), and Financial Institutions (FIs) for raising bulk deposits. This provides banks with an alternative source of funds beyond regular savings/current accounts.

-

Form: Issued in Demat format (electronic, no physical certificate), at a discount to face value (like T-Bills—you pay less than face value and receive face value at maturity). Settlement happens on T+1 day basis.

-

Maturity:

- Banks: Minimum 7 days and maximum 12 months.

- Financial Institutions (FIs): Minimum 1 year and maximum 3 years. FIs have longer tenors because they typically fund longer-term projects.

-

Amount: Minimum Rs. 5 lakh (no maximum limit). Must be in multiples of Rs. 5 lakh. This ensures CDs remain a wholesale/institutional instrument.

-

Conditions:

- No loan against CD — Banks cannot grant loans using CD as collateral.

- No premature cancellation — The investor must hold until maturity (or sell in secondary market).

- Transferable any time — CDs can be freely transferred/sold to other investors.

- Trading in secondary market allowed — CDs can be bought/sold on exchanges with T+1 day settlement.

-

Buy back: The issuing bank can buy back its own CD only after 7 days from the date of issue.

-

Maturity day: If the CD matures on a holiday, payment is made on the preceding working day (not the next working day).

-

Reserves: CDs are treated as deposits for reserve requirements—CRR and SLR are applicable on CD balances. This is important for banks' liquidity management.

-

Investors: Individuals, companies, financial institutions, other banks, trusts, funds, etc. can invest in CDs.

Commercial Paper (CP)

What is Commercial Paper?

Commercial Paper (CP) is an unsecured usance promissory note issued by corporations and financial institutions to raise funds for short-term obligations like working capital, payroll, or inventory financing. Think of it as an "IOU" (I Owe You)—a formal acknowledgement of debt—that companies issue instead of taking a bank loan.

Why Do Companies Issue CP?

- Cheaper than Bank Loans: Interest rates on CP are typically lower than bank lending rates.

- Flexibility: Quick issuance without lengthy loan approval processes.

- No Collateral Required: It's unsecured, so companies don't need to pledge assets.

Key Features:

| Feature | Details |

|---|---|

| Maturity | 7 days to 1 year |

| Denomination | Min ₹5 lakh (multiples of ₹5 lakh) |

| Mode of Issue | Discount to face value (like T-Bills) |

| Trading | Can be traded in secondary market |

- Form: Issued in Demat format (electronic, no physical certificate), at a discount to face value.

Eligibility Conditions for a company:

- Sanctioned working capital limits.

- Loans should be in standard category and min credit rating AAA from 1 SEBI approved credit rating agency (update 03.01.2024), if amount is Rs. 1000 cr or more in calendar year.

- Companies, Non-Banking Financial Companies (NBFCs), Housing Finance Companies (HFCs), Infrastructure Investment Trusts (InvITs), Real Estate Investment Trusts (REITs), and All India Financial Institutions (AIFIs).

- Other Eligible Entities: Societies, LLPs, other corporate bodies with Net Worth of Min Rs. 100 cr.

- Individual/HUF investors: Max 25% of total amount of issue.

- Settlement Cycles: Over-the-Counter (OTC) transactions can be settled on either a T+0 (same day) or T+1 (next business day) basis, providing flexibility in how quickly funds are transferred.

- Buy Back: Companies can buy back their own CP from the market to reduce debt if they have surplus cash. However, this is only permitted after a minimum holding period of 7 days from the date of issue.

