🚢 Export Finance

Pre-shipment and post-shipment export credit, Rupee EPC, PCFC, ECGC, post-shipment modes, interest rates, ECNOS, Interest Equalisation Scheme, Gold Card for exporters, EBR, consignment exports, sanction of export credit proposals.

Export Finance

Introduction

- India's export growth is essential for economic development and maintaining a healthy trade balance.

- The availability of timely and adequate credit at internationally competitive rates is crucial for promoting exports.

- Export finance ensures exporters can meet their working capital needs at every stage — from procurement of raw materials to realization of export proceeds.

- Term finance is for setting up new export-oriented units or expanding capacity; export finance specifically covers the production-to-realization cycle.

Two Stages of Export Finance

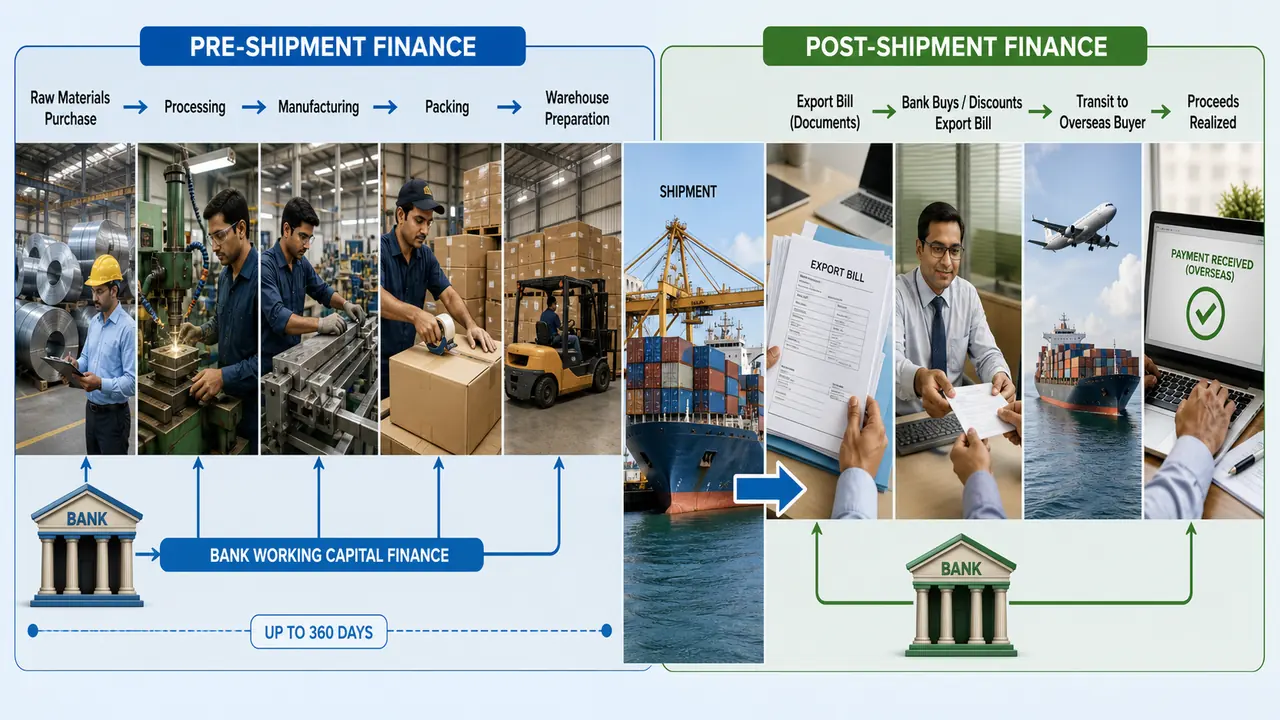

Export finance is broadly divided into two stages:

| Stage | Description |

|---|---|

| Pre-shipment Finance | Credit provided to an exporter before shipment of goods for purchasing, processing, manufacturing, and packing |

| Post-shipment Finance | Credit provided after shipment of goods until export proceeds are received |

Pre-shipment Finance

Forms of Pre-shipment Finance

- Rupee Export Packing Credit (EPC)

- Packing Credit in Foreign Currency (PCFC)

- ECGC advances

- Duty Drawback advances

- Advance against export receipts

Rupee Export Packing Credit (EPC)

- Working capital finance for purchasing, processing, manufacturing, and packing of goods meant for export.

- Must be settled within 360 days from the date of advance.

Eligibility Conditions

- Exporter must hold a valid IEC (Importer-Exporter Code) — a 10-digit code with lifetime validity, issued by DGFT.

- Must possess necessary export licenses.

- Must have confirmed orders or Letters of Credit (LCs).

- Bank must perform due diligence on the exporter.

Loan Disbursement

- Loan amount is the lower of FOB value or domestic production cost.

- Can be disbursed as a lump sum or in stages depending on manufacturing requirements.

RBI Liquidity Provisions

- RBI has stopped direct refinance to banks for export credit.

- RBI provides liquidity through special term repo operations.

- Dr. Urjit R. Patel Committee recommended that RBI stop direct refinance for export credit.

Liquidation of Packing Credit

- Normally by conversion to post-shipment credit on submission of export documents.

- Can also be through EEFC (Exchange Earners' Foreign Currency) Account or Diamond Dollar Account.

- Banks have flexibility on interest rate policies and repayment terms.

Packing Credit in Excess of Export Value

- For agro products, surplus over exportable quantity may be allowed.

- If goods become non-exportable, domestic sale proceeds can be used to liquidate.

- Financing of processed agricultural products is permitted.

Exporter Clients with Good Track Record

- Banks may provide repayment flexibility for established exporters.

- Contract substitution is allowed — one export order can replace another.

- Packing credit can be given from export savings of the exporter.

Running Account Facility

- Pre-shipment credit can be given without requiring immediate proof of LC for exporters with a solid track record.

- Must be settled within 360 days.

- Exporters must provide LCs or firm orders within a set timeframe.

- Utilization is monitored for production of firm orders or LCs.

- Funds must not be diverted for domestic use.

- Follows a First-In-First-Out (FIFO) system for marking off.

- Running account facility should not be extended to sub-suppliers.

Monitoring and Compliance

- FIFO approach for liquidation.

- Preferential export credit for a maximum of 360 days.

- Banks closely watch end-use of funds and subsequent production of firm orders.

- Penalties apply for non-export use of funds; facility may be revoked if misused.

Rupee Pre-shipment Credit to Specific Sectors

- Available to STC, MMTC, export houses, and similar entities.

- Credit can be extended for sub-suppliers through the Export Order Holder (EOH).

- The EOH bears responsibility and compliance obligations.

- ECGC guarantee may be required.

Packing Credit in Foreign Currency (PCFC)

Interest Collection

- Monthly interest collection against foreign currency sales, EEFC balances, or export bill discounting.

Credit Duration

- PCFC terms assessed individually, max 360 days.

- Interest rates for extensions within 180 days are bank-determined.

- PCFC adjusted at T.T. selling rate if no export occurs within 360 days.

Utilization and Disbursement

- For domestic inputs, appropriate spot rates applied.

- Banks may set minimum transaction lots based on resource availability.

Liquidation of PCFC

- Through export document proceeds, foreign currency loans, EEFC account balances, or exporter's rupee resources post-export.

PCFC Exceeding F.O.B. Value

- Limited to exportable portion for specific agro products.

Order or Commodity Substitution

- PCFC repayment possible with documents from different orders/commodities.

- Banks must verify the need for substitution and ensure it's commercially necessary.

Handling Cancellation or Non-Execution of Export Orders

- Exporters can repay PCFC by buying foreign exchange if the export order is canceled or unfulfilled.

- Interest payable on the rupee equivalent at ECNOS pre-shipment rate plus a penalty.

- Banks can send repayment to an overseas bank if PCFC was from that bank's credit line.

- Banks may re-issue PCFC after confirming the genuineness of previous cancellations.

Running Account Facility in PCFC

- Available to exporters with a solid track record.

- The need for such a facility must be justified by the exporter.

Monitoring and Penal Measures

- Banks closely watch end-use of funds and subsequent production of firm orders.

- Penalties apply for non-export use; facility may be revoked.

Managing Foreign Exchange and Borrowings

- Banks must manage prepayments within their foreign exchange position and Aggregate Gap Limit.

- Banks may charge for funding costs arising from mismatches in prepayments beyond one month.

Borrowing and Lending for PCFC

- Banks can secure foreign loans or negotiate credit lines without RBI's prior approval.

- Intra-bank lending rates in India may be used if overseas borrowing is not possible.

- Interest rate spread is at the discretion of the involved banks.

Forward Contracts for Exporters

- Exporters can book forward contracts based on confirmed orders before PCFC is availed.

- Forward contracts can be canceled when PCFC is used, especially for imported inputs.

- Customers can choose any actively traded permitted currency for coverage.

- Banks must comply with Foreign Exchange Management norms.

Sharing PCFC

- PCFC can be shared between the export order holder and the actual manufacturer.

