📦 Export Credit & Import Payments

Complete guide to trade finance - pre-shipment and post-shipment credit, packing credit loans, import payments, trade credit, and ECGC coverage

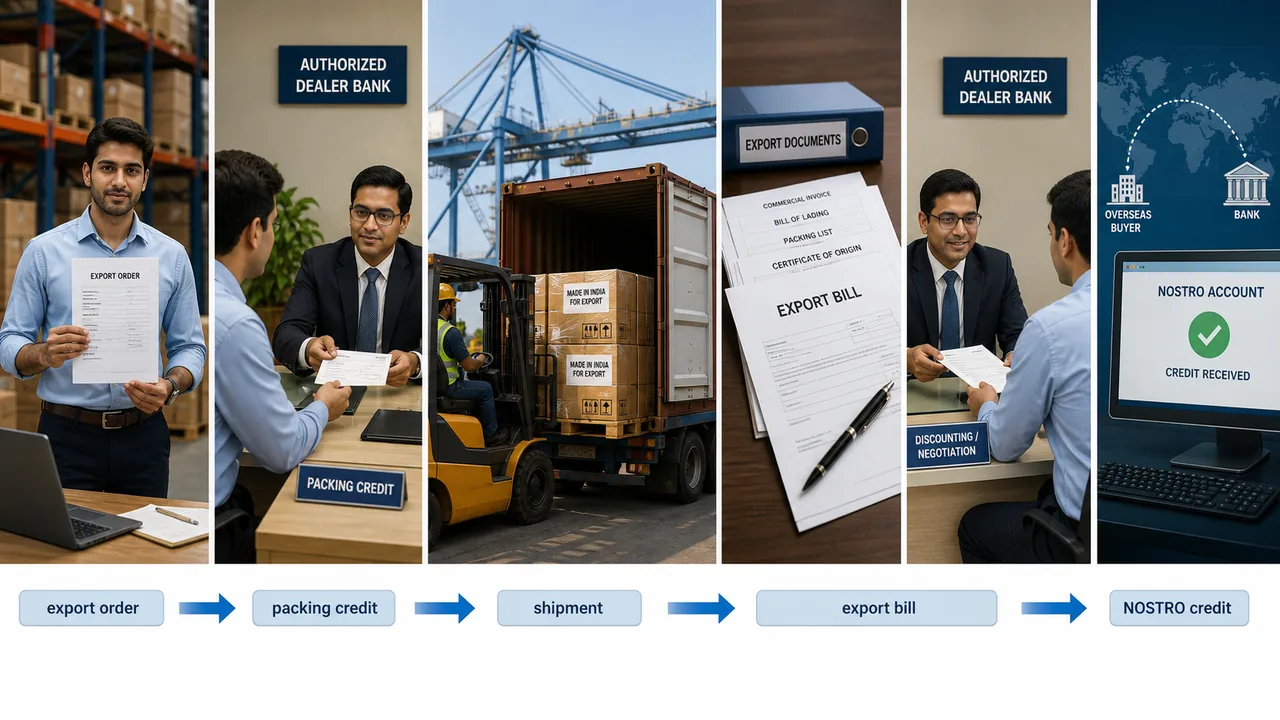

Overview of Export Credit

Export credit is a specialized form of trade finance provided to exporters to support their export activities. These are working capital advances that help exporters manufacture, process, and ship goods to foreign buyers.

Export credit can be:

- Pre-shipment Credit (Packing Credit)

- Post-shipment Credit

Pre-shipment Credit (Packing Credit)

Pre-shipment credit is given to exporters for the manufacture and shipment of goods before they are actually exported.

