📜 Letter of Credit (LC): Types, Documents, UCP 600 & Operation Process | Banking Notes

Letter of Credit (LC) explained — types, parties (issuing bank, advising bank, negotiating bank), important documents, UCP 600 rules, step-by-step operation process. Complete banking finance guide for IBPS AFO, RRB SO, SBI PO exams.

Letter of Credit (LC)

A Letter of Credit (LC), also known as a Documentary Credit, is one of the most important instruments in international trade finance. It provides a secure mechanism for payment where the buyer and seller may not know each other well or operate in different legal jurisdictions.

Definition

An undertaking of an issuing bank on behalf of the applicant (buyer/importer), in favour of the beneficiary (seller/exporter), to make payment on presentation of documents, provided they are in compliance strictly as per the LC terms (Complying Presentation).

General Considerations

- LC is akin to a bank guarantee ensuring payment on presenting required documents.

- LC is not negotiable.

- LC is a device ensuring payment in trade — it is not a flexible agreement, a bank loan, or a local trade mechanism.

Advantages of LC

For Buyer:

- No upfront payment needed.

- Can secure credit due to bank guarantee.

- Can set quality checks and conditions to safeguard interests.

For Seller:

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Letter of Credit (LC)

A Letter of Credit (LC), also known as a Documentary Credit, is one of the most important instruments in international trade finance. It provides a secure mechanism for payment where the buyer and seller may not know each other well or operate in different legal jurisdictions.

Definition

An undertaking of an issuing bank on behalf of the applicant (buyer/importer), in favour of the beneficiary (seller/exporter), to make payment on presentation of documents, provided they are in compliance strictly as per the LC terms (Complying Presentation).

General Considerations

- LC is akin to a bank guarantee ensuring payment on presenting required documents.

- LC is not negotiable.

- LC is a device ensuring payment in trade — it is not a flexible agreement, a bank loan, or a local trade mechanism.

Advantages of LC

For Buyer:

- No upfront payment needed.

- Can secure credit due to bank guarantee.

- Can set quality checks and conditions to safeguard interests.

For Seller:

- Guaranteed payment upon meeting LC terms.

- Can get immediate payment post-shipment by negotiating bills with a local bank.

Features of LC

- Documentary Credit: LC is fundamentally a credit based on documents, not the physical goods.

- Separate Contract: The LC is independent of the underlying sale-purchase contract between the buyer and seller. The bank doesn't care if the actual goods are defective or if there's a dispute between buyer/seller. If the documents match the LC terms exactly, the bank must pay.

- Deal in Documents: As per Article 5 of UCP 600 (Uniform Customs and Practice for Documentary Credits), banks deal with documents and not with goods, services, or performance to which the documents may relate. if the documents are correct, the bank pays, regardless of the actual condition of the goods.

The LC is like a referee at a game. The referee (bank) only checks if the rules (documents) are followed — they don't care who's winning or if players have a personal grudge. Their job is just to enforce the document rules.

Documents under a Letter of Credit

Principles

- Strict Compliance: All parties must adhere to LC terms and conditions. Any deviation can lead to liability or non-payment. As noted by Lord Sumner: Documents should exactly match LC requirements.

- Independent Nature: LC operates separately from the underlying sales contract.

Issuing Bank's Duty

- Ensure presented documents align with customer instructions.

- Failure to ensure compliance results in no reimbursement or remuneration for the bank.

Essential LC Documents

- Bill of Exchange:

- Payment instrument.

- Only the beneficiary can draw it.

- Should align with LC terms like amount and due date.

- Invoice:

- Describes sale details.

- Must match LC conditions exactly. Deviations can lead to rejection.

Transport Documents

- Dictated by sales contract terms.

- Bill of Lading: Proves sea shipment of goods.

- Types: Traditional and Combined/Multimodal Transport.

- Represents ownership of goods.

- Multiple originals — banker should obtain all.

- Airway Bill: Proves goods received by airline; not a title to goods.

- Post/Courier Receipts: Proves goods entrusted for postal or courier transport.

Insurance Documents

- Ensures goods are insured as per LC.

- Policy details must match LC requirements.

Other Documents

- Examples: certificates of origin, weight, quality, etc.

- Must adhere strictly to LC terms.

Operation of Letter of Credit

The lifecycle of an LC involves several distinct steps and parties:

Parties Involved

- Applicant: Buyer / Importer who requests the LC.

- Issuing Bank: Buyer's bank that opens the LC.

- Beneficiary: Seller / Exporter in whose favor the LC is issued.

- Advising Bank: Bank in the seller's country that authenticates and delivers the LC.

- Nominated Bank: Bank authorizing to negotiate or pay the documents. (Often the same as Advising Bank).

Parties & Obligations

The LC ecosystem involves multiple banks and parties, each with specific roles and liabilities.

1. Applicant (Buyer/Importer)

- The person who requests the LC to be established.

- Obligation: To make payment against documents.

- Critical Rule: Must pay even if goods are defective or not received, provided the documents are compliant. (LC deals in documents only).

Why this matters: The buyer cannot refuse payment by saying "the goods were damaged." Their only recourse is to sue the seller separately. This is why LC is called a "documentary credit" — banks only verify papers, not cargo.

2. Issuing / Opening Bank

- The bank that issues (opens) the LC.

- Liability: Has to make payment to the nominated bank on the due date upon receipt of compliant documents.

- Time Limit: Must check documents within 5 banking days following the date of presentation.

Why this matters: The issuing bank takes on the risk of the buyer. If the buyer goes bankrupt, the bank still pays the seller. This is why banks assess buyer creditworthiness before opening an LC.

3. Advising Bank

- The bank in the exporter's country.

- Role: Verifies the genuineness of the LC and advises it to the beneficiary.

- Liability: Not liable for delays due to force majeure (riots, war, etc.).

- Amendments: Any subsequent investigation or amendment must be routed through the same advising bank.

Why this matters: The advising bank protects the seller from fake LCs. They verify the issuing bank's authenticity without taking on payment liability themselves.

4. Beneficiary (Seller/Exporter)

- The person in whose favor the LC is issued.

- Obligation: Must present documents strictly as per LC terms to the nominated bank.

- Time Limit: Must submit documents within the validity period for negotiation, or maximum 21 days from the date of shipment (whichever is earlier).

Why this matters: Even a minor error (wrong date format, spelling mistake) can lead to payment rejection. This is called "strict compliance" — the seller must match documents to LC terms exactly.

5. Nominated / Negotiating Bank

- The bank authorized to negotiate the documents.

- Role: Examines documents and makes payment (negotiates) to the beneficiary.

- Time Limit: Must determine compliance within 5 banking days.

- Claim: Claims reimbursement from the opening bank.

Why this matters: The nominated bank is the seller's "cash counter." They pay the seller upfront and later collect from the issuing bank. This gives sellers immediate liquidity.

6. Confirming Bank

- A bank that adds its confirmation to the LC (usually at the request of the opening bank).

- Liability: Undertakes the same liability as the opening bank (guarantees payment if opening bank defaults).

Why this matters: If the buyer's country is politically unstable or the issuing bank is unknown, the seller may demand confirmation from a trusted international bank as backup.

7. Reimbursing Bank

- Bank authorized by the opening bank to provide reimbursement (funds) to the nominated or confirming bank.

Why this matters: For speed and convenience — instead of waiting for funds from the issuing bank, the nominated bank gets immediate payment from a designated reimbursing bank (often in a major financial hub).

Process of LC

Types of Letter of Credit

LCs can be classified based on their operation, security, and obligations.