- Transfers can occur within EOU/EPZ/SEZ units, from supplier to receiver or via manufacturer disclaimer.

- Financing is subject to the production cycle of goods and agreement between banks or bank consortiums.

Deemed Exports and PCFC

- PCFC is applicable to 'deemed exports' for supplies funded by international agencies.

- Such PCFC should be cleared by foreign currency loans at post-supply stage within 30 days or by the payment deadline from the project authorities.

- Repayment can also be through EEFC account balances or exporter's rupee resources.

Diamond Dollar Account Scheme

- Entities with a strong record in diamond trade and specific annual turnover are eligible for the DDA Scheme.

- Under DDA, PCFC can be cleared using dollar proceeds from diamond sales to other DDA holders.

- Detailed guidelines in RBI's AP (DIR Series) Circular No.13 dated October 29, 2009.

Post-shipment Rupee Export Finance

Types of Post-shipment Credit

- Credit extended after shipping goods/providing services until export proceeds are received.

- Standard period for export proceeds collection is up to 12 months after shipment.

Modes of Post-shipment Financing

- Purchasing or discounting export bills

- Negotiating export bills

- Providing advances against bills sent for collection

- Offering advances against exports shipped on consignment

- Issuing advances against un-drawn balances on exports

- Financing against expected duty drawback claims

Common Financing Practices

- The most frequent methods are bill purchase/discounting and bill negotiation.

Repayment of Post-shipment Credit

- Cleared with the export bills proceeds from overseas.

- Can also be repaid with funds from EEFC Account.

- Proceeds from other export bills that are not financed can also be used for repayment.

Period of Credit

| Nature of Bill | Period of Advance |

|---|---|

| Demand Bills | Normal Transit Period (NTP) as specified by FEDAI |

| Usance Bills | Max 365 days from date of shipment (incl. of NTP) |

| Overdue Bill — Demand Bill | Not Paid within NTP plus grace period |

| Usance Bill | Not Paid on due date |

- Normal Transit Period (NTP) means the average period normally involved from the date of negotiation/purchase/discount till the receipt of bill proceeds in the Nostro account of the bank concerned, as prescribed by FEDAI.

Advances Against Undrawn Balances

- Banks may offer advances on the undrawn balance of export bills, considering the quality/quantity assurance by the buyer.

- Based on the exporter's reliability and the buyer's payment history.

Advances Against Retention Money

- For turnkey projects or construction contracts, retention money is the percentage held back from progressive payments.

- Retention money is paid post-completion of the contract, pending approval by relevant authorities.

Guidelines for Retention Money Advances

- No advances against service-related retention money.

- Exporters encouraged to opt for guarantees over retention money.

- Advances for supplies-related retention may be considered based on amount, effect on exporter's liquidity, and past receipt records.

- Secure retention payments via Letter of Credit (LC) or Bank Guarantee where feasible.

Interest Rates on Retention Money Advances

- If retention is payable within one year of shipment, interest rates follow the 'ECNOS' category after 90 days.

- Retention payable after one year from shipment allows the bank to set the interest rate, considering it as deferred payment credit extending beyond one year.

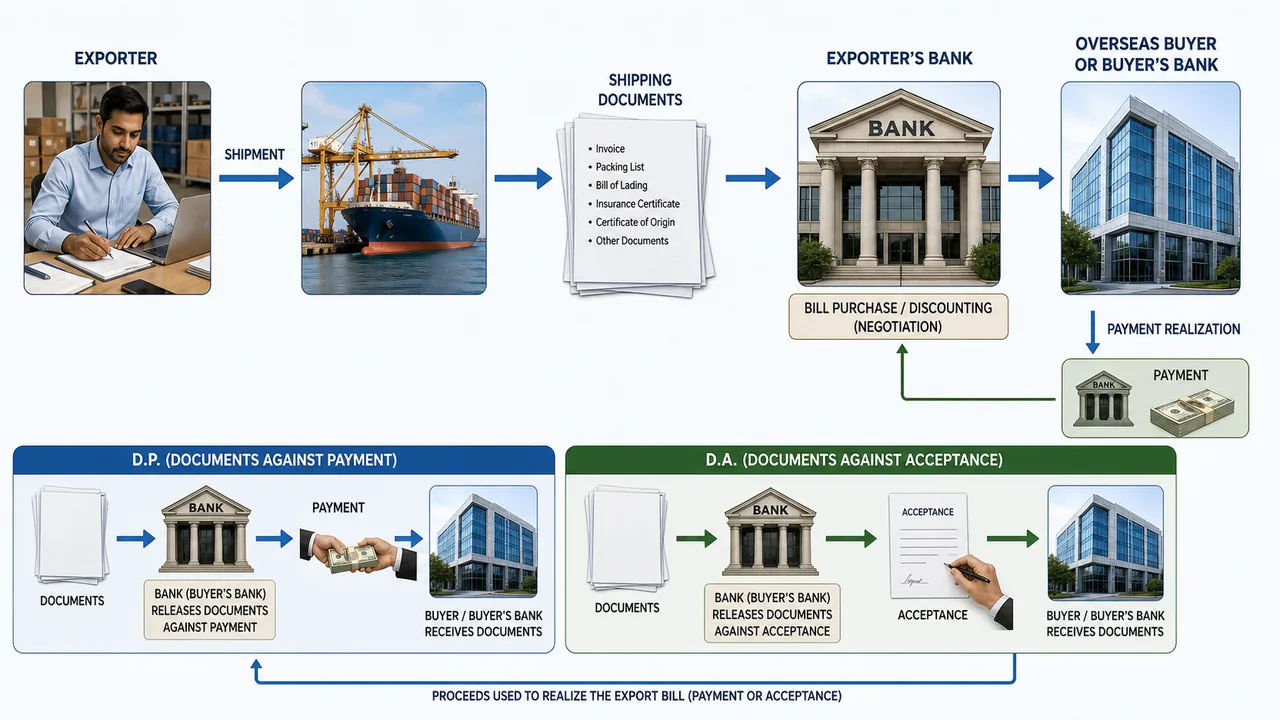

Handling of Export Bills for Payment/Acceptance

- Banks may provide financial support by purchasing or discounting export bills based on contractual terms.

- Credit limits for bill purchase/discounting are decided based on the exporter's needs.

Risk Management in Bill Transactions

- Purchase/discount of non-L/C covered bills carries payment risks, warranting ECGC (Export Credit Guarantee Corporation) insurance.

- Banks usually secure a WTPSG (Whole Turnover Post Shipment Guarantee), while exporters can opt for a buyer-specific policy.

Documentation and Control

- Documents against payment (D.P.) allow bank control over goods until payment.

- Documents against acceptance (D.A.) mean control is relinquished upon document release.

- House bills should only be purchased/discounted with specific high-level approval.

Exchange Rate Application

- The rupee value of a bill is based on the current bill buying rate or forward contract rate, depending on the bill's tenor.

Transit Period Consideration

- The NTP, as per FEDAI rules, is typically 25 days from document purchase to payment.

Negotiation of Bills Under L/C

- Bills drawn under irrevocable L/Cs can be negotiated easily if they adhere to L/C terms.

- Thorough scrutiny is essential to ensure presented documents fully comply with the L/C, avoiding any grounds for payment refusal by the issuing bank.

Common Discrepancies in Documents

- Late negotiation of documents: submission after expiry of L/C

- Late shipment: Date of B/L is later than the date given in L/C

- Late presentation: Documents not submitted within the limitation period in L/C or within 21 days from the date of shipment

- Drawings in excess of L/C amount

- Shipment made from/to the port other than that mentioned in L/C

- Partial shipment/Transshipment made in contravention of L/C

- Bill of Lading/AWB has not been properly signed

- Bill of Lading not presented in complete set

- Variation in the weight in invoice, weight list and other documents

- Inadequate value of insurance policy/certificate

- Presentation of unsigned/undated insurance policy/certificate

- Incomplete or incorrect drawing of Draft/Bill of Exchange

- Insufficient number of copies of various documents required in the LC

- Non-submission of certain documents as called for in the LC

Export on Consignment Basis

- Consignment exports can be prone to delays in the return of sales proceeds.

- Banks treat consignment exports on equal footing with cash term sales for interest rate purposes on post-shipment credit.

Interest Charges on Consignment Exports

- Interest is charged at the prescribed rate until the notional due date, which is based on the expected payment period, up to a maximum of one year.

- If the Foreign Exchange Department allows for an extended period beyond 365 days for the return of proceeds, the interest rate applies only until the original due date.

Exports of Gems

- Exports of precious and semi-precious stones often occur on consignment and may not close the pre-shipment credit within 365 days.

- Banks may transfer the outstanding pre-shipment credit to a special post-shipment account when the export occurs.

Adjustment of Advances for Gem Exports

- The special post-shipment account should be settled as soon as sales proceeds are received, but no later than 365 days after export, or as per the period extended by RBI's Foreign Exchange Department.