Eligibility Criteria

Pre-shipment credit is given to exporters who:

| Requirement | Details |

|---|---|

| IEC Number | Must have Import Export Code issued by DGFT (10-digit code) |

| RBI Caution List | Must NOT be on RBI's caution list |

| ECGC Approval | Must NOT be on ECGC's approval list (specific approval list) |

| Export Order | Must have a confirmed export order with them |

📌 IEC (Import Export Code) is a 10-digit unique identification number issued by the Directorate General of Foreign Trade (DGFT), mandatory for any person/entity engaged in import/export activities.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Overview of Export Credit

Export credit is a specialized form of trade finance provided to exporters to support their export activities. These are working capital advances that help exporters manufacture, process, and ship goods to foreign buyers.

Export credit can be:

- Pre-shipment Credit (Packing Credit)

- Post-shipment Credit

Pre-shipment Credit (Packing Credit)

Pre-shipment credit is given to exporters for the manufacture and shipment of goods before they are actually exported.

Eligibility Criteria

Pre-shipment credit is given to exporters who:

| Requirement | Details |

|---|---|

| IEC Number | Must have Import Export Code issued by DGFT (10-digit code) |

| RBI Caution List | Must NOT be on RBI's caution list |

| ECGC Approval | Must NOT be on ECGC's approval list (specific approval list) |

| Export Order | Must have a confirmed export order with them |

📌 IEC (Import Export Code) is a 10-digit unique identification number issued by the Directorate General of Foreign Trade (DGFT), mandatory for any person/entity engaged in import/export activities.

📌 Export Credit Guarantee Corporation (ECGC) maintains a "Specific Approval List (SAL)" which acts as a warning database. It contains the names of exporters who have defaulted on previous loans or are currently involved in legal disputes regarding credit.

Key Parameters of Pre-shipment Credit

| Parameter | Details |

|---|---|

| Period | At bank's discretion (with reference to date of shipment) |

| Amount | Linked to FOB (Free on Board) value - i.e., the cost involved up to putting the goods on board the ship |

| Type of Account | Normally, a demand loan |

| Running Account | Available for good exporters, 100% EOU (Export Oriented Unit), SEZ (Special Economic Zone) units, EPZ (Export Processing Zone) units |

💡 FOB Value includes cost of goods + packing + inland transportation + loading charges up to the ship. It does NOT include freight and insurance (which are buyer's responsibility in FOB terms).

📌 Demand Loan vs Running Account: Normally, pre-shipment credit is a demand loan (one loan per order → export → repay → close). Trusted exporters (EOU, SEZ, EPZ) can get a running account - a revolving credit line to draw against multiple orders, adjusted on FIFO (First In First Out) basis.

Special Provisions for PCL (Packing Credit Loan)

PCL to Sub-suppliers:

- Can be allowed to sub-suppliers

- But running account facility cannot be extended to sub-suppliers

PCL Above FOB Value:

- Allowed for certain commodities with bye-products (e.g., de-oiled cakes)

- Must be liquidated within 30 days

📌 Example: An exporter of groundnuts may get PCL above FOB for the de-oiled cake (bye-product) generated during processing. This extra amount must be repaid within 30 days.

Adjustment of Packing Credit

Packing credit can be adjusted from:

- Proceeds of post-shipment advance (most common)

- From EEFC account (Exchange Earners' FC account)

- Proceeds of other export bills not financed by the bank

For Running Account:

- Adjustment on FIFO (First In First Out) basis

- Individual advance should not outstand for more than 360 days

⚠️ Important: If an individual packing credit advance remains outstanding for more than 360 days, it may be classified as irregular and attract higher interest rates.

Post-shipment Credit

Post-shipment credit is given against export receivables - i.e., after goods have been shipped but payment is yet to be received from the foreign buyer.

Types of Post-shipment Credit

| Method | Description |

|---|---|

| 1. Purchase/Discount of FC export bills | Bank buys the export bill and pays the exporter immediately |

| 2. Negotiation of bills under LC | Bank negotiates (pays) bills drawn under Letter of Credit |

| 3. Advance against bills under collection | Advance given while bill is sent for collection |

| 4. Overdraft against duty drawback claims | Advance against pending government duty refunds |

| 5. Advance against un-drawn balances | Advance for balance amount to be received later |

📌 Example: ABC Exports ships goods worth USD 100,000 to a US buyer. Instead of waiting 60 days for payment, they get the bank to discount the export bill. Bank pays them immediately (minus discount charges) and collects from the buyer later.