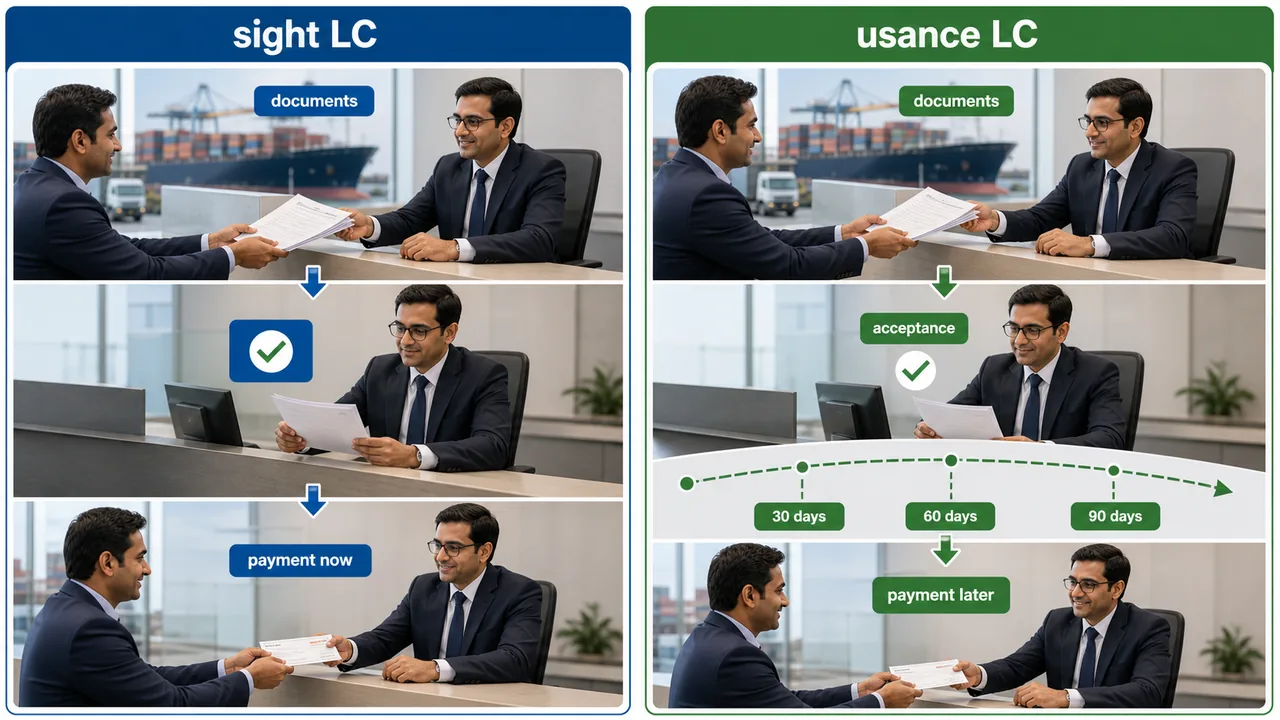

1. Sight vs Usance LC

Sight LC = Payment immediately when documents are presented

- Flow: Seller submits documents → Bank checks them → Pays instantly (within 5 banking days)

- Think of it like cash on delivery

Usance LC = Payment after a delay (credit period)

- Flow: Seller submits documents → Bank accepts them → Pays after 30/60/90/180 days

- Think of it like buy now, pay later

| Type | Payment | Also Known As | Benefit |

|---|---|---|---|

| Sight LC | Immediately on document presentation | DP-LC (Documents against Payment) | Seller gets paid fast |

| Usance LC | After agreed period (30-180 days) | DA-LC (Documents against Acceptance) | Buyer gets credit time |

2. Revocable vs Irrevocable LC

- Revocable LC: Can be cancelled or amended without the consent of the beneficiary. However, if the nominated bank has already taken up documents, the issuing bank must reimburse them.

- Irrevocable LC: Can be cancelled or amended only with the consent of the beneficiary, issuing bank, and confirming bank.