Financing Exports for Exhibitions and Sales

- Banks may extend financing to exporters for goods sent abroad for exhibitions and sales.

- Upon sale completion, exporters can benefit from reduced interest rates for both pre and post-shipment stages, provided as a rebate.

Separate Account Management

- Such advances are to be managed in distinct accounts.

Advances Against Duty Drawback Entitlements

- Post-shipment advances can be granted based on duty drawback entitlements, subject to ECGC guarantee.

- These are provisional advances pending final approval from Customs.

- Advances are contingent upon the export promotion copy of the shipping bill, which must include the EGM Number from Customs.

- Banks should arrange liens with designated banks to ensure the transfer of duty drawback funds.

Deferred Payment Terms for Specific Exports

- Post-shipment credit on deferred payment terms can be provided for exports of capital and producer goods, as delineated by the RBI.

ECGC Whole Turnover Post-Shipment Guarantee Scheme

- Banks can use ECGC's scheme to guard against the risk of non-payment by exporters after shipment.

- Banks are encouraged to adopt ECB for enhancing export promotion.

- Banks should ideally absorb the costs of the post-shipment guarantee premium, not the exporters.

- Exporters should obtain individual buyer insurance policies for additional risk mitigation.

- Coverage by ECGC can lead to lower capital charges for the bank due to reduced risk weight.

- Despite ECGC coverage, banks must continue to diligently pursue the collection of outstanding export payments.

Interest Rate on Rupee Export Credit

Base Rate System

- Implementation of Base Rate System: Initiated on July 1, 2010 for rupee export credit.

- All new rupee export credits are to be priced at or above the Base Rate.

Previous BPLR System Rates

- Until June 30, 2010, rates were capped at BPLR minus 2.5% annually for certain export credits.

Current Rate Setting

- Banks set interest rates based on 1-year MCLR, subtracting the Interest Equalisation rate and then potentially adding a bank-determined spread.

Risk-Based Pricing

- Interest rates may be adjusted based on the borrower's creditworthiness or risk profile.

Categories of Export Credit

Pre-shipment Credit (from the date of advance)

- Up to 270 days

- Against incentives receivable from Government covered by ECGC Guarantee up to 90 days

Post-shipment Credit (from the date of advance)

- On demand bills for transit period (as specified by FEDAI)

- Usance bills for total period comprising usance period of export bills, transit period as specified by FEDAI, and grace period, wherever applicable — up to 180 days

- Up to 365 days for exporters under the Gold Card Scheme

- Against incentives receivable from Govt. (covered by ECGC Guarantee) up to 90 days

- Against undrawn balances (up to 90 days)

- Against retention money (for supplies portion only) payable within one year from date of shipment (up to 90 days)

ECNOS (Export Credit Not Otherwise Specified)

- If pre-shipment advances aren't repaid from export proceeds within 360 days, they lose their special interest rate.

- They're then called Export Credit Not Otherwise Specified (ECNOS).

- Banks may charge a different interest rate for ECNOS pre-shipment credits.

- If exports don't happen at all, banks charge a domestic lending rate plus a penalty interest rate.

- The penalty rate is decided by each bank, based on transparent policies approved by their board.

- Banks have the autonomy to determine interest rates for ECNOS, within BPLR and spread rules.

- No additional penalty interest is applied to ECNOS categories.

Interest on Post-Shipment Credit — For Early Payment

| Nature of Bills | Payment | Applicable Rate |

|---|---|---|

| Demand Bill | Before expiry of NTP | Prescribed rate from date of advance to realization (credit to Nostro Account) |

| Usance Bill | Before Due Date | Prescribed rate up to the notional/actual due date or credit to the bank's Nostro account abroad, whichever is earlier |

| Demand bills/Usance bills | Interest for NTP/Notional or actual due date already recovered | Excess interest collected, if any, should be refunded |

| Overdue bills (Demand bills/Usance bills) | After NTP in case of expiry of bills/Upon expiry of due date in case of usance bill | Prescribed rate up to NTP (Demand Bills)/Due date (Usance Bills) and overdue period BPLR minus 2.5% up to 180 days till further notice |

Interest on Post-shipment Credit Adjusted from Rupee Resources

- In case ECGC has settled the claim due to non-expatriation of foreign exchange by the Govt./Banking Authorities of the importer countries as a result of balance of payment problems even though the payments have been made locally by the importers, interest rate as applicable for ECNOS post-shipment to be charged on full amount of advance.

- If export proceeds are later received, exporters get a refund for the difference in interest charged.

Interest Equalisation Scheme Overview

- Initiated by the Indian government to support select export categories and SMEs.

- Offers a 2% annual interest subvention, initially from April 2007 to September 2008.

- Expanded to include more products and additional 2% subvention for certain goods, imposing a minimum interest rate of 7%.

Scheme Extensions and Conditions

- Second scheme covered employment-focused sectors from December 2008 to September 2009, extended to March 2010.

- Third scheme from April 2010 to March 2011 with specific interest rate conditions.

- Additional sectors added over time, including leather, engineering, and textiles.

Interest Rate Adjustment

- With Base Rate System from July 2010, banks adjusted rates for eligible sectors by the subvention amount, maintaining a 7% floor rate.

- Interest rate reductions due to subvention are not considered a Base Rate violation.

Obligations and Reimbursements

- Banks must pass the full subvention benefit to exporters and claim reimbursement from RBI.

- Reimbursement claims are to be certified by external auditors and submitted quarterly.

Interest Equalisation Scheme on Pre and Post-Shipment Rupee Export Credit

Background

- Scheme initiated in April 2015.

- Initially valid for 5 years, extended due to COVID.

- Currently capped at Rs 10 Cr per annum per IEC.

- Banks that lend to exporters at an average rate of more than Repo + 4% would be debarred under the Scheme.

- Aimed at supporting exporters from identified sectors and MSMEs.

- Approved by the Union Cabinet until June 30, 2024.

Implementation Strategy

- Implemented by RBI through Public and Non-Public Sector Banks.

- Jointly monitored by DGFT and RBI.

Latest RBI Circular (February 22, 2024)

- RBI extends the Interest Equalization Scheme (IES) on Pre and Post Shipment Rupee Export Credit until June 30, 2024.

- Offers 2% interest equalization for manufacturers and merchant exporters in specified 410 HS lines and 3% for MSME manufacturers across any HS line.

- Restrictions on banks charging over Repo Rate + 4% before subvention.

- Cap on the annual net subvention amount at Rs 10 Cr per IEC.

Category-wise Rates

| Category of Exporters | Rate of Interest Equalisation |

|---|---|

| Manufacturer and Merchant Exporters exporting products listed in the 410 tariff lines | 2% |

| MSME exporters of all tariff lines | 3% |

Exclusions

- Telecom Instruments sector, except for MSME manufacturer exporters, is excluded from the Scheme.

- Beneficiaries availing benefits under any Production Linked Incentive (PLI) scheme are not eligible for the extended Scheme.

Post-Shipment Export Finance in Foreign Currency

- Banks can use their own foreign currency holdings, such as EEFC, RFC, and FCNR(B) accounts, to discount export usance bills.

- Rediscounting export bills overseas is possible at international rates.

- A collective bills portfolio facility is often more accessible than individual bill rediscounting abroad.

- Banks can set up a Bankers Acceptance Facility (BAF) for rediscounting bills, which requires no margin and is secured by collateral.

- Each bank can determine its BAF limit with foreign banks or rediscounting agencies, including factoring agencies, provided it's a 'without recourse' arrangement.

- Exporters can establish their own credit lines with foreign entities for direct bill discounting.

- Limits set by overseas entities under BAF are excluded from RBI's (FED) borrowing limit calculations for banks.

Eligibility Criteria (Rediscounting of Export Bills Abroad — EBR)

- Applicable mainly to export bills with a usance period of up to 180 days, including the shipping time and any grace period.

- Demand bills can be included if the foreign institution agrees.

- If the exporter is allowed to draw usance bills for more than 180 days per current FED rules, they may receive post-shipment credit under EBR for an extended period.

- Rediscounting can be conducted in any convertible currency.

- The EBR facility is also available for exports to Asian Clearing Union (ACU) member countries.

- Banks may centralize the BAF Scheme at a specific branch for ease of operation; other branches can also offer this service.

Source of On-shore Funds

- Demand bills should be processed using current post-shipment credit options or via foreign currency loans to exporters from banks' foreign currency balances.

- Banks may keep bills in their portfolio instead of rediscounting, but should access local markets if needed, to conserve foreign exchange.

- Inter-bank rediscounting is possible, allowing banks with unused BAF limits to assist others.

- Banks can obtain credit lines from domestic banks if unable to secure foreign loans or lacking overseas branches, ensuring the cost to exporters doesn't exceed 350 basis points over LIBOR/EURO LIBOR/EURIBOR.

- Banks can set their foreign currency export credit rates from May 5, 2012.

- Banks are allowed to use foreign loans and funds from buy-sell swaps in domestic forex for EBR facilities under specific conditions.

