🏛️ Capital Structure & Pillars

Understanding the evolution of Basel norms, the 3 Pillars, and implementation of Pillar 1 Capital Standards in India.

Common Risk Terms for Bankers

- Credit Risk: Arising on account of possible default by borrower to repay the loan.

- Market Risk: Arising on account of changes in the value of investment in govt. securities, gold or forex, held by the bank, due to change in market variables.

- Interest Rate Risk: Arising due to change in interest rates. It is part of market risk.

- Liquidity Risk: Arising due to mismatch in residual maturity period of assets and liabilities. This is of short term nature. It is part of market risk.

- Settlement Risk: Inability of a bank to settle due the payments due to other banks.

- Systemic Risk: Impact of failure of one bank on other banks / banking system.

- Operational Risk: Arising due to (1) errors by staff or (2) inadequate or failed systems or (3) external reasons. (for example opening of account without complying with KYC).

- Legal Risk: Defective documentation (it is an operational risk).

Introduction to Basel Norms

Why Do We Need Banking Regulations?

Banks are special institutions that hold public money (deposits). Unlike other businesses, if a bank fails:

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Common Risk Terms for Bankers

- Credit Risk: Arising on account of possible default by borrower to repay the loan.

- Market Risk: Arising on account of changes in the value of investment in govt. securities, gold or forex, held by the bank, due to change in market variables.

- Interest Rate Risk: Arising due to change in interest rates. It is part of market risk.

- Liquidity Risk: Arising due to mismatch in residual maturity period of assets and liabilities. This is of short term nature. It is part of market risk.

- Settlement Risk: Inability of a bank to settle due the payments due to other banks.

- Systemic Risk: Impact of failure of one bank on other banks / banking system.

- Operational Risk: Arising due to (1) errors by staff or (2) inadequate or failed systems or (3) external reasons. (for example opening of account without complying with KYC).

- Legal Risk: Defective documentation (it is an operational risk).

Introduction to Basel Norms

Why Do We Need Banking Regulations?

Banks are special institutions that hold public money (deposits). Unlike other businesses, if a bank fails:

- Depositors lose their life savings

- Loans stop flowing to businesses and individuals

- The entire economy can collapse (as seen in 2008)

This is why governments worldwide regulate banks to ensure they are financially strong and can survive difficult times.

BCBS (Basel Committee on Banking Supervision)

Think of BCBS as: The "Supreme Court of Banking Rules" – they set the global standards that all countries follow.

- Origin: The Bank Herstatt failure in 1974 (a German bank) resulted in massive losses to many banks worldwide. When Herstatt collapsed, it left many international transactions incomplete, causing a domino effect of losses. This crisis prompted G-10 countries (the world's richest nations at the time) to form the Basel Committee on Banking Supervision (BCBS) in 1974.

- Headquarters: Located under the Bank for International Settlements (BIS) in Basel, Switzerland – hence the name "Basel" norms.

- Membership: Central banks of most countries (including RBI for India) are members of BCBS, and its recommendations are implemented by them. However, BCBS doesn't have legal authority – it only provides guidelines that member countries voluntarily adopt.

Evolution of Basel Norms

Basel I (1988)

The first global banking standard. Focused only on **Credit Risk** – the risk that borrowers won't repay loans. Required banks to maintain minimum capital of 8% of Credit RWAs. Implemented in India in 1993. In 1996, **Market Risk** RWA was added.

Basel II (2006)

Added **Operational Risk** (fraud, system failures, etc.) to the calculation. Introduced the famous **Three Pillar Structure**. Made the framework more risk-sensitive. