💱 Forward Exposure & Unhedged Foreign Currency Exposure (UFCE)

Unhedged Foreign Currency Exposures, UFCE computation, provisioning & capital requirements, forward contracts, AD general/specific directions, user classification, permissible FX derivatives, and pre-settlement risk.

Forward Exposure & Unhedged Foreign Currency Exposure (UFCE)

Introduction — Unhedged Foreign Currency Exposures

- Entities with Foreign Currency (FCY) Exposures are exposed to currency risk.

- If these exposures are not hedged, adverse movements in exchange rates can affect the entity's capacity to service its debt.

- This in turn impacts the credit risk borne by banks lending to such entities.

- RBI requires banks to factor in the risks arising from Unhedged Foreign Currency Exposures (UFCE) of their borrowers.

- Banks must put in place a proper mechanism to:

- Estimate UFCE of borrowers

- Assess the riskiness of such exposures

- Factor this in their credit appraisal, loan pricing, and provisioning

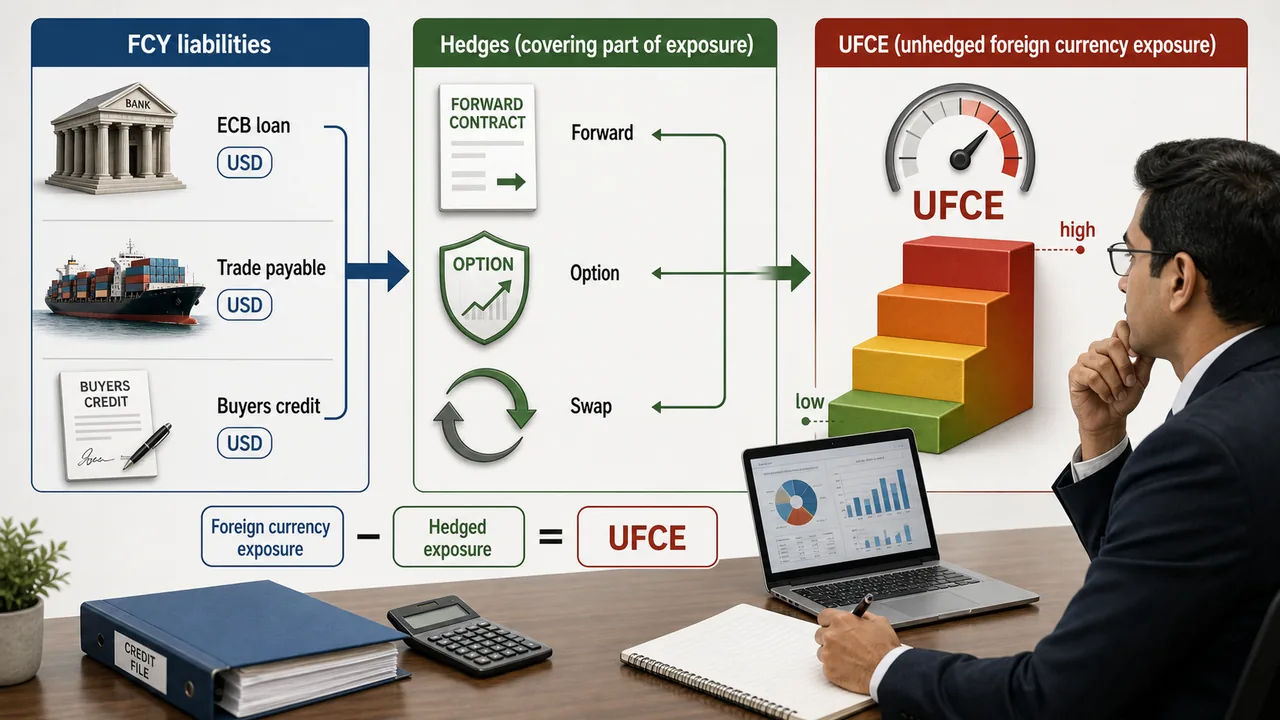

Computation of UFCE

Definition

- UFCE = Total FCY Exposure − FCY Hedged Exposure

- Only financial hedges (forward contracts, options, swaps) are considered, not natural hedges for this computation.

Natural Hedge

- A natural hedge exists when a borrower has FCY earnings that can offset FCY liabilities.

- Example: An exporter with dollar receivables and dollar loans — the receivables naturally offset the loan exposure.

- RBI's guidelines focus on financial hedges (derivatives) for UFCE computation, but banks may consider natural hedges in their internal credit assessment.