Interest Rates on Export Credit

Rate of Interest

| Parameter | Details |

|---|---|

| ROI on Pre-shipment Credit | Bank's discretion, but not below MCLR |

| ROI on Post-shipment Credit | Bank's discretion, but not below MCLR |

| Additional interest for ad-hoc limits | No additional interest charged |

MCLR = Marginal Cost of Funds Based Lending Rate (the minimum rate below which banks cannot lend)

If Export Does Not Take Place

- If export does not take place for 1 year from date of advance

- Commercial ROI (higher rate) is charged from the date of advance

- This acts as a penalty for non-performance

Interest Equalization Scheme (IES) (Subvention)

The government provides interest subsidy to select exporters to make Indian exports competitive:

| Beneficiary | Subvention Rate |

|---|---|

| Regular exporters | 2% interest subvention |

| MSMEs (Micro, Small & Medium Enterprises) | 3% interest subvention |

⚠️ Update (28.08.25): ROI by bank = Repo rate + 4%. Subvention to be claimed monthly from Central Govt. through RBI.

How it works:

- Banks claim the subvention monthly from Central Government through RBI

- Exporters get the benefit of reduced interest cost

- Subvention applies on both pre-shipment and post-shipment credit

Post-shipment Credit (Detailed)

Types of Post-shipment Loans

| Type | Description |

|---|---|

| (a) Purchase of FC demand bills | Bank buys demand bills (immediate payment) |

| (b) Discount of FC usance bills | Bank discounts time bills (deferred payment) |

| (c) Advance against duty drawback claims | Advance against pending government refunds |

Normal Transit Period (NTP)

What is NTP?

NTP is the time it takes for funds to reach the bank after the export bill is purchased/negotiated:

Exporter submits bill → Bank purchases bill → Bill sent abroad → Foreign bank pays →

Credit received in Indian bank's NOSTRO account

NTP = Period from date of purchase/negotiation to date of credit in bank's NOSTRO account

| Bill Type | NTP Period |

|---|---|

| Demand bills | NTP fixed by FEDAI (normal = 25 days). Differs for specific exports |

� Why NTP matters: Bank gives exporter money TODAY, but receives payment from foreign buyer after 25 days. NTP accounts for this gap (document transmission, processing, fund transfer time). Exporter submits bill to SBI → SBI purchases bill & pays exporter → Bill sent to US bank → US bank collects from buyer → USD credited to SBI's NOSTRO account (SBI's account with Bank of America)

Period for Usance Bills Discounting

| Exporter Type | Maximum Period |

|---|---|

| Warehouse exporters | 15 months |

| All other exporters | 9 months (was 15M for exports till 31.7.20 (due to COVID-19)) |

Treatment of NTP in Usance Bill:

- NTP to be added in usance period while calculating due date

- If usance period is 90 days, due date = 90 + 25 days = 115 days

Usance = Credit period given to the buyer to pay for goods. 📌 Example: An exporter ships goods on 90-day usance. The buyer pays after 90 days from bill acceptance. But bank adds NTP (25 days) for transit, so total period = 115 days from date of purchase.

Documents Submission

- Documents should be submitted within 21 days from date of shipment

- Documents should include EDF/SOFTEX form

EDF = Export Declaration Form (for physical goods export) SOFTEX = Software Export form (for software/IT exports)

Crystallization of Overdue Bills

What is Crystallization?