- Note: If "Revocable/Irrevocable" is not stated in the LC, it is treated as Irrevocable (as per UCP 600).

3. Revolving LC

- Provides for repeated negotiation, subject to payment of previous documents by the applicant.

- Used like a running account (similar to Cash Credit / Overdraft).

- The LC amount gets restored either automatically or upon specific request once the previous utilization is settled.

3. Recourse vs Without Recourse

Recourse means liability.

- With Recourse: The risk of non-payment falls on the beneficiary (drawer).

- Without Recourse: The risk of non-payment falls on the nominated bank. The beneficiary is not liable if the issuing bank fails to pay.

4. By Mode of Payment

- Acceptance Credit LC: Bill of exchange or draft. Payable upon acceptance, at the future date, subject to receipt of documents confirming to the terms and conditions of LC.

- Deferred Payment LC: Similar to acceptance credit, except that there is no bill of exchange or draft.

- Negotiation Credit LC: Issuing bank undertakes to make payment to the bank which has negotiated the document.

5. Special Types of LC

- Confirmed LC: A guarantee added by another bank (Confirming Bank) in addition to the opening bank. It gives double security to the exporter.

- Standby LC: Issued in lieu of a Bank Guarantee. It is the "Most Risky" type (for the bank). Governed by ISP-98 (International Standby Practices).

- Instalment LC: Allows shipment in instalments. Critical Rule: If one shipment is not made on time, the LC expires for that and all future shipments.

6. Advance & Transferable LCs

- Red Clause LC:

- Provides for an advance (pre-shipment loan) to the beneficiary before presentation of documents.

- The advance is adjusted from the final payment.

- Risk: The risk is borne by the applicant and opening bank.

- Green Clause LC:

- An extension of Red Clause LC.

- It provides for warehouse storage of goods before sale + advance.

- Risk: The risk is borne by the applicant and opening bank.

Red Clause vs Green Clause LC

| Points | Red Clause LC | Green Clause LC |

|---|---|---|

| What are they? | Allows the exporter an advance payment for working capital to purchase raw materials, process, and package goods | Extension of Red Clause LC. Allows additional advances for pre-shipment warehousing at the port of origin and insurance expenses |

| When Advance is Given? | Bank provides advance payment before the seller ships the goods | Advance is granted only after purchased goods are stored in bonded warehouses |

| Document Requirements | Written undertaking and receipts | Written undertaking, receipts, and additional documents |

| Proportion of Advance | 20% to 25% of the face value of the LC | 75% to 80% of the face value of the LC |

| Security | Riskier for the buyer as the advance is extended even before production begins | More secure for the importer as advance is given against the document of title |

- Transferable LC:

- Can be transferred in full or in part to another party (Second Beneficiary) at the request of the Original Beneficiary.

- Limit: Can be transferred only once.

- Back to Back LC:

- A 2nd LC issued on the security of the original (Master) LC.

- Used when the supplier is different from the beneficiary. -Terms are same except for the price (profit margin).

Practice Questions

- When provision for pre-shipment credit is made in LC, it is called Red Clause LC.

- LC issued on strength of original LC is called Back to Back LC.

- LC issued in place of a bank guarantee is called Standby LC.

- Transferable LC, can be transferred how many times? Only Once.

- Irrevocable LC can be cancelled or amended with consent of Issuing Bank, Confirming Bank (if any) and Beneficiary.

- Confirmed LC is an LC where Confirming Bank adds its confirmation.

- If the exporter wants warehouse storage facility, he should insist on Green Clause LC.

- LC which provides for repeated negotiations: Revolving LC.

- Documents are delivered to applicant on receipt of payment in case of Sight LC.

- Beneficiary wants to get an LC where after negotiation of documents, he should not be made to repay back the amount. Which LC is suitable? Without Recourse LC.

- Most safe LC from the perspective of the beneficiary? LC which provide 3 facilities:Confirmed, Non-revocable, Non-recourse

Uniform Customs & Practices for Documentary Credits (UCPDC 600)

UCP 600 (w.e.f. July 1, 2007) is a set of universally recognized rules prepared by ICC-Paris to regulate LC transactions.

Key Changes from UCP 500 to UCP 600

- Approved on 25 October 2006.

- Article count decreased: 49 (UCP 500) → 39 (UCP 600) — a reduction of 10 articles.

- Introduced articles for 'Definitions' and 'Interpretations'.

- Replaced 'reasonable time' with a fixed 5 banking days for document acceptance/refusal.

- Introduced rules for discounting deferred payment credits (new provisions).

- Defined negotiation as the 'purchase' of drafts/documents.

- Integrated the 12 Articles from the eUCP supplement for electronic document presentation.

General Rules

- Application: Applicable if the LC text expressly states it.

- Conflict: If LC terms and UCP 600 rules contradict, the LC terms will prevail.

- Dates: Documents dated earlier than the LC date are acceptable, but not after.

- Branches of a bank in different country, to be treated as different banks.

Payment under LC — Primary Obligation for Banks

UCP Articles Overview

- Articles 6-13: Discuss liabilities & responsibilities in letter of credit transactions.

- Articles 14-17: Examine documents for discrepancies before payment.

- General Principle: Banks have a primary obligation to pay under a Letter of Credit regardless of the underlying contract.

Important Case Laws

Case 1: Tarapore & Co. vs V/O Tractors Export

- Situation: Indian firm claims Russian machinery is unsatisfactory. Wants to prevent payment through LC.

- Decision: Supreme Court upheld the importance of irrevocable LCs in international trade, refraining from interfering unless exceptional circumstances exist.

- Key Takeaway: LCs are independent of sales contracts. Courts avoid interfering with LC autonomy.

Case 2: United Commercial Bank vs Bank of India

- Situation: Discrepancy in goods description results in payment "under reserve". Bank demands refund.

- Decision: The Supreme Court reaffirms that:

- LC is the sole contract with the banker; underlying disputes don't matter.

- Bankers need to strictly comply with the LC and their customer's instructions.

- It's the bank's duty to refuse payment if documents aren't as per LC.

- The banking system relies on the absolute obligation of confirmed LCs to pay.

- Courts only interfere in exceptional cases like clear fraud.

1. Tolerances

| LC Provisions | Tolerance |

|---|---|

| Amount, quantity, price mentioned as 'about' or 'approximate' | 10% plus or minus. (e.g. LC value USD 10000 appx → USD 9000 to 11000 allowed) |

| Quantity not specified in terms of stipulated no. of packing units or individual items | 5% plus or minus. (Provided total amount is within LC limit) |

2. Time Interpretations

| Term | Meaning / Period |

|---|---|

| Date specified as 'on and about' | 5 calendar days before or after. |

| "Beginning of month" | 1st to 10th of the month. |

| "Middle of month" | 11th to 20th of the month. |

| "End of month" | 21st to last day of the month. |

| "1st half of the month" | 1st to 15th of the month. |

| "2nd half of the month" | 16th to last day of the month. |

| Expiry on Holiday | If LC expires on a closed day, it is extended to the next banking day. |

3. Insurance Rules

- Value: If not stated, must be at least 110% of CIF (Cost/Insurance/Freight) value/CIP (Cost/Insurance/Port) value.

- Currency: Must be the same as the LC currency.

- Date: Insurance policy dated subsequent to date of shipment can be accepted, provided cover is effective from date of shipment.

- Example: Date of shipment Jan 20. Policy dated Jan 22 can be accepted, if effective from Jan 20.

4. Other Important Provisions

- Trans-shipment: Acceptable if the transport document states it will take place, even if LC prohibits it!

- Clean Transport Doc: Bank accepts only "clean" documents (no clause declaring defective goods/packaging).