ECGC Cover

- 'With recourse' export bill rediscounting keeps existing ECGC coverage as exporter liability remains until bill settlement.

- 'Without recourse' rediscounting ends ECGC liability when bills are rediscounted.

- Banks cannot use export bills discounted under this scheme for RBI refinance.

- These discounted export bills should be reported separately from other export credit for refinance purposes.

- Foreign currency export credit interest rates depend on loan duration and comply with RBI guidelines.

Customer Service & Simplification of Procedure

- RBI is enhancing exporter competitiveness and efficiency by minimizing bank-related procedural delays.

Key Initiatives

- Encouraging banks to ensure timely and sufficient credit to exporters.

- Banks should offer essential services and advice on export procedures and opportunities.

- Creation of Export Counsel Offices in banks to support and guide exporters, especially the small-scale and non-traditional ones.

Gold Card Scheme for Exporters

- Available for all qualifying exporters, including small and medium enterprises.

- Excludes exporters flagged by ECGC or with over 10% overdue bills from the past year's turnover.

- Cardholders receive preferential credit terms, such as lower interest rates.

- Streamlined and expedited processing of credit applications for cardholders.

- Banks to outline specific benefits for Gold Card users, including lower service charges.

- Simplified procedures for sanctioning and renewing credit limits, with in-principle approval for three years and easy renewal conditions.

- Provision of a standby credit limit, at least 20% above the assessed limit, for sudden orders or seasonal fluctuations.

- Flexible inventory norms for unexpected large orders.

- Quick processing of requests: 25 days for new applications, 15 for renewals, and 7 days for ad-hoc requests.

- Priority given to Gold Card holders for foreign currency packing credit.

- Potential for collateral waivers and exemptions from ECGC guarantees based on the cardholder's credibility.

- Additional banking services like ATM, internet banking, and international debit/credit cards may be offered.

- Interest rates for Gold Card holders capped at general export credit rates and within RBI guidelines, with potential for further reduction based on performance.

- Extended interest rate benefits on post-shipment credit up to 365 days.

- Eligibility for foreign currency credit cards based on export proceeds realization history.

- Priority access to PCFC funds over non-export borrowers.

- Option for term loans in foreign currency from certain designated funds, excluding overseas borrowings.

Sanction of Export Credit Proposals

- Banks aim to approve new or increased export credit limits within 45 days and renew existing ones within 30 days. Ad hoc facilities should be processed within 15 days, except for Gold Card holders who have shorter timeframes.

- Ad hoc credit facilities should not incur additional interest charges.

- Export credit applications should be streamlined, with reduced data requirements for exporters.

- Banks can use different assessment methods (Projected Balance Sheet, Turnover, or Cash Budget) to determine exporters' working capital needs.

- Lines of Credit are normally set for one year but can extend up to three years and are subject to annual review. In case of renewal delays, current limits remain valid, and urgent credit needs should be met promptly.

- Requirement for submission of export orders or L/Cs for each disbursement can be waived for exporters with good track records; periodic statements are sufficient.

- Banks are tasked with ensuring that export credit needs are fully and promptly met at competitive rates and addressing any inefficiencies in credit delivery to the export sector.

- Export bills should be realized within 12 months; extensions are possible for genuine cases. Unsettled bills can be converted to rupee loans/terms, with ECGC claims lodged for defaults as necessary.

Other Points

- Before offering export finance, banks must refer to the Foreign Trade Policy and check the ECGC coverage and country risk profiles.

- Banks should adhere to their own guidelines regarding export credit, margin, and security requirements.

- A bank must assess the exporter's real financial needs and obtain all necessary documents at once for efficiency.

- Conduct pre-sanction inspections, perform due diligence, and strictly enforce KYC protocols.

- Banks are advised to be flexible regarding financial ratios and security standards but must ensure the proposal's viability and the borrower's integrity.

- Exporters need to demonstrate their ability to fulfill orders within set timelines.

- The bank should evaluate the exporter's experience in the trade.

- The amount of finance provided should align with the anticipated export turnover and input costs.

- Verify the standing of the L/C issuing bank and the terms of the L/C itself.

- For orders not covered by an L/C, banks should acquire a satisfactory status report on the foreign buyer, consulting ECGC or head office when necessary.

- Pre-shipment and post-shipment financing should be addressed concurrently.

- Pre-shipment finance can be accessed at any branch, but post-shipment finance is limited to designated branches ('A' or 'B' category).

- Employ various methods to assess export credit limits: Projected Turnover Method for smaller limits, MPBF Method, or Cash Budget Method.

- In a consortium setting, once MPBF is agreed upon, member banks should sanction limits promptly based on their share.

- Annually review export credit limits without disrupting ongoing finance arrangements.

- Meet urgent or additional financial needs on an ad hoc basis if there are delays in sanctioning regular limits.

Quick Notes for Exam

- Pre-shipment finance assists exporters with packing of goods, procuring raw materials, and transporting goods to the port — but NOT marketing expenses.

- The PCFC is considered up to the date of shipment.

- PCFC is intended to help exporters with procurement of raw materials and goods for export.

- The Whole-Turnover Packing Credit (ECIB-WTPC) guarantee fee is to be borne by the exporters.

- The WTPC guarantee helps exporters by covering all packing credit accounts.

- The primary reason for providing pre-shipment credit in foreign currency is to avoid currency exchange risk.

- Interest rate on rupee export credit advances should be at or above Base Rate.

- Exporters can avail a whole turnover guarantee under the WTPC scheme.

- ECGC offers coverage to both exporters and banks.

- The purpose of pre-sanction inspection in export finance is to ensure due diligence and compliance.

- The primary source of information on the buyer's country risk profile is Head Office or ECGC.

- In export finance, KYC compliance must be strict.

- The prime status of the L/C issuing bank determines the credibility and reliability of the payment.

- When an export order is not backed by an L/C, banks should obtain a satisfactory status report on the foreign buyer.

- Banks should ensure exporters' credit requirements are met in full and promptly at competitive rates.

- Upon delay in renewal, banks should allow existing sanctioned limits to continue uninterrupted.

- In case of non-realisation of export bills by due date, banks should convert the outstanding to a rupee loan/term.

- Banks should consider dispensation of export credit to be expeditious and timely.

- In case of delay in renewal of limits, banks should provide urgent requirements on an ad hoc basis by extending an interim ad hoc limit.

- Flexibility in banking terms for exporters should not compromise the viability of the proposal.

- Under a consortium arrangement, banks are required to process proposals within a set time frame after MPBF approval.

- Pre-shipment and post-shipment limits should be considered simultaneously and in full.

- The Fixed Asset Method is NOT used for assessing export credit limits — only Projected Turnover, MPBF, or Cash Budget methods.

- Post-shipment finance includes all of the following EXCEPT pre-shipment export credit: Export Bills Purchased/Discounted, Advance against Bills sent for Collection, Advance against Export on Consignment Basis.

- The sanctioned export credit should be reviewed annually.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Two Stages | Pre-shipment (before shipment) and Post-shipment (after shipment) |

| Pre-shipment Forms | Rupee EPC, PCFC, ECGC advances, Duty Drawback, Advance against export receipts |

| EPC Purpose | Working capital for purchasing, processing, manufacturing, packing |

| EPC Max Duration | 360 days from date of advance |

| IEC Code | 10-digit, lifetime validity, issued by DGFT |

| Loan Amount | Lower of FOB value or domestic production cost |

| RBI Refinance | Stopped direct refinance; uses special term repo instead |

| Dr. Urjit Patel | Recommended RBI stop direct refinance for export credit |

| Liquidation of EPC | Conversion to post-shipment credit, EEFC/DDA proceeds |

| Running Account | Pre-shipment without immediate LC proof; FIFO system; max 360 days |

| Running Account — Not For | Sub-suppliers |

| STC/MMTC Credit | Via Export Order Holder; ECGC guarantee may be required |

| PCFC Max Duration | 360 days; adjusted at T.T. selling rate if no export |

| PCFC Liquidation | Export document proceeds, EEFC balances, foreign currency loans |

| PCFC Cancellation | Buy foreign exchange; pay ECNOS rate + penalty |

| PCFC Forward Contracts | Allowed on confirmed orders; can cancel when PCFC used |

| PCFC Sharing | Between export order holder and manufacturer; within EOU/EPZ/SEZ |

| Deemed Exports | PCFC applicable; cleared within 30 days at post-supply stage |

| DDA Scheme | Diamond trade entities; RBI Circular No.13, October 29, 2009 |

| Post-shipment Period | Up to 12 months after shipment for proceeds collection |

| Post-shipment Modes | Bill purchase/discount, negotiation, advances against collection/consignment/undrawn balances/duty drawback |

| NTP | Normal Transit Period; typically 25 days per FEDAI |

| Demand Bills | Advance for NTP as specified by FEDAI |

| Usance Bills | Max 365 days from shipment (incl. NTP) |

| Retention Money | For turnkey/construction; no advances on service-related retention |