- FC liability to be converted to rupee liability by selling FC back to the exporter

- Done at TT Selling Rate

- Purpose: To stop exchange fluctuation risk

| Aspect | Details |

|---|---|

| Period for crystallization | Decided by bank (earlier FEDAI) |

| Effect | Stops FC risk, converts to INR loan |

📌 Example: If export bill remains unpaid for too long, bank crystallizes the FC amount (say USD 10,000) into INR at current TT Selling Rate. Now exporter owes INR, eliminating forex risk for bank.

Advance Against Undrawn Balances

- Maximum 10% of value of export bills

- For amounts to be received later (e.g., commission adjustments)

RBI Reporting

| Aspect | Details |

|---|---|

| System | Integrated with EDPMS from HY Dec 2015 |

| Earlier reporting | HY Report to RBI on Form XOS, within 15 days |

EDPMS = Export Data Processing and Monitoring System

Adjustment of Post-shipment Credit

Post-shipment credit can be adjusted from:

- Proceeds of bills received from abroad for goods exported

- EEFC account

- Proceeds of any other unfinanced (collection) bill

Gold Card Scheme for Exporters

Banks provide preferential treatment to creditworthy exporters through the Gold Card Scheme:

Eligibility for Gold Card

| Requirement | Details |

|---|---|

| (a) Creditworthy exporters | 3 years standard account track record |

| (b) Not on caution/black list | Must not be on RBI/ECGC caution or black list |

| (c) No losses | Have not incurred loss during last 3 years |

Gold Card Benefits

| Parameter | Details |

|---|---|

| Amount | Need-based, on projected export turnover |

| Standby Limit | Minimum 20% of assessed limit |

| Application Disposal | Fresh: 25 days, Renewal: 15 days, Ad-hoc: 7 days |

| Concessional ROI | At bank discretion |

| In-principle Sanction | Valid for 3 years (subject to annual review) |

| Pre-shipment in FC | Preference for granting pre-shipment in FC |

📌 Example: XYZ Exports has maintained a standard account for 4 years with no losses. They apply for Gold Card and get a limit of Rs.5 crore based on projected exports. They also get a 20% (Rs.1 crore) standby limit for unexpected needs, processed in just 7 days.

ECGC Whole Turnover Policy

ECGC (Export Credit Guarantee Corporation) provides credit guarantee to cover export loans:

| Aspect | Details |

|---|---|

| Purpose | To cover the loan under credit guarantee |

| Coverage | Whole turnover (pre-shipment or post-shipment) |

| Requirement | Information should be sent to ECGC within prescribed period |

Why it matters:

- If exporter defaults on the loan

- ECGC compensates the bank (partial coverage)

- This reduces risk for banks in export financing

💡 ECGC coverage encourages banks to lend to exporters, as a portion of the risk is covered by the guarantee.