CD vs CP: Key Differences

| Parameter | Certificate of Deposit (CD) | Commercial Paper (CP) |

|---|---|---|

| Issuer | Banks & Financial Institutions | Corporates, NBFCs, FIs |

| Security | Unsecured (but considered safe, as issued by banks) | Also unsecured (but considered riskier) |

| Purpose | Raise bulk deposits | Raise working capital |

| Maturity | 7 days – 12 months (Banks), 1–3 years (FIs) | 7 days – 12 months |

| Min Amount | ₹5 lakh | ₹5 lakh |

| Premature Cancellation | Not allowed | Not applicable (can sell in market) |

| Buy Back | After 7 days | After 7 days |

| Loan Against | Not permitted | Not applicable |

| CRR/SLR | Applicable (treated as deposit) | Not applicable |

| Credit Rating | Not required | Required (min A3) |

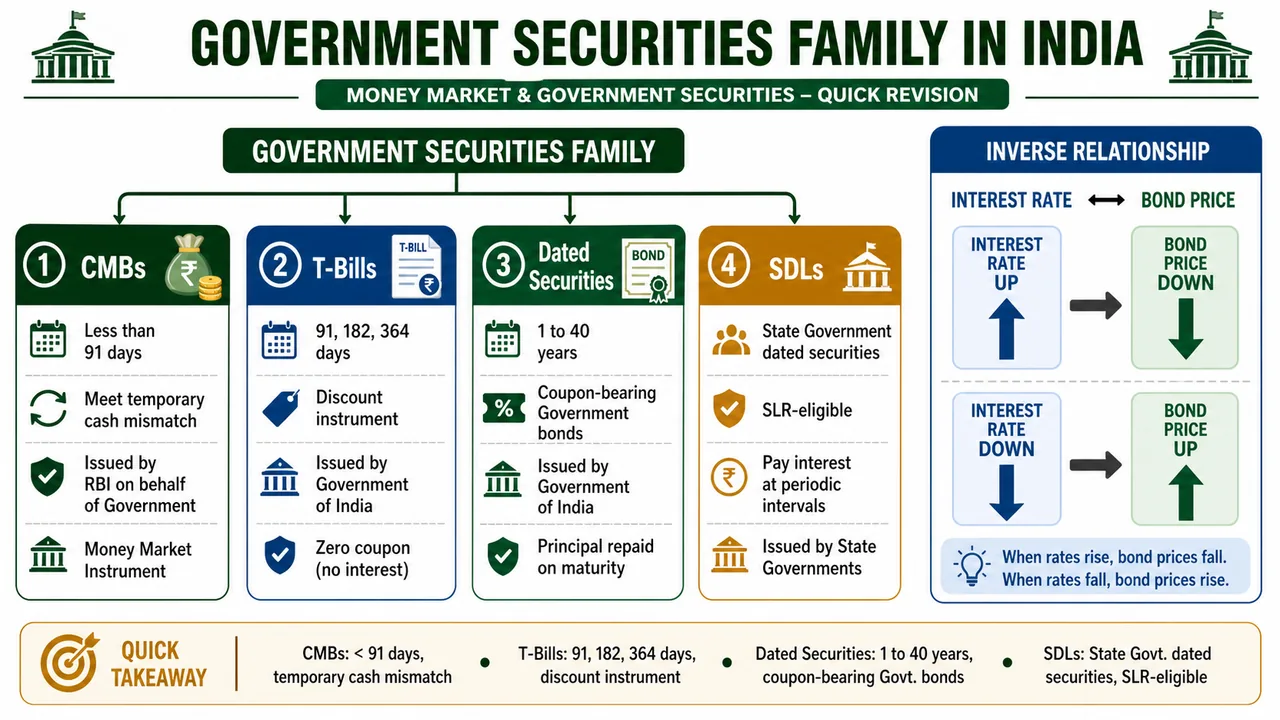

Govt. Securities (Gilt-Edged or G-Securities)

Government Securities (G-Secs) are debt instruments issued by the government to borrow money from the market. They are called "Gilt-Edged" because they carry virtually zero default risk—the government will always honor its debt obligations. G-Secs form the backbone of India's debt market and are crucial for banks' SLR compliance.

- Definition: A tradable instrument issued by RBI through auction on the NDS (Negotiated Dealing System) platform, on behalf of the Government to borrow money. The NDS is an electronic platform that facilitates trading and settlement of G-Secs.

- Issuers:

- Central Government: Issues Treasury Bills (short-term) and Dated Securities (long-term).