- Force Majeure: Banks assume NO liability for consequences arising from Acts of God, riots, wars, strikes, etc., or for loss of documents in transit.

- Unsolicited Docs: Documents submitted but not required by LC will be disregarded.

- Transportation Loss: Banks assume NO liability for loss of documents in transit.

Bill of Lading (BL)

A Bill of Lading (BL) is a document issued by a carrier (or their agent) to acknowledge receipt of cargo for shipment. In LC transactions, it serves three key functions:

- Receipt of Goods: Proof that the carrier has received the goods.

- Document of Title: It represents ownership of the goods. If negotiable, possession of the original BL allows transfer of ownership.

- Contract of Carriage: Evidence of the contract between shipper and carrier.

Types of Bill of Lading

The Bill of Lading is a critical document of title. Banks look for specific types:

1. Clean BL

- Feature: No mention of defective packing of goods.

- Status: Valid document for negotiation.

2. Claused / Dirty BL

- Feature: Explicitly mentions defective packing of goods.

- Status: Defective document for negotiation (Banks generally reject unless LC permits).

3. Stale BL

- Feature: Presented after the validity period expired (or after 21 days from shipment if no period specified).

- Status: Defective document for negotiation.

4. On-board BL

- Feature: Contains a specific confirmation/notation that goods have been put on board the ship (shipped on board).

- Status: Preferred for negotiation as it proves shipment has occurred.

Summary Cheat Sheet

| Concept | Key Fact / Answer |

|---|---|

| UCP Framed By | ICC (International Chamber of Commerce), Paris. |

| Current UCP Ver. | UCP 600 (Applicable from 01.07.2007). Approved 25 Oct 2006. |

| UCP Articles | 39 articles (reduced from 49 in UCP 500). |

| Negotiation (UCP 600) | Defined as the 'purchase' of drafts/documents. |

| Object of Dealings | In LC, all parties deal in Documents, not goods/services. |

| LC Nature | LC is not negotiable. Independent of underlying sales contract. |

| "About" Amount/Qty | ± 10% tolerance allowed. |

| Qty (No Units) | ± 5% is allowed (if no specific packing units mentioned). |

| "On or about" Date | 5 calendar days before or after the specified date. |

| "Beginning of Month" | 1st to 10th of the month. |

| "Middle of Month" | 11th to 20th of the month. |

| "First Half of Month" | 1st to 15th of the month. |

| Submission Limit | Beneficiary must submit docs within 21 days of shipment. |

| Checking Time | Negotiating/Opening banks get 5 banking days to check docs. |

| Insurance Value | Minimum 110% of CIF/CIP value (if not stated). |

| Insurance Currency | Must be the same as the LC currency. |

| UCP Art. 6-13 | Liabilities & responsibilities in LC transactions. |

| UCP Art. 14-17 | Document examination for discrepancies. |

| eUCP Supplement | 12 articles for electronic document presentation. |

| Claused BL | BL mentioning defective packing (Defective for negotiation). |

| Airway Bill | Not a title to goods (unlike Bill of Lading). |

| Confirming Bank | The bank that gives a guarantee of payment for the opening bank. |

| Buyer's Liability | Applicant MUST pay against compliant docs, even if goods defective. |

| Without Recourse | Beneficiary not made to repay after negotiation. |

| Transferable LC | Can be transferred only once. |

| Standby LC | Substitute for Bank Guarantee (Risk on Bank). |

| Instalment LC | If one shipment missed, LC expires immediately. |

| Red Clause Advance | 20-25% of face value of LC. |

| Green Clause Advance | 75-80% of face value of LC. |

| Acceptance Credit LC | Payment via bill of exchange at a future date. |

| Deferred Payment LC | Like acceptance credit but no bill of exchange. |

| Court Interference | Courts interfere with LC obligations only in cases of clear fraud. |

Lesson Doubts

Ask questions, get expert answers