Comparison: Pre-shipment vs Post-shipment Credit

| Feature | Pre-shipment (Packing) Credit | Post-shipment Credit |

|---|---|---|

| When given | Before shipment | After shipment |

| Purpose | Manufacture & ship goods | Cover receivables |

| Security | Export order | Export bill/LC |

| Amount basis | FOB value | Bill value |

| Account type | Demand loan (usually) | Purchase/discount of bills |

| Max period | 360 days (running a/c) | Bill tenure + NTP |

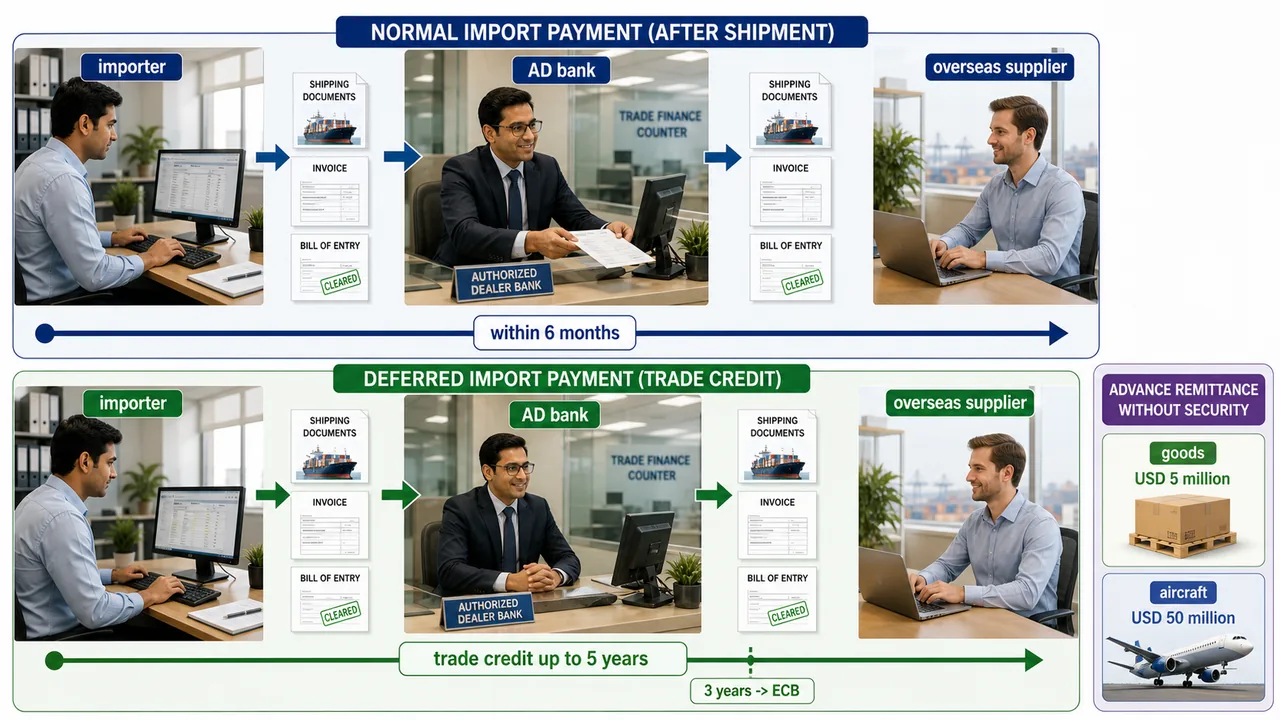

Import Payments

Import payments are the reverse of export transactions - here, Indian entities pay foreign suppliers for goods/services imported into India. These are regulated by RBI and DGFT.

Basic Requirements for Importers

| Requirement | Details |

|---|---|

| IEC Number | Importer must have Import Export Code issued by DGFT |

| AD Bank | Payments routed through Authorized Dealer (AD) bank |

| Documentation | Bill of Entry, Invoice, and other customs documents required |

📌 IEC (Import Export Code) is the same 10-digit code used for both imports AND exports, issued by DGFT.

Time Limit to Settle Import Payments

| Type of Arrangement | Maximum Period | Notes |

|---|---|---|

| Normal course | 6 months from date of shipment | Standard timeline for most imports |

| Deferred payment arrangement | Up to 5 years | Called Trade Credit (explained below) |

💡 Date of shipment = Date on Bill of Lading (B/L) or Airway Bill (AWB)

Import of Foreign Currency (Physical FC)

| Aspect | Details |

|---|---|

| Ceiling | No ceiling on import of FC |

| Declaration requirement | Subject to declaration on Form CDF to Customs |

| Mandatory declaration | If aggregate value > USD 10,000 OR FC notes value > USD 5,000 |

⚠️ Form CDF = Currency Declaration Form - must be filled at customs if carrying FC above threshold

Import of INR (From Nepal & Bhutan)

| Aspect | Details |

|---|---|

| Countries allowed | Nepal & Bhutan only |

| Amount limit | Any amount can be brought |

| Denomination rule | Highest denomination allowed: Rs.500 |

| Special rule | If amount > Rs.25,000: highest denomination = Rs.100 |

📌 This restriction prevents high-value INR notes from circulating outside India's banking system.