| WTPSG | Whole Turnover Post Shipment Guarantee — bank secures this |

| D.P. vs D.A. | D.P. = bank control until payment; D.A. = control released on acceptance |

| Document Discrepancies | 14 common types (late negotiation, excess amount, port mismatch, etc.) |

| Consignment Exports | Equal footing with cash terms for interest; max 1 year expected payment |

| Gem Exports | May not close pre-shipment within 365 days; special post-shipment account |

| Duty Drawback Advances | Subject to ECGC guarantee; need EGM Number from Customs |

| ECGC WTPSG | Bank absorbs premium cost; leads to lower capital charges |

| Base Rate System | From July 1, 2010 for rupee export credit |

| Pre-BPLR Rate | Capped at BPLR minus 2.5% until June 30, 2010 |

| Current Rate | Based on 1-year MCLR minus Interest Equalisation + bank spread |

| Pre-shipment Credit Period | Up to 270 days |

| ECNOS | Export Credit Not Otherwise Specified; when not repaid within 360 days |

| ECNOS Penalty | Domestic lending rate + penalty; no additional penalty on ECNOS category |

| Interest Equalisation | 2% subvention initially (April 2007); 7% floor rate |

| IES (2015 Scheme) | Initiated April 2015; cap Rs 10 Cr/annum per IEC |

| IES Rate — 410 HS Lines | 2% for manufacturer & merchant exporters |

| IES Rate — MSME | 3% for MSME manufacturers across all tariff lines |

| IES Bank Cap | Banks charging over Repo + 4% are debarred |

| IES Exclusion | Telecom Instruments (except MSME); PLI scheme beneficiaries |

| IES Extended Until | June 30, 2024 (RBI circular Feb 22, 2024) |

| EBR Usance | Up to 180 days including shipping time and grace |

| EBR Currency | Any convertible currency; available for ACU member countries |

| BAF | Bankers Acceptance Facility; no margin; secured by collateral |

| EBR Cost Cap | Max 350 bps over LIBOR/EURO LIBOR/EURIBOR |

| FC Export Credit Rates | Banks can set own rates from May 5, 2012 |

| With Recourse | ECGC coverage continues until bill settlement |

| Without Recourse | ECGC liability ends on rediscounting |

| Gold Card Eligibility | All exporters incl. SMEs; excludes ECGC-flagged or >10% overdue |

| Gold Card — Standby Limit | At least 20% above assessed limit |

| Gold Card — Processing | New: 25 days; Renewal: 15 days; Ad hoc: 7 days |

| Gold Card — Post-shipment | Interest rate benefits up to 365 days |

| Gold Card — In-Principle | Approval for 3 years with easy renewal |

| Sanction — New Limits | Within 45 days |

| Sanction — Renewal | Within 30 days |

| Sanction — Ad Hoc | Within 15 days; no additional interest charges |

| Assessment Methods | Projected Balance Sheet, Turnover, Cash Budget |

| LOC Duration | Set for 1 year; extendable up to 3 years; annual review |

| Bill Realization | Within 12 months; unsettled → rupee loan conversion |

| Post-shipment Branch | Only 'A' or 'B' category designated branches |

| Pre-shipment Branch | Available at any branch |

| Export Counsel Office | For small-scale and non-traditional exporters |

🔐

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

Pro

Popular Save ₹100/mo

₹ 99 /mo

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Export Finance

Introduction

- India's export growth is essential for economic development and maintaining a healthy trade balance.

- The availability of timely and adequate credit at internationally competitive rates is crucial for promoting exports.

- Export finance ensures exporters can meet their working capital needs at every stage — from procurement of raw materials to realization of export proceeds.

- Term finance is for setting up new export-oriented units or expanding capacity; export finance specifically covers the production-to-realization cycle.

Two Stages of Export Finance

Export finance is broadly divided into two stages:

| Stage | Description |

|---|---|

| Pre-shipment Finance | Credit provided to an exporter before shipment of goods for purchasing, processing, manufacturing, and packing |

| Post-shipment Finance | Credit provided after shipment of goods until export proceeds are received |

Pre-shipment Finance

Forms of Pre-shipment Finance

- Rupee Export Packing Credit (EPC)

- Packing Credit in Foreign Currency (PCFC)

- ECGC advances

- Duty Drawback advances

- Advance against export receipts

Rupee Export Packing Credit (EPC)

- Working capital finance for purchasing, processing, manufacturing, and packing of goods meant for export.

- Must be settled within 360 days from the date of advance.

Eligibility Conditions

- Exporter must hold a valid IEC (Importer-Exporter Code) — a 10-digit code with lifetime validity, issued by DGFT.

- Must possess necessary export licenses.

- Must have confirmed orders or Letters of Credit (LCs).

- Bank must perform due diligence on the exporter.

Loan Disbursement

- Loan amount is the lower of FOB value or domestic production cost.

- Can be disbursed as a lump sum or in stages depending on manufacturing requirements.

RBI Liquidity Provisions

- RBI has stopped direct refinance to banks for export credit.

- RBI provides liquidity through special term repo operations.

- Dr. Urjit R. Patel Committee recommended that RBI stop direct refinance for export credit.

Liquidation of Packing Credit

- Normally by conversion to post-shipment credit on submission of export documents.

- Can also be through EEFC (Exchange Earners' Foreign Currency) Account or Diamond Dollar Account.

- Banks have flexibility on interest rate policies and repayment terms.

Packing Credit in Excess of Export Value

- For agro products, surplus over exportable quantity may be allowed.

- If goods become non-exportable, domestic sale proceeds can be used to liquidate.

- Financing of processed agricultural products is permitted.

Exporter Clients with Good Track Record

- Banks may provide repayment flexibility for established exporters.

- Contract substitution is allowed — one export order can replace another.

- Packing credit can be given from export savings of the exporter.

Running Account Facility

- Pre-shipment credit can be given without requiring immediate proof of LC for exporters with a solid track record.

- Must be settled within 360 days.

- Exporters must provide LCs or firm orders within a set timeframe.

- Utilization is monitored for production of firm orders or LCs.

- Funds must not be diverted for domestic use.

- Follows a First-In-First-Out (FIFO) system for marking off.

- Running account facility should not be extended to sub-suppliers.

Monitoring and Compliance

- FIFO approach for liquidation.

- Preferential export credit for a maximum of 360 days.

- Banks closely watch end-use of funds and subsequent production of firm orders.

- Penalties apply for non-export use of funds; facility may be revoked if misused.

Rupee Pre-shipment Credit to Specific Sectors

- Available to STC, MMTC, export houses, and similar entities.

- Credit can be extended for sub-suppliers through the Export Order Holder (EOH).

- The EOH bears responsibility and compliance obligations.

- ECGC guarantee may be required.

Packing Credit in Foreign Currency (PCFC)

Interest Collection

- Monthly interest collection against foreign currency sales, EEFC balances, or export bill discounting.

Credit Duration

- PCFC terms assessed individually, max 360 days.

- Interest rates for extensions within 180 days are bank-determined.

- PCFC adjusted at T.T. selling rate if no export occurs within 360 days.

Utilization and Disbursement

- For domestic inputs, appropriate spot rates applied.

- Banks may set minimum transaction lots based on resource availability.

Liquidation of PCFC

- Through export document proceeds, foreign currency loans, EEFC account balances, or exporter's rupee resources post-export.

PCFC Exceeding F.O.B. Value

- Limited to exportable portion for specific agro products.

Order or Commodity Substitution

- PCFC repayment possible with documents from different orders/commodities.

- Banks must verify the need for substitution and ensure it's commercially necessary.

Handling Cancellation or Non-Execution of Export Orders

- Exporters can repay PCFC by buying foreign exchange if the export order is canceled or unfulfilled.

- Interest payable on the rupee equivalent at ECNOS pre-shipment rate plus a penalty.

- Banks can send repayment to an overseas bank if PCFC was from that bank's credit line.

- Banks may re-issue PCFC after confirming the genuineness of previous cancellations.

Running Account Facility in PCFC

- Available to exporters with a solid track record.

- The need for such a facility must be justified by the exporter.

Monitoring and Penal Measures

- Banks closely watch end-use of funds and subsequent production of firm orders.

- Penalties apply for non-export use; facility may be revoked.

Managing Foreign Exchange and Borrowings

- Banks must manage prepayments within their foreign exchange position and Aggregate Gap Limit.

- Banks may charge for funding costs arising from mismatches in prepayments beyond one month.

Borrowing and Lending for PCFC

- Banks can secure foreign loans or negotiate credit lines without RBI's prior approval.

- Intra-bank lending rates in India may be used if overseas borrowing is not possible.

- Interest rate spread is at the discretion of the involved banks.

Forward Contracts for Exporters

- Exporters can book forward contracts based on confirmed orders before PCFC is availed.

- Forward contracts can be canceled when PCFC is used, especially for imported inputs.

- Customers can choose any actively traded permitted currency for coverage.

- Banks must comply with Foreign Exchange Management norms.

Sharing PCFC

- PCFC can be shared between the export order holder and the actual manufacturer.