- State Governments: Issue State Development Loans (SDLs), also known as State Development Bonds.

- Investors: Include banks, Primary Dealers (PDs), insurance companies, mutual funds, and provident funds. Eligible investors must maintain a Subsidiary General Ledger (SGL) account with RBI—this is an electronic account that holds G-Secs in dematerialized form.

1. Cash Management Bills (CMBs)

CMBs are ultra-short-term instruments used by the government to manage temporary cash flow mismatches.

- Character: Has the generic character of a Treasury Bill (issued at discount, zero-coupon).

- Maturity: Less than 91 days. This distinguishes them from regular T-Bills which have fixed tenors of 91/182/364 days.

- Purpose: Used when the government needs very short-term funds to bridge timing gaps between receipts and payments.

2. Treasury Bills (T-Bills)

T-Bills are short-term money market instruments issued by RBI on behalf of the Central Government. They are the safest short-term investment option.

- Maturity: Available in three tenors: 91 days, 182 days, and 364 days.

- Zero Coupon: Issued at a discount to face value—meaning you pay less than ₹100 and receive ₹100 at maturity. There are no periodic interest payments.

- Return: The return to the investor is the difference between the issue price and face value. For example, if you buy a 91-day T-Bill at ₹98.50 and receive ₹100 at maturity, your return is ₹1.50.

- Min amount: Rs. 10,000 (w.e.f. 1st April 2020, RBI reduced from ₹25,000 to ₹10,000 to encourage retail participation).

- Auction Schedule:

- 91-day T-Bills: Auctioned every Wednesday.

- 182-day + 364-day T-Bills: Auctioned on alternate Wednesdays.

- Settlement: T+1 day basis (funds and securities exchanged on the next business day).

3. Dated Securities

Dated Securities are long-term government bonds that pay periodic interest (coupon) and return the principal at maturity.

- Tenor: Long-term loans and bonds ranging from 1 year to 40 years (typically 5-30 years).

- Depository: The Public Debt Office (PDO) of RBI maintains the registry and acts as depository for these securities.

- Coupon: Most are fixed coupon securities—they pay a fixed interest rate (coupon) semi-annually.

- Minimum amount: Rs. 10,000 (and multiples thereof).

- Types of Bonds:

- Fixed Rate Bonds: Pay a fixed coupon rate throughout the life of the bond.

- Floating Rate Bonds (FRBs): Coupon rate is linked to a benchmark (like T-Bill rate) and changes periodically.

- Zero Coupon Bonds: Issued at discount, no periodic interest, full value paid at maturity.

https://www.rbi.org.in/commonman/english/scripts/PressReleases.aspx?Id=3217

4. State Development Loans (SDLs)

SDLs are dated securities issued by State Governments to meet their borrowing requirements.

- Issuance: Issued by RBI through auction on behalf of State Governments. The auction mechanism is similar to Central Government dated securities.

- Character: Similar to dated securities—they pay coupon semi-annually and have medium to long-term maturity.

- SLR Eligibility: Investment in SDLs qualifies for SLR purposes, making them attractive for banks. Banks can hold SDLs to meet their Statutory Liquidity Ratio requirements.

Effect of Market Interest Rate on G-Sec Value

The market value of fixed-income securities (like bonds) has an inverse relationship with market interest rates:

-

MROI > CR (Market Rate of Interest > Coupon Rate): When current market interest rates rise above the coupon rate of your bond, the bond becomes less attractive (new bonds offer higher rates), so its Market Value (MV) will decline.

-

CR > MROI (Coupon Rate > Market Rate of Interest): When current market interest rates fall below the coupon rate of your bond, the bond becomes more attractive (it offers a higher rate than new bonds), so its MV will increase.

💡 Exam Tip: Remember this as an inverse relationship—when interest rates go UP, bond prices go DOWN, and vice versa.