Advance Remittance for Imports (Without BG/LC/LoU/LoC)

Banks can allow advance remittance without security (Bank Guarantee, Letter of Credit, Letter of Undertaking, Letter of Comfort) based on creditworthiness:

| Type of Import | Maximum Advance (Without BG/LC) |

|---|---|

| Import of goods | USD 5 million |

| Aircraft / Helicopter / Aviation | USD 50 million |

| Import of services | At bank's discretion |

💡 Why higher for aviation? Aircraft are high-value assets with strong resale value, reducing bank risk.

Trade Credit for Imports

Trade credit is credit extended by overseas suppliers/banks for import of goods into India.

Types of Trade Credit

| Type | Arranged By | Maximum Period | Notes |

|---|---|---|---|

| Buyer's Credit | Buyer (Indian) | Less than 3 years | Credit from overseas bank |

| Supplier's Credit | Overseas supplier | Less than 3 years | Credit directly from seller |

⚠️ Important: If credit period is 3 years or above, it becomes part of ECB (External Commercial Borrowing) and different rules apply.

Merchant Trade Transactions (MTT)

Merchant trade = Goods purchased from one country and sold to another without entering India.

Key Conditions:

| Condition | Details |

|---|---|

| (1) Goods entry | Goods NOT entering domestic tariff area (India) |

| (2) No transformation | No transformation of goods (just trading) |

| Completion timeline | Transaction to be completed within 9 months |

| Forex outlay | Maximum 4 months from date of foreign exchange payment |

| Advance payment (no BG/LC) | Maximum USD 500,000 per transaction |

| Caution listing | If outstanding > 5% of export earnings → caution listed |

📌 Example: An Indian trader buys goods from China and sells directly to a buyer in USA. Goods never enter India - this is merchant trade.

Evidence of Import of Goods

Remittance for imports can be made on the basis of proof of import:

| Evidence Type | Details |

|---|---|

| (1) Bill of Entry | Filed on IDPMS platform |

| (2) Custom Assessment Certificate | Issued by customs authorities |

| (3) Postal Appraisal Form | For goods imported by post |

Special Rules for Evidence of Import

| Rule | Details |

|---|---|

| Evidence in lieu of BoE | Not mandatory for physical imports up to USD 1 lakh |

| Extension in submission of BoE | ADs to enter information in IDPMS |

| Preservation by AD | Evidence of import to be preserved for minimum 1 year |

| Non-submission of BoE | Banks to follow up for 3 months. Atleast 1 registered letter required |

IDPMS = Import Data Processing and Monitoring System (counterpart of EDPMS for imports)

Payment of Documents Directly Received by Importer

| Importer Type | Maximum Amount (Direct Payment) |

|---|---|

| Normal course | USD 300,000 |

| Limited companies | No ceiling |

| Status holder exporters | No ceiling |

| Wholly owned subsidiary of foreign company | No ceiling |

💡 Status Holder = Exporter who has earned a certain level of export earnings over past years (recognized by DGFT)

Status Holders (Foreign Trade Policy 2023 Update)

As per Foreign Trade Policy 2023, categorization of Status Holders depends on total FOB (FOR for deemed exports) export performance during the current plus preceding 3 years (taken together) upon exceeding the limit below. (For Gem and Jewellery sectors, it is 2 preceding years).

Star Export House Thresholds (FOB Value in USD Million):

| Status Category | Export Performance Threshold (USD Million) |

|---|---|

| One Star Export House | 3 |

| Two Star Export House | 15 |

| Three Star Export House | 50 |

| Four Star Export House | 200 |

| Five Star Export House | 800 |

Crystallization of Overdue Import Bills under LC

| Aspect | Details |

|---|---|

| Decision | At discretion of bank |

| Exchange rate | Bills Selling Rate (not TT Selling Rate) |

| Purpose | Convert FC liability to INR, stop forex risk |

📌 Difference from Export Crystallization: Export uses TT Selling Rate, Import uses Bills Selling Rate.