- Transfers can occur within EOU/EPZ/SEZ units, from supplier to receiver or via manufacturer disclaimer.

- Financing is subject to the production cycle of goods and agreement between banks or bank consortiums.

Deemed Exports and PCFC

- PCFC is applicable to 'deemed exports' for supplies funded by international agencies.

- Such PCFC should be cleared by foreign currency loans at post-supply stage within 30 days or by the payment deadline from the project authorities.

- Repayment can also be through EEFC account balances or exporter's rupee resources.

Diamond Dollar Account Scheme

- Entities with a strong record in diamond trade and specific annual turnover are eligible for the DDA Scheme.

- Under DDA, PCFC can be cleared using dollar proceeds from diamond sales to other DDA holders.

- Detailed guidelines in RBI's AP (DIR Series) Circular No.13 dated October 29, 2009.

Post-shipment Rupee Export Finance

Types of Post-shipment Credit

- Credit extended after shipping goods/providing services until export proceeds are received.

- Standard period for export proceeds collection is up to 12 months after shipment.

Modes of Post-shipment Financing

- Purchasing or discounting export bills

- Negotiating export bills

- Providing advances against bills sent for collection

- Offering advances against exports shipped on consignment

- Issuing advances against un-drawn balances on exports

- Financing against expected duty drawback claims

Common Financing Practices

- The most frequent methods are bill purchase/discounting and bill negotiation.

Repayment of Post-shipment Credit

- Cleared with the export bills proceeds from overseas.

- Can also be repaid with funds from EEFC Account.

- Proceeds from other export bills that are not financed can also be used for repayment.

Period of Credit

| Nature of Bill | Period of Advance |

|---|---|

| Demand Bills | Normal Transit Period (NTP) as specified by FEDAI |

| Usance Bills | Max 365 days from date of shipment (incl. of NTP) |

| Overdue Bill — Demand Bill | Not Paid within NTP plus grace period |

| Usance Bill | Not Paid on due date |

- Normal Transit Period (NTP) means the average period normally involved from the date of negotiation/purchase/discount till the receipt of bill proceeds in the Nostro account of the bank concerned, as prescribed by FEDAI.

Advances Against Undrawn Balances

- Banks may offer advances on the undrawn balance of export bills, considering the quality/quantity assurance by the buyer.

- Based on the exporter's reliability and the buyer's payment history.

Advances Against Retention Money

- For turnkey projects or construction contracts, retention money is the percentage held back from progressive payments.

- Retention money is paid post-completion of the contract, pending approval by relevant authorities.

Guidelines for Retention Money Advances

- No advances against service-related retention money.

- Exporters encouraged to opt for guarantees over retention money.

- Advances for supplies-related retention may be considered based on amount, effect on exporter's liquidity, and past receipt records.

- Secure retention payments via Letter of Credit (LC) or Bank Guarantee where feasible.

Interest Rates on Retention Money Advances

- If retention is payable within one year of shipment, interest rates follow the 'ECNOS' category after 90 days.

- Retention payable after one year from shipment allows the bank to set the interest rate, considering it as deferred payment credit extending beyond one year.

Handling of Export Bills for Payment/Acceptance

- Banks may provide financial support by purchasing or discounting export bills based on contractual terms.

- Credit limits for bill purchase/discounting are decided based on the exporter's needs.

Risk Management in Bill Transactions

- Purchase/discount of non-L/C covered bills carries payment risks, warranting ECGC (Export Credit Guarantee Corporation) insurance.

- Banks usually secure a WTPSG (Whole Turnover Post Shipment Guarantee), while exporters can opt for a buyer-specific policy.

Documentation and Control

- Documents against payment (D.P.) allow bank control over goods until payment.

- Documents against acceptance (D.A.) mean control is relinquished upon document release.

- House bills should only be purchased/discounted with specific high-level approval.

Exchange Rate Application

- The rupee value of a bill is based on the current bill buying rate or forward contract rate, depending on the bill's tenor.

Transit Period Consideration

- The NTP, as per FEDAI rules, is typically 25 days from document purchase to payment.

Negotiation of Bills Under L/C

- Bills drawn under irrevocable L/Cs can be negotiated easily if they adhere to L/C terms.

- Thorough scrutiny is essential to ensure presented documents fully comply with the L/C, avoiding any grounds for payment refusal by the issuing bank.

Common Discrepancies in Documents

- Late negotiation of documents: submission after expiry of L/C

- Late shipment: Date of B/L is later than the date given in L/C

- Late presentation: Documents not submitted within the limitation period in L/C or within 21 days from the date of shipment

- Drawings in excess of L/C amount

- Shipment made from/to the port other than that mentioned in L/C

- Partial shipment/Transshipment made in contravention of L/C

- Bill of Lading/AWB has not been properly signed

- Bill of Lading not presented in complete set

- Variation in the weight in invoice, weight list and other documents

- Inadequate value of insurance policy/certificate

- Presentation of unsigned/undated insurance policy/certificate

- Incomplete or incorrect drawing of Draft/Bill of Exchange

- Insufficient number of copies of various documents required in the LC

- Non-submission of certain documents as called for in the LC

Export on Consignment Basis

- Consignment exports can be prone to delays in the return of sales proceeds.

- Banks treat consignment exports on equal footing with cash term sales for interest rate purposes on post-shipment credit.

Interest Charges on Consignment Exports

- Interest is charged at the prescribed rate until the notional due date, which is based on the expected payment period, up to a maximum of one year.

- If the Foreign Exchange Department allows for an extended period beyond 365 days for the return of proceeds, the interest rate applies only until the original due date.

Exports of Gems

- Exports of precious and semi-precious stones often occur on consignment and may not close the pre-shipment credit within 365 days.

- Banks may transfer the outstanding pre-shipment credit to a special post-shipment account when the export occurs.

Adjustment of Advances for Gem Exports

- The special post-shipment account should be settled as soon as sales proceeds are received, but no later than 365 days after export, or as per the period extended by RBI's Foreign Exchange Department.

Financing Exports for Exhibitions and Sales

- Banks may extend financing to exporters for goods sent abroad for exhibitions and sales.

- Upon sale completion, exporters can benefit from reduced interest rates for both pre and post-shipment stages, provided as a rebate.

Separate Account Management

- Such advances are to be managed in distinct accounts.

Advances Against Duty Drawback Entitlements

- Post-shipment advances can be granted based on duty drawback entitlements, subject to ECGC guarantee.

- These are provisional advances pending final approval from Customs.

- Advances are contingent upon the export promotion copy of the shipping bill, which must include the EGM Number from Customs.

- Banks should arrange liens with designated banks to ensure the transfer of duty drawback funds.

Deferred Payment Terms for Specific Exports

- Post-shipment credit on deferred payment terms can be provided for exports of capital and producer goods, as delineated by the RBI.

ECGC Whole Turnover Post-Shipment Guarantee Scheme

- Banks can use ECGC's scheme to guard against the risk of non-payment by exporters after shipment.

- Banks are encouraged to adopt ECB for enhancing export promotion.

- Banks should ideally absorb the costs of the post-shipment guarantee premium, not the exporters.

- Exporters should obtain individual buyer insurance policies for additional risk mitigation.

- Coverage by ECGC can lead to lower capital charges for the bank due to reduced risk weight.

- Despite ECGC coverage, banks must continue to diligently pursue the collection of outstanding export payments.

Interest Rate on Rupee Export Credit

Base Rate System

- Implementation of Base Rate System: Initiated on July 1, 2010 for rupee export credit.

- All new rupee export credits are to be priced at or above the Base Rate.

Previous BPLR System Rates

- Until June 30, 2010, rates were capped at BPLR minus 2.5% annually for certain export credits.

Current Rate Setting

- Banks set interest rates based on 1-year MCLR, subtracting the Interest Equalisation rate and then potentially adding a bank-determined spread.

Risk-Based Pricing

- Interest rates may be adjusted based on the borrower's creditworthiness or risk profile.

Categories of Export Credit

Pre-shipment Credit (from the date of advance)

- Up to 270 days

- Against incentives receivable from Government covered by ECGC Guarantee up to 90 days

Post-shipment Credit (from the date of advance)

- On demand bills for transit period (as specified by FEDAI)

- Usance bills for total period comprising usance period of export bills, transit period as specified by FEDAI, and grace period, wherever applicable — up to 180 days

- Up to 365 days for exporters under the Gold Card Scheme

- Against incentives receivable from Govt. (covered by ECGC Guarantee) up to 90 days

- Against undrawn balances (up to 90 days)

- Against retention money (for supplies portion only) payable within one year from date of shipment (up to 90 days)

ECNOS (Export Credit Not Otherwise Specified)

- If pre-shipment advances aren't repaid from export proceeds within 360 days, they lose their special interest rate.

- They're then called Export Credit Not Otherwise Specified (ECNOS).

- Banks may charge a different interest rate for ECNOS pre-shipment credits.

- If exports don't happen at all, banks charge a domestic lending rate plus a penalty interest rate.