Steps in UFCE Estimation

- Identify all FCY liabilities (ECB, FCNR loans, buyer's credit, trade payables, etc.)

- Identify all FCY hedges (forward contracts, options, swaps)

- Compute UFCE = FCY Liabilities − FCY Hedges

- Express UFCE as a percentage of the entity's total equity or EBID (Earnings Before Interest & Depreciation)

UFCE Ratio

- UFCE as % of EBID is the key ratio used for provisioning and capital adequacy computation.

- Higher UFCE/EBID ratio → higher risk → higher provisioning and capital charge.

Provisioning and Capital Requirements for UFCE

Incremental Provisioning

Banks must maintain incremental provisioning for borrowers with UFCE:

🔐

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

Pro

Popular Save ₹100/mo

₹ 99 /mo

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Forward Exposure & Unhedged Foreign Currency Exposure (UFCE)

Introduction — Unhedged Foreign Currency Exposures

- Entities with Foreign Currency (FCY) Exposures are exposed to currency risk.

- If these exposures are not hedged, adverse movements in exchange rates can affect the entity's capacity to service its debt.

- This in turn impacts the credit risk borne by banks lending to such entities.

- RBI requires banks to factor in the risks arising from Unhedged Foreign Currency Exposures (UFCE) of their borrowers.

- Banks must put in place a proper mechanism to:

- Estimate UFCE of borrowers

- Assess the riskiness of such exposures

- Factor this in their credit appraisal, loan pricing, and provisioning

Computation of UFCE

Definition

- UFCE = Total FCY Exposure − FCY Hedged Exposure

- Only financial hedges (forward contracts, options, swaps) are considered, not natural hedges for this computation.

Natural Hedge

- A natural hedge exists when a borrower has FCY earnings that can offset FCY liabilities.

- Example: An exporter with dollar receivables and dollar loans — the receivables naturally offset the loan exposure.

- RBI's guidelines focus on financial hedges (derivatives) for UFCE computation, but banks may consider natural hedges in their internal credit assessment.

Steps in UFCE Estimation

- Identify all FCY liabilities (ECB, FCNR loans, buyer's credit, trade payables, etc.)

- Identify all FCY hedges (forward contracts, options, swaps)

- Compute UFCE = FCY Liabilities − FCY Hedges

- Express UFCE as a percentage of the entity's total equity or EBID (Earnings Before Interest & Depreciation)

UFCE Ratio

- UFCE as % of EBID is the key ratio used for provisioning and capital adequacy computation.

- Higher UFCE/EBID ratio → higher risk → higher provisioning and capital charge.

Provisioning and Capital Requirements for UFCE

Incremental Provisioning

Banks must maintain incremental provisioning for borrowers with UFCE:

| UFCE as % of EBID | Incremental Provisioning |

|---|---|

| Up to 15% | Nil |

| More than 15% and up to 30% | 20 bps (0.20%) |

| More than 30% and up to 50% | 40 bps (0.40%) |

| More than 50% and up to 75% | 60 bps (0.60%) |

| More than 75% | 80 bps (0.80%) |

Incremental Capital Requirement

Banks must hold incremental capital on exposure to borrowers with UFCE:

| UFCE as % of EBID | Incremental Capital (Risk Weight) |

|---|---|

| Up to 15% | Nil |

| More than 15% and up to 30% | 25% |

| More than 30% and up to 50% | 40% |

| More than 50% and up to 75% | 60% |

| More than 75% | 80% |

Key Points

- These are incremental provisions/capital — they are in addition to regular provisioning and risk weighting norms.

- Banks should review UFCE of borrowers at least on a quarterly basis.

- Information on UFCE should be obtained as part of regular credit appraisal and review.

Concepts of Forward Exposure

Forward Contract

- A forward contract is an agreement to buy or sell a specified quantity of foreign currency at a predetermined exchange rate on a specified future date.

- It is a binding obligation on both parties — the buyer and the seller.

- Used for hedging foreign currency risk arising from trade or capital account transactions.

Forward Rate

- The forward rate is determined by the spot rate adjusted for the interest rate differential between the two currencies.

- Forward Rate = Spot Rate × (1 + Interest Rate of Quote Currency) / (1 + Interest Rate of Base Currency)

- If the domestic interest rate is higher than the foreign interest rate, the forward rate will be at a premium (higher than spot).

- If the domestic interest rate is lower, it will be at a discount (lower than spot).