Example: Understanding the Inverse Relationship

You own a 10-year Government Bond:

- Face value: ₹100

- Coupon Rate: 7% (pays ₹7 per year)

Scenario 1: Market rates RISE to 9%

- New bonds now offer 9% (₹9 per year)

- Your bond still pays only 7% (₹7 per year)

- Nobody wants your bond at ₹100 because new bonds pay more

- Your bond's price drops to ~₹78 (to compensate buyers for the lower coupon)

Scenario 2: Market rates FALL to 5%

- New bonds now offer only 5% (₹5 per year)

- Your bond pays 7% (₹7 per year) — better than new bonds!

- Everyone wants your bond, driving up demand

- Your bond's price rises to ~₹120 (buyers pay a premium for higher coupon)

| Market Rates | Your Bond's Appeal | Bond Price |

|---|---|---|

| ⬆️ Go UP | Less attractive | ⬇️ Falls |

| ⬇️ Go DOWN | More attractive | ⬆️ Rises |

Classification of SLR Securities

Banks are required to maintain a portion of their deposits in liquid assets (SLR). When banks invest in Government Securities to meet this requirement, they must classify these securities into specific categories based on their intent—whether they plan to hold, trade, or sell them. This classification affects how the securities are valued and how gains/losses are reported.

SLR securities are classified as:

-

Held to Maturity (HTM):

- Securities the bank intends to hold until maturity (no intention to sell).

- Limit: Maximum 25% of total deposits (can be higher with RBI permission during extraordinary circumstances).

- Advantage: No Mark-to-Market (MTM) losses—even if market prices fall, the bank doesn't have to book losses since it will hold till maturity and receive face value.

- Use Case: Banks use HTM to protect their P&L from interest rate volatility.

-

Held for Trading (HFT):

- Securities acquired with the intention to sell in the short term (within 90 days) to profit from price movements.

- Must be marked to market daily—gains/losses are immediately reflected in the P&L.

- High Risk: Exposes the bank to market volatility.

-

Available for Sale (AFS):

- Securities that don't fit into HTM or HFT categories.

- The bank may or may not sell them—there's no fixed intent.

- Marked to market periodically (typically quarterly), and gains/losses are taken to reserves (not directly to P&L until sold).

-

Fair Value through Profit and Loss (FVTPL):

- Securities held for trading purposes where gains/losses are recognized directly in the Profit & Loss account.

- Note: HFT is a sub-category within FVTPL. Both are marked to market with changes hitting the income statement.

Time of Classification:

- Classification is decided at the time of purchase—banks must declare their intent upfront.

- Reclassification: Allowed only once a year, typically at the beginning of the financial year. Frequent switching is not permitted to prevent manipulation of reported profits.

Valuation:

| Category | Valuation Method | Impact |

|---|---|---|

| HTM | Acquisition cost (book value) | No MTM impact on P&L |

| AFS | Mark-to-Market | Gains/losses to reserves |

| FVTPL/HFT | Mark-to-Market | Gains/losses to P&L immediately |

💡 Why This Matters: During rising interest rate cycles, bond prices fall. Banks with large AFS/HFT portfolios may report significant MTM losses, while banks with more securities in HTM are protected from such volatility.

Short term Non-Convertible Debentures (NCD)

Non-Convertible Debentures (NCDs) are fixed-income debt instruments issued by companies to raise funds from capital markets. Unlike convertible debentures, NCDs cannot be converted into equity shares—they remain as debt until maturity. Short-term NCDs can be issued under two frameworks:

- Companies Act, 2013 — General framework for corporate debentures regulated by SEBI.

- RBI Guidelines — Specific framework for short-term NCDs in the money market (detailed below).

Issue under RBI guidelines:

- Purpose: Companies can issue short-term NCDs to raise working capital or short-term funds from the money market. This provides an alternative to bank borrowing and Commercial Paper.

- Period: Minimum 90 days and maximum 12 months. This makes them suitable for bridging temporary cash flow gaps or financing short-term projects.

- Amount: Minimum denomination of Rs. 5 lakh (no maximum limit). Must be in multiples of Rs. 1 lakh. Like CP, this ensures the instrument remains in the wholesale/institutional market segment.

- Conditions to be satisfied by a company: Same eligibility criteria as Commercial Paper (CP)—the company must have sanctioned working capital limits, loan accounts in standard category, and a valid credit rating (minimum A3 from SEBI-approved CRAs).

CP vs NCD: While both are short-term debt instruments, CP is an unsecured promissory note (issued at discount), while NCDs are debentures (may carry a coupon). NCDs can offer better security features but are less common in the money market.

CBLO/TREPS

Collateralized Borrowing & Lending Obligation (CBLO) is a money market instrument that was developed by the Clearing Corporation of India Ltd. (CCIL) in 2003 to address the liquidity needs of banks and other market participants who were excluded from the inter-bank call money market. It has since evolved into Tri-Party Repo Dealing System (TREPS) which is the modern platform for conducting these transactions.

- CBLO: A money market instrument in the form of a tripartite repo trade. Unlike a regular repo between two parties, CBLO involves three parties—the borrower, the lender, and CCIL as the central counterparty. This structure eliminates direct counterparty exposure between the borrower and lender.

- Settlement Agent: The Clearing Corporation of India (CCIL) acts as the settlement agent and central counterparty for all CBLO/TREPS transactions. Since CCIL guarantees the settlement of every trade, there is no counterparty risk for participants. If a borrower defaults, CCIL steps in to ensure the lender receives their funds.

- Participants: Both borrowers (entities needing short-term funds) and lenders (entities with surplus funds) can be banks, primary dealers, mutual funds, insurance companies, NBFCs, and other market entities approved by CCIL.

- Platform: All CBLO transactions now take place on the Tri-Party Repo Dealing System (TREPS), which replaced the traditional CBLO segment in November 2018. TREPS is operated by CCIL and provides an electronic, automated platform for repo trades.

- Borrowers: Entities needing funds can borrow by depositing eligible securities (government securities, treasury bills, etc.) with CCIL as collateral. CCIL assigns a borrowing limit to each participant based on the value of their deposited securities.

- Lenders: Entities with surplus funds lend money against the securities deposited by borrowers. The securities remain with CCIL as collateral, providing full security to the lender for the duration of the loan.

- Mechanism: TREPS operates as an anonymous order matching system. Borrowers place borrow orders specifying amount, rate, and tenor, while lenders place lending orders. The system automatically matches compatible orders without revealing the identity of the counterparty.

- Minimum lot size: Rs. 5 lakh (and multiples of Rs. 5 lakh).

- Maturity period: 1 day to 1 year, providing flexibility for short-term liquidity management.

Regulatory Framework: For banks, TREPS is regulated by RBI, while for mutual funds, it is regulated by SEBI. SEBI mandates that mutual funds maintain a portion of their assets (at least 5%) in liquid instruments like TREPS to ensure they can meet redemption requests. Mutual funds commonly park their excess liquidity in TREPS because it is considered extremely safe—CCIL guarantees the trade and the collateral consists of government securities.

RBI Retail Direct Scheme

The RBI Retail Direct Scheme, launched on November 12, 2021, is a landmark initiative by the Reserve Bank of India to democratize access to government securities. Previously, retail investors could only invest in G-Secs through mutual funds or banks acting as intermediaries. This scheme allows individuals to directly invest in government securities without any intermediary, similar to how they buy stocks through a demat account.

-

Objective: To facilitate investment in Govt Securities by individual investors. The scheme aims to broaden the investor base for government securities, increase retail participation, and provide a safe investment avenue with sovereign guarantee.

-

Access: Through an online portal (rbiretaildirect.org.in) to open a Retail Direct Gilt Account (RDG Account) with RBI. This account is linked to the investor's savings bank account and PAN. The entire process—from account opening to buying/selling securities—is fully online.

-

Fees: No fee for opening or maintaining the account. This makes it highly attractive compared to other investment options that charge demat fees, brokerage, or fund management charges.