- The penalty rate is decided by each bank, based on transparent policies approved by their board.

- Banks have the autonomy to determine interest rates for ECNOS, within BPLR and spread rules.

- No additional penalty interest is applied to ECNOS categories.

Interest on Post-Shipment Credit — For Early Payment

| Nature of Bills | Payment | Applicable Rate |

|---|---|---|

| Demand Bill | Before expiry of NTP | Prescribed rate from date of advance to realization (credit to Nostro Account) |

| Usance Bill | Before Due Date | Prescribed rate up to the notional/actual due date or credit to the bank's Nostro account abroad, whichever is earlier |

| Demand bills/Usance bills | Interest for NTP/Notional or actual due date already recovered | Excess interest collected, if any, should be refunded |

| Overdue bills (Demand bills/Usance bills) | After NTP in case of expiry of bills/Upon expiry of due date in case of usance bill | Prescribed rate up to NTP (Demand Bills)/Due date (Usance Bills) and overdue period BPLR minus 2.5% up to 180 days till further notice |

Interest on Post-shipment Credit Adjusted from Rupee Resources

- In case ECGC has settled the claim due to non-expatriation of foreign exchange by the Govt./Banking Authorities of the importer countries as a result of balance of payment problems even though the payments have been made locally by the importers, interest rate as applicable for ECNOS post-shipment to be charged on full amount of advance.

- If export proceeds are later received, exporters get a refund for the difference in interest charged.

Interest Equalisation Scheme Overview

- Initiated by the Indian government to support select export categories and SMEs.

- Offers a 2% annual interest subvention, initially from April 2007 to September 2008.

- Expanded to include more products and additional 2% subvention for certain goods, imposing a minimum interest rate of 7%.

Scheme Extensions and Conditions

- Second scheme covered employment-focused sectors from December 2008 to September 2009, extended to March 2010.

- Third scheme from April 2010 to March 2011 with specific interest rate conditions.

- Additional sectors added over time, including leather, engineering, and textiles.

Interest Rate Adjustment

- With Base Rate System from July 2010, banks adjusted rates for eligible sectors by the subvention amount, maintaining a 7% floor rate.

- Interest rate reductions due to subvention are not considered a Base Rate violation.

Obligations and Reimbursements

- Banks must pass the full subvention benefit to exporters and claim reimbursement from RBI.

- Reimbursement claims are to be certified by external auditors and submitted quarterly.

Interest Equalisation Scheme on Pre and Post-Shipment Rupee Export Credit

Background

- Scheme initiated in April 2015.

- Initially valid for 5 years, extended due to COVID.

- Currently capped at Rs 10 Cr per annum per IEC.

- Banks that lend to exporters at an average rate of more than Repo + 4% would be debarred under the Scheme.

- Aimed at supporting exporters from identified sectors and MSMEs.

- Approved by the Union Cabinet until June 30, 2024.

Implementation Strategy

- Implemented by RBI through Public and Non-Public Sector Banks.

- Jointly monitored by DGFT and RBI.

Latest RBI Circular (February 22, 2024)

- RBI extends the Interest Equalization Scheme (IES) on Pre and Post Shipment Rupee Export Credit until June 30, 2024.

- Offers 2% interest equalization for manufacturers and merchant exporters in specified 410 HS lines and 3% for MSME manufacturers across any HS line.

- Restrictions on banks charging over Repo Rate + 4% before subvention.

- Cap on the annual net subvention amount at Rs 10 Cr per IEC.

Category-wise Rates

| Category of Exporters | Rate of Interest Equalisation |

|---|---|

| Manufacturer and Merchant Exporters exporting products listed in the 410 tariff lines | 2% |

| MSME exporters of all tariff lines | 3% |

Exclusions

- Telecom Instruments sector, except for MSME manufacturer exporters, is excluded from the Scheme.

- Beneficiaries availing benefits under any Production Linked Incentive (PLI) scheme are not eligible for the extended Scheme.

Post-Shipment Export Finance in Foreign Currency

- Banks can use their own foreign currency holdings, such as EEFC, RFC, and FCNR(B) accounts, to discount export usance bills.

- Rediscounting export bills overseas is possible at international rates.

- A collective bills portfolio facility is often more accessible than individual bill rediscounting abroad.

- Banks can set up a Bankers Acceptance Facility (BAF) for rediscounting bills, which requires no margin and is secured by collateral.

- Each bank can determine its BAF limit with foreign banks or rediscounting agencies, including factoring agencies, provided it's a 'without recourse' arrangement.

- Exporters can establish their own credit lines with foreign entities for direct bill discounting.

- Limits set by overseas entities under BAF are excluded from RBI's (FED) borrowing limit calculations for banks.

Eligibility Criteria (Rediscounting of Export Bills Abroad — EBR)

- Applicable mainly to export bills with a usance period of up to 180 days, including the shipping time and any grace period.

- Demand bills can be included if the foreign institution agrees.

- If the exporter is allowed to draw usance bills for more than 180 days per current FED rules, they may receive post-shipment credit under EBR for an extended period.

- Rediscounting can be conducted in any convertible currency.

- The EBR facility is also available for exports to Asian Clearing Union (ACU) member countries.

- Banks may centralize the BAF Scheme at a specific branch for ease of operation; other branches can also offer this service.

Source of On-shore Funds

- Demand bills should be processed using current post-shipment credit options or via foreign currency loans to exporters from banks' foreign currency balances.

- Banks may keep bills in their portfolio instead of rediscounting, but should access local markets if needed, to conserve foreign exchange.

- Inter-bank rediscounting is possible, allowing banks with unused BAF limits to assist others.

- Banks can obtain credit lines from domestic banks if unable to secure foreign loans or lacking overseas branches, ensuring the cost to exporters doesn't exceed 350 basis points over LIBOR/EURO LIBOR/EURIBOR.

- Banks can set their foreign currency export credit rates from May 5, 2012.

- Banks are allowed to use foreign loans and funds from buy-sell swaps in domestic forex for EBR facilities under specific conditions.

ECGC Cover

- 'With recourse' export bill rediscounting keeps existing ECGC coverage as exporter liability remains until bill settlement.

- 'Without recourse' rediscounting ends ECGC liability when bills are rediscounted.

- Banks cannot use export bills discounted under this scheme for RBI refinance.

- These discounted export bills should be reported separately from other export credit for refinance purposes.

- Foreign currency export credit interest rates depend on loan duration and comply with RBI guidelines.

Customer Service & Simplification of Procedure

- RBI is enhancing exporter competitiveness and efficiency by minimizing bank-related procedural delays.

Key Initiatives

- Encouraging banks to ensure timely and sufficient credit to exporters.

- Banks should offer essential services and advice on export procedures and opportunities.

- Creation of Export Counsel Offices in banks to support and guide exporters, especially the small-scale and non-traditional ones.

Gold Card Scheme for Exporters

- Available for all qualifying exporters, including small and medium enterprises.

- Excludes exporters flagged by ECGC or with over 10% overdue bills from the past year's turnover.

- Cardholders receive preferential credit terms, such as lower interest rates.

- Streamlined and expedited processing of credit applications for cardholders.

- Banks to outline specific benefits for Gold Card users, including lower service charges.

- Simplified procedures for sanctioning and renewing credit limits, with in-principle approval for three years and easy renewal conditions.

- Provision of a standby credit limit, at least 20% above the assessed limit, for sudden orders or seasonal fluctuations.

- Flexible inventory norms for unexpected large orders.

- Quick processing of requests: 25 days for new applications, 15 for renewals, and 7 days for ad-hoc requests.

- Priority given to Gold Card holders for foreign currency packing credit.

- Potential for collateral waivers and exemptions from ECGC guarantees based on the cardholder's credibility.

- Additional banking services like ATM, internet banking, and international debit/credit cards may be offered.

- Interest rates for Gold Card holders capped at general export credit rates and within RBI guidelines, with potential for further reduction based on performance.

- Extended interest rate benefits on post-shipment credit up to 365 days.

- Eligibility for foreign currency credit cards based on export proceeds realization history.

- Priority access to PCFC funds over non-export borrowers.

- Option for term loans in foreign currency from certain designated funds, excluding overseas borrowings.

Sanction of Export Credit Proposals

- Banks aim to approve new or increased export credit limits within 45 days and renew existing ones within 30 days. Ad hoc facilities should be processed within 15 days, except for Gold Card holders who have shorter timeframes.

- Ad hoc credit facilities should not incur additional interest charges.

- Export credit applications should be streamlined, with reduced data requirements for exporters.

- Banks can use different assessment methods (Projected Balance Sheet, Turnover, or Cash Budget) to determine exporters' working capital needs.

- Lines of Credit are normally set for one year but can extend up to three years and are subject to annual review. In case of renewal delays, current limits remain valid, and urgent credit needs should be met promptly.

- Requirement for submission of export orders or L/Cs for each disbursement can be waived for exporters with good track records; periodic statements are sufficient.