Forward Premium and Discount

- Forward Premium: When the forward rate is higher than the spot rate.

- Forward Discount: When the forward rate is lower than the spot rate.

- In India, since INR interest rates are typically higher than USD rates, USD is generally quoted at a forward premium against INR.

Types of Forward Contracts

- Fixed Date Forward: Delivery on a specific date.

- Option Forward: Delivery during a specified period (not a specific date) — the customer has the option to choose any date within the period.

- The option period should not exceed one month.

Cancellation and Extension

- Forward contracts can be cancelled or extended (rolled over) on or before the maturity date.

- Cancellation charges apply based on the difference between the contracted rate and the prevailing market rate.

- Automatic cancellation occurs if the contract is not utilized within 15 days after maturity.

Regulatory Guidelines — General Directions for Authorised Dealers (ADs)

Authorised Dealers

- Authorised Dealers (ADs) are entities licensed by RBI under FEMA, 1999 to deal in foreign exchange.

- Categories:

- AD Category-I: Banks (can undertake all current and capital account transactions)

- AD Category-II: Select financial institutions, authorized money changers

- AD Category-III: Select financial institutions for specific purposes

General Directions

- ADs must ensure that foreign exchange transactions are undertaken for bona fide purposes.

- They must comply with FEMA provisions and RBI directions.

- ADs should have a Board-approved policy for foreign exchange risk management.

- Know Your Customer (KYC) and Anti-Money Laundering (AML) norms must be followed.

- ADs must report transactions to RBI through prescribed returns and statements.

Specific Directions for ADs

Proprietary Trading

- ADs can undertake proprietary trading in foreign exchange for their own account.

- Must maintain open position limits as prescribed by RBI:

- Net Open Position (NOP) limits — daylight and overnight

- Aggregate Gap Limits (AGL)

- Proprietary positions must be within Board-approved limits.

Client Transactions

- ADs can offer foreign exchange products to clients for hedging genuine exposures.

- Must ensure suitability and appropriateness of products offered.

- Must provide fair pricing and transparent terms.

Risk Management

- ADs must have robust risk management systems including:

- Market risk management

- Credit risk management (counterparty risk)

- Operational risk management

- Regular stress testing and scenario analysis must be conducted.

- Mid-office (risk monitoring) must be independent of front office (dealing) and back office (settlement).

Directions for Exchanges

- Currency futures and currency options are permitted on recognized stock exchanges.

- Permitted currency pairs: USD-INR, EUR-INR, GBP-INR, JPY-INR, and cross-currency pairs (EUR-USD, GBP-USD, USD-JPY).

- Participants can take positions up to USD 100 million equivalent across all exchanges for USD-INR without underlying exposure documentation.

- For positions beyond the limit, participants must have underlying exposure.

- Exchanges must have robust risk management, margining, and settlement systems.

- Clearing Corporation acts as the Central Counterparty (CCP).

User Classification

Retail Users

- Entities that are not market-makers.

- Include individuals, corporates, firms, partnership firms, trusts, etc.

- They access FX derivatives to hedge their underlying exposure.

- Banks must ensure retail users understand the risks of derivative products.

Non-Retail Users

- Entities classified as non-retail include:

- AD Category-I banks

- Other entities with net worth of Rs. 500 crore or more

- Entities that have turnover of Rs. 1,000 crore or more

- Non-retail users are deemed to have the expertise to understand and manage risks of derivative products.

- They have access to a wider range of derivative products.

Suitability and Appropriateness

For Retail Users

- ADs must follow a Suitability and Appropriateness Policy when offering derivatives to retail users.

- Must assess whether the product is suitable for the user's needs and risk profile.

- Must explain the risks, costs, and payoffs of the product clearly.

- Provide a Product Suitability Statement to the user.

- Exotic products or complex structures cannot be offered to retail users unless they meet specific criteria.

For Non-Retail Users

- Deemed to have the expertise; suitability assessment is not mandatory.

- However, ADs must still ensure fair dealing and transparency.

- Non-retail users can access all permissible derivative products.

Permissible Foreign Exchange Derivative Contracts

OTC Derivatives (via ADs)

- Forward Contracts — most common hedging tool

- Foreign Currency Options — European/American style

- Foreign Currency Swaps — exchange of cash flows in different currencies

- Interest Rate Swaps (IRS) — in foreign currency

- Forward Rate Agreements (FRAs)

- Cross-Currency Swaps

- Cost Reduction Structures — combinations of options (for non-retail users)

- Seagull Structures — combination of call spread + selling a put (for non-retail users)

Exchange-Traded Derivatives

- Currency Futures — standardized contracts on exchanges

- Currency Options — standardized options on exchanges

- Available on: NSE, BSE, MCX-SX (MSEI)

Restrictions

- Leveraged products are not permitted for retail users.