-

Eligible Investors:

- Individuals (Single or Joint): Any Indian citizen with a valid PAN, KYC, and savings bank account can open an RDG account—either singly or jointly with another individual.

- Non-Residents: NRIs who are eligible to invest in government securities under FEMA (Foreign Exchange Management Act) can also participate.

-

Eligible Securities: The following can be purchased through primary auctions (when issued) or secondary market (NDS-OM):

- GoI Treasury Bills: Short-term securities (91-day, 182-day, 364-day) issued at a discount.

- GoI Dated Securities: Long-term bonds (1–40 years) with fixed or floating coupon rates.

- Sovereign Gold Bonds (SGB): Government-backed gold bonds that pay 2.5% p.a. interest and track gold prices.

- State Development Loans (SDLs): Bonds issued by State Governments, similar to dated securities.

Summary Cheat Sheet

Money Market Instruments at a Glance

| Instrument | Issuer | Min Amount | Maturity | Key Feature |

|---|---|---|---|---|

| CD | Banks, FIs | ₹5 lakh | 7 days – 12 months (Banks), 1–3 years (FIs) | CRR/SLR applicable, No premature cancellation |

| CP | Corporates, NBFCs | ₹5 lakh | 7 days – 12 months | Credit rating required (A3), Unsecured |

| NCD | Companies | ₹5 lakh | 90 days – 12 months | Same eligibility as CP |

| T-Bills | Central Govt (via RBI) | ₹10,000 | 91 / 182 / 364 days | Zero coupon, Discount to face value |

| CMBs | Central Govt | — | < 91 days | Ultra-short term cash management |

| Dated Securities | Govt | ₹10,000 | 1 – 40 years | Fixed/Floating coupon, Semi-annual interest |

| SDLs | State Govt | — | Medium to long | SLR eligible |

CD vs CP vs NCD Comparison

| Parameter | CD | CP | NCD |

|---|---|---|---|

| Issuer | Banks & FIs | Corporates, NBFCs | Companies |

| Regulator | RBI | RBI | RBI / SEBI |

| Purpose | Raise bulk deposits | Working capital | Short-term borrowing |

| Security | Unsecured | Unsecured | May be secured/unsecured |

| Min Amount | ₹5 lakh | ₹5 lakh | ₹5 lakh |

| Maturity | 7 days – 12 months | 7 days – 12 months | 90 days – 12 months |

| CRR/SLR | ✅ Applicable | ❌ Not applicable | ❌ Not applicable |

| Credit Rating | Not required | Required (min A3) | Required (min A3) |

| Premature Cancellation | Not allowed | N/A (sell in market) | N/A (sell in market) |

| Buyback | After 7 days | After 7 days | — |

CBLO/TREPS Quick Reference

| Feature | Detail |

|---|---|

| Platform | TREPS (replaced CBLO in Nov 2018) |

| Operator | CCIL (Clearing Corporation of India) |

| Min Lot Size | ₹5 lakh |

| Maturity | 1 day – 1 year |

| Collateral | G-Secs / T-Bills |

| Counterparty Risk | None (CCIL guarantee) |

G-Sec Classification (SLR Securities)

| Category | Valuation | MTM Impact |

|---|---|---|

| HTM | Acquisition cost | No P&L impact |

| AFS | Mark-to-Market | Gains/losses to reserves |

| FVTPL/HFT | Mark-to-Market | Directly to P&L |

Key Exam Points

| Concept | Remember |

|---|---|

| CD/CP Min Amount | ₹5 lakh (multiples of ₹5 lakh) |

| T-Bill Min Amount | ₹10,000 (w.e.f. April 2020) |

| CD Buyback | After 7 days |

| CP Buyback | After 7 days |

| CP Credit Rating | Min A3 from SEBI-approved CRA |

| HTM Limit | Max 25% of deposits |

| Interest Rate ↑ | Bond Price ↓ (inverse relationship) |

Lesson Doubts

Ask questions, get expert answers