Summary Cheat Sheet

Export Credit - Key Numbers

| Parameter | Value / Details |

|---|---|

| Running account eligibility | Good exporters, 100% EOU, SEZ units, EPZ units |

| Pre-shipment loan amount basis | FOB (Free on Board) value |

| ROI (Pre & Post-shipment) | Bank discretion, not below MCLR. No additional interest for ad-hoc limits |

| Post-shipment demand bills period | NTP fixed by FEDAI (normal 25 days) |

| Post-shipment usance bills period | Warehouse: 15 months, Others: 9 months |

| Crystallization period | Decided by bank (earlier FEDAI) |

| Overdue bills report to RBI | Form XOS, within 15 days (now EDPMS integrated) |

| Interest subvention rate | 2% (Regular), 3% (MSMEs) w.e.f. 28.08.25 |

| ROI for subvention case | Repo rate + 4% |

| Duty drawback advance | Against pending government duty refund claims |

| No export penalty | If export doesn't happen in 1 year → Commercial ROI from day one |

| Max running account outstanding | 360 days per individual advance |

Gold Card Scheme - Key Numbers

| Parameter | Value |

|---|---|

| Track record required | 3 years standard account |

| Loss condition | No loss in last 3 years |

| Standby limit | Min 20% of assessed limit |

| Fresh application disposal | 25 days |

| Renewal disposal | 15 days |

| Ad-hoc disposal | 7 days |

| In-principle validity | 3 years (annual review) |

Import Payments - Key Numbers

| Parameter | Value / Details |

|---|---|

| Normal settlement time limit | 6 months from date of shipment |

| Trade credit (deferred payment) | Up to 5 years |

| Trade credit → ECB threshold | Credit period ≥ 3 years becomes ECB |

| Advance without BG/LC (goods) | USD 5 million |

| Advance without BG/LC (aircraft) | USD 50 million |

| FC declaration mandatory | Total FC > USD 10,000 OR FC notes > USD 5,000 |

| INR import from Nepal/Bhutan | Max denomination Rs.500 (Rs.100 if amount > Rs.25,000) |

| Merchant trade completion | Max 9 months |

| Merchant trade forex outlay | Max 4 months |

| Evidence of import types | Bill of Entry (IDPMS), Customs Certificate, Postal Appraisal Form |

| BoE not mandatory for | Physical imports up to USD 1 lakh |

| Bank preservation of evidence | Minimum 1 year |

| Direct payment limit (normal) | USD 300,000 (No ceiling for Ltd companies, Status holders) |

| Import crystallization exchange rate | Bills Selling Rate (vs TT Selling Rate for exports) |

Quick Memory Tips

Export Credit

| Concept | Remember As |

|---|---|

| Pre-shipment | Before goods leave → Packing the goods |

| Post-shipment | After goods shipped → Payment awaited |

| FOB value | Freight On Buyer (after FOB, buyer pays) |

| 360 days | Max running account limit (1 year minus 5 days) |

| NTP 25 days | Normal Transit = 25 days (2+5) |

| Crystallization | Crystal clear - FC converted to INR to stop risk |

| Gold Card 3-3 | 3 years track record, no loss for 3 years |

Import Payments

| Concept | Remember As |

|---|---|

| 6 months limit | 6 = normal import settlement (half a year) |

| 5 years trade credit | 5 years max = becomes ECB after 3 years |

| USD 5M / 50M advance | 5M for goods, 50M for aircraft (10x for aviation) |

| USD 10K/5K declaration | 10K total FC OR 5K notes = must declare on CDF |

| 9 months merchant | Merchant trade = 9 months max (think: 3 quarters) |

| 1 year preservation | Bank keeps evidence for 1 year minimum |

| IDPMS vs EDPMS | Import vs Export Data Processing Monitoring System |

Lesson Doubts

Ask questions, get expert answers