- Derivatives must be for hedging purposes (retail users) — not speculation.

- Non-retail users can take positions based on their risk appetite.

Remittance Related to FX Derivative Contracts

- All premiums, margins, and settlement amounts related to FX derivative contracts can be remitted through ADs.

- No prior RBI approval is required for remittances under derivative contracts booked with ADs.

- For exchange-traded derivatives, margins and settlement are handled through the clearing mechanism.

- Net settlement in INR is permitted for certain derivative contracts.

- ADs must ensure that remittances are for genuine derivative transactions and not for circumventing FEMA provisions.

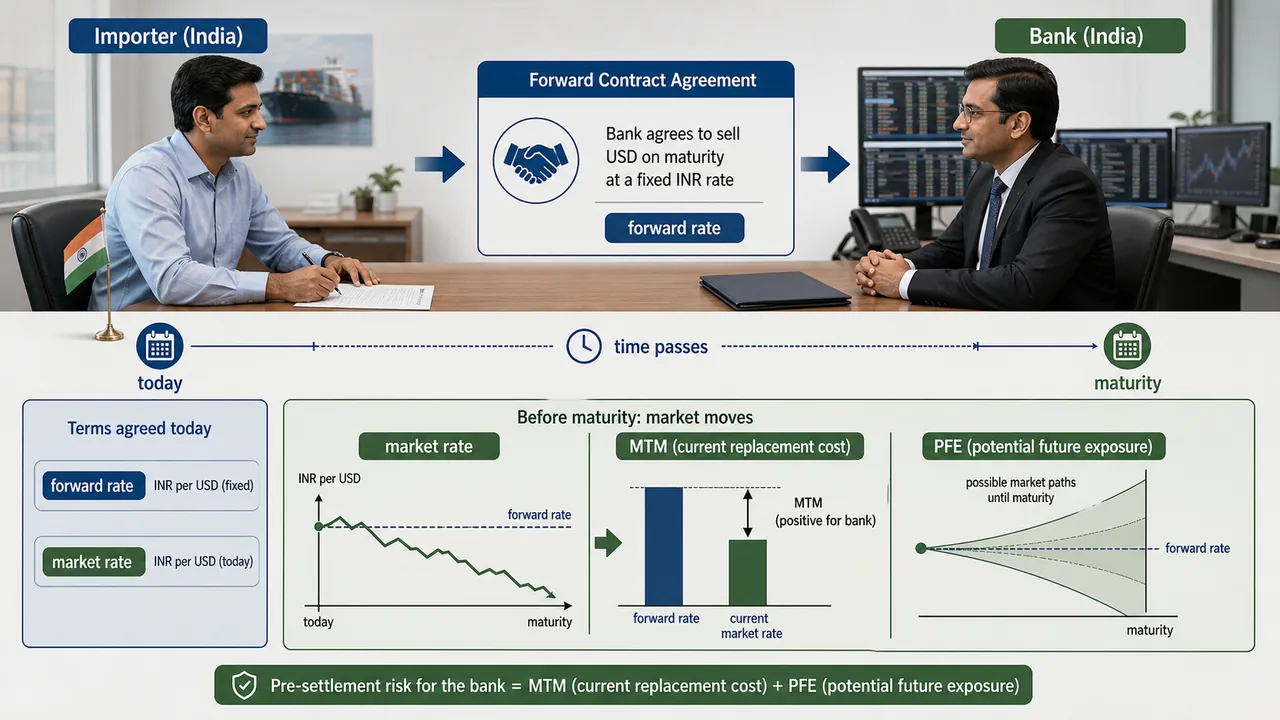

Pre-Settlement Risk

Definition

- Pre-Settlement Risk (PSR) is the risk that a counterparty will default before the final settlement of the transaction.

- Also known as counterparty credit risk in derivative transactions.

- Arises from the time a transaction is entered into until it is finally settled.

Components of PSR

-

Replacement Cost (Current Exposure):

- The mark-to-market (MTM) value of the contract.

- If the MTM is positive, the bank faces a loss if the counterparty defaults.

- If the MTM is negative, there is no current exposure (but potential future exposure exists).