- Banks are tasked with ensuring that export credit needs are fully and promptly met at competitive rates and addressing any inefficiencies in credit delivery to the export sector.

- Export bills should be realized within 12 months; extensions are possible for genuine cases. Unsettled bills can be converted to rupee loans/terms, with ECGC claims lodged for defaults as necessary.

Other Points

- Before offering export finance, banks must refer to the Foreign Trade Policy and check the ECGC coverage and country risk profiles.

- Banks should adhere to their own guidelines regarding export credit, margin, and security requirements.

- A bank must assess the exporter's real financial needs and obtain all necessary documents at once for efficiency.

- Conduct pre-sanction inspections, perform due diligence, and strictly enforce KYC protocols.

- Banks are advised to be flexible regarding financial ratios and security standards but must ensure the proposal's viability and the borrower's integrity.

- Exporters need to demonstrate their ability to fulfill orders within set timelines.

- The bank should evaluate the exporter's experience in the trade.

- The amount of finance provided should align with the anticipated export turnover and input costs.

- Verify the standing of the L/C issuing bank and the terms of the L/C itself.

- For orders not covered by an L/C, banks should acquire a satisfactory status report on the foreign buyer, consulting ECGC or head office when necessary.

- Pre-shipment and post-shipment financing should be addressed concurrently.

- Pre-shipment finance can be accessed at any branch, but post-shipment finance is limited to designated branches ('A' or 'B' category).

- Employ various methods to assess export credit limits: Projected Turnover Method for smaller limits, MPBF Method, or Cash Budget Method.

- In a consortium setting, once MPBF is agreed upon, member banks should sanction limits promptly based on their share.

- Annually review export credit limits without disrupting ongoing finance arrangements.

- Meet urgent or additional financial needs on an ad hoc basis if there are delays in sanctioning regular limits.

Quick Notes for Exam

- Pre-shipment finance assists exporters with packing of goods, procuring raw materials, and transporting goods to the port — but NOT marketing expenses.

- The PCFC is considered up to the date of shipment.

- PCFC is intended to help exporters with procurement of raw materials and goods for export.

- The Whole-Turnover Packing Credit (ECIB-WTPC) guarantee fee is to be borne by the exporters.

- The WTPC guarantee helps exporters by covering all packing credit accounts.

- The primary reason for providing pre-shipment credit in foreign currency is to avoid currency exchange risk.

- Interest rate on rupee export credit advances should be at or above Base Rate.

- Exporters can avail a whole turnover guarantee under the WTPC scheme.

- ECGC offers coverage to both exporters and banks.

- The purpose of pre-sanction inspection in export finance is to ensure due diligence and compliance.

- The primary source of information on the buyer's country risk profile is Head Office or ECGC.

- In export finance, KYC compliance must be strict.

- The prime status of the L/C issuing bank determines the credibility and reliability of the payment.

- When an export order is not backed by an L/C, banks should obtain a satisfactory status report on the foreign buyer.

- Banks should ensure exporters' credit requirements are met in full and promptly at competitive rates.

- Upon delay in renewal, banks should allow existing sanctioned limits to continue uninterrupted.

- In case of non-realisation of export bills by due date, banks should convert the outstanding to a rupee loan/term.

- Banks should consider dispensation of export credit to be expeditious and timely.

- In case of delay in renewal of limits, banks should provide urgent requirements on an ad hoc basis by extending an interim ad hoc limit.

- Flexibility in banking terms for exporters should not compromise the viability of the proposal.

- Under a consortium arrangement, banks are required to process proposals within a set time frame after MPBF approval.

- Pre-shipment and post-shipment limits should be considered simultaneously and in full.

- The Fixed Asset Method is NOT used for assessing export credit limits — only Projected Turnover, MPBF, or Cash Budget methods.

- Post-shipment finance includes all of the following EXCEPT pre-shipment export credit: Export Bills Purchased/Discounted, Advance against Bills sent for Collection, Advance against Export on Consignment Basis.

- The sanctioned export credit should be reviewed annually.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Two Stages | Pre-shipment (before shipment) and Post-shipment (after shipment) |

| Pre-shipment Forms | Rupee EPC, PCFC, ECGC advances, Duty Drawback, Advance against export receipts |

| EPC Purpose | Working capital for purchasing, processing, manufacturing, packing |

| EPC Max Duration | 360 days from date of advance |

| IEC Code | 10-digit, lifetime validity, issued by DGFT |

| Loan Amount | Lower of FOB value or domestic production cost |

| RBI Refinance | Stopped direct refinance; uses special term repo instead |

| Dr. Urjit Patel | Recommended RBI stop direct refinance for export credit |

| Liquidation of EPC | Conversion to post-shipment credit, EEFC/DDA proceeds |

| Running Account | Pre-shipment without immediate LC proof; FIFO system; max 360 days |

| Running Account — Not For | Sub-suppliers |

| STC/MMTC Credit | Via Export Order Holder; ECGC guarantee may be required |

| PCFC Max Duration | 360 days; adjusted at T.T. selling rate if no export |

| PCFC Liquidation | Export document proceeds, EEFC balances, foreign currency loans |

| PCFC Cancellation | Buy foreign exchange; pay ECNOS rate + penalty |

| PCFC Forward Contracts | Allowed on confirmed orders; can cancel when PCFC used |

| PCFC Sharing | Between export order holder and manufacturer; within EOU/EPZ/SEZ |

| Deemed Exports | PCFC applicable; cleared within 30 days at post-supply stage |

| DDA Scheme | Diamond trade entities; RBI Circular No.13, October 29, 2009 |

| Post-shipment Period | Up to 12 months after shipment for proceeds collection |

| Post-shipment Modes | Bill purchase/discount, negotiation, advances against collection/consignment/undrawn balances/duty drawback |

| NTP | Normal Transit Period; typically 25 days per FEDAI |

| Demand Bills | Advance for NTP as specified by FEDAI |

| Usance Bills | Max 365 days from shipment (incl. NTP) |

| Retention Money | For turnkey/construction; no advances on service-related retention |

| WTPSG | Whole Turnover Post Shipment Guarantee — bank secures this |

| D.P. vs D.A. | D.P. = bank control until payment; D.A. = control released on acceptance |

| Document Discrepancies | 14 common types (late negotiation, excess amount, port mismatch, etc.) |

| Consignment Exports | Equal footing with cash terms for interest; max 1 year expected payment |

| Gem Exports | May not close pre-shipment within 365 days; special post-shipment account |

| Duty Drawback Advances | Subject to ECGC guarantee; need EGM Number from Customs |

| ECGC WTPSG | Bank absorbs premium cost; leads to lower capital charges |

| Base Rate System | From July 1, 2010 for rupee export credit |

| Pre-BPLR Rate | Capped at BPLR minus 2.5% until June 30, 2010 |

| Current Rate | Based on 1-year MCLR minus Interest Equalisation + bank spread |

| Pre-shipment Credit Period | Up to 270 days |

| ECNOS | Export Credit Not Otherwise Specified; when not repaid within 360 days |

| ECNOS Penalty | Domestic lending rate + penalty; no additional penalty on ECNOS category |

| Interest Equalisation | 2% subvention initially (April 2007); 7% floor rate |

| IES (2015 Scheme) | Initiated April 2015; cap Rs 10 Cr/annum per IEC |

| IES Rate — 410 HS Lines | 2% for manufacturer & merchant exporters |

| IES Rate — MSME | 3% for MSME manufacturers across all tariff lines |

| IES Bank Cap | Banks charging over Repo + 4% are debarred |

| IES Exclusion | Telecom Instruments (except MSME); PLI scheme beneficiaries |

| IES Extended Until | June 30, 2024 (RBI circular Feb 22, 2024) |

| EBR Usance | Up to 180 days including shipping time and grace |

| EBR Currency | Any convertible currency; available for ACU member countries |

| BAF | Bankers Acceptance Facility; no margin; secured by collateral |

| EBR Cost Cap | Max 350 bps over LIBOR/EURO LIBOR/EURIBOR |

| FC Export Credit Rates | Banks can set own rates from May 5, 2012 |

| With Recourse | ECGC coverage continues until bill settlement |

| Without Recourse | ECGC liability ends on rediscounting |

| Gold Card Eligibility | All exporters incl. SMEs; excludes ECGC-flagged or >10% overdue |

| Gold Card — Standby Limit | At least 20% above assessed limit |

| Gold Card — Processing | New: 25 days; Renewal: 15 days; Ad hoc: 7 days |

| Gold Card — Post-shipment | Interest rate benefits up to 365 days |

| Gold Card — In-Principle | Approval for 3 years with easy renewal |

| Sanction — New Limits | Within 45 days |

| Sanction — Renewal | Within 30 days |

| Sanction — Ad Hoc | Within 15 days; no additional interest charges |

| Assessment Methods | Projected Balance Sheet, Turnover, Cash Budget |

| LOC Duration | Set for 1 year; extendable up to 3 years; annual review |

| Bill Realization | Within 12 months; unsettled → rupee loan conversion |