-

Potential Future Exposure (PFE):

- The estimated increase in exposure over the remaining life of the contract.

- Accounts for potential future changes in market rates.

- Calculated using add-on factors based on the type and residual maturity of the contract.

Example

- Bank enters a forward contract to buy USD 1 million at ₹83.

- On the date of potential default, the market rate is ₹85.

- Replacement cost = (85 − 83) × 1,000,000 = ₹20,00,000

- If the counterparty defaults, the bank loses ₹20 lakh because it must now buy USD at ₹85 instead of ₹83.

- Additionally, PFE would be computed based on add-on factors.

Estimation of PSR

- PSR = Max(0, MTM) + PFE

- MTM is the current replacement cost (only positive values considered).

- PFE is computed using add-on percentages prescribed by RBI/Basel norms:

| Residual Maturity | Interest Rate | FX & Gold | Equity | Precious Metals | Other Commodities |

|---|---|---|---|---|---|

| Up to 1 year | 0.0% | 1.0% | 6.0% | 7.0% | 10.0% |

| 1–5 years | 0.5% | 5.0% | 8.0% | 7.0% | 12.0% |

| Over 5 years | 1.5% | 7.5% | 10.0% | 8.0% | 15.0% |

Countering Pre-Settlement Risk

- Credit Limits: Set counterparty-wise credit limits for derivative exposures.

- Netting Agreements: Legally enforceable netting reduces exposure (net positive vs gross exposure).

- Collateral (CSA): Credit Support Annex under ISDA — counterparties post collateral (margin) against MTM.

- Central Clearing (CCP): Exchange-traded derivatives cleared through CCP reduce bilateral PSR.

- Credit Value Adjustment (CVA): Pricing adjustment for counterparty credit risk.

- Close-out Netting: On default, all transactions with the counterparty are netted and closed.

- Regular MTM Monitoring: Daily mark-to-market and margin calls.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| UFCE | Total FCY Exposure − Hedged Exposure |

| UFCE Ratio | UFCE as % of EBID |

| UFCE ≤ 15% | Nil incremental provisioning & capital |

| UFCE 15–30% | 20 bps provisioning, 25% add'l risk weight |

| UFCE 30–50% | 40 bps provisioning, 40% add'l risk weight |

| UFCE 50–75% | 60 bps provisioning, 60% add'l risk weight |

| UFCE > 75% | 80 bps provisioning, 80% add'l risk weight |

| UFCE Review | At least quarterly |

| Forward Contract | Agreement to buy/sell FCY at predetermined rate on future date |

| Forward Rate | Spot Rate × (1 + Quote CCY rate) / (1 + Base CCY rate) |

| Forward Premium | Forward rate > Spot rate (higher domestic interest) |

| Forward Discount | Forward rate < Spot rate (lower domestic interest) |

| Option Forward | Delivery within a period (max 1 month) |

| Auto Cancellation | If not utilized within 15 days after maturity |

| AD Category-I | Banks — all current & capital account transactions |

| AD Category-II | Select FIs, authorized money changers |

| AD Category-III | Select FIs for specific purposes |

| Open Position Limits | NOP (daylight & overnight) + AGL |

| Exchange Pairs | USD-INR, EUR-INR, GBP-INR, JPY-INR + cross pairs |

| No-Doc Limit | Up to USD 100 million equivalent on exchanges |

| Non-Retail Threshold | Net worth ≥ Rs. 500 crore or turnover ≥ Rs. 1,000 crore |

| Retail Users | Must have underlying exposure; suitability assessment mandatory |

| Non-Retail Users | Wider product access; suitability not mandatory |

| OTC Derivatives | Forwards, Options, Swaps, IRS, FRA, Cross-Currency Swaps |

| Exchange Derivatives | Currency Futures & Options on NSE, BSE, MSEI |

| PSR | Pre-Settlement Risk = Max(0, MTM) + PFE |

| Replacement Cost | Positive MTM of contract |

| PFE (FX ≤ 1yr) | 1.0% of notional |

| PFE (FX 1–5yr) | 5.0% of notional |

| PFE (FX > 5yr) | 7.5% of notional |

| Countering PSR | Credit limits, Netting, Collateral (CSA), CCP, CVA, Close-out |

| Netting | ISDA close-out netting reduces bilateral exposure |

| CSA | Credit Support Annex — collateral against MTM |

| CVA | Credit Value Adjustment for counterparty risk pricing |

| Mid-Office | Must be independent of front office & back office |

Lesson Doubts

Ask questions, get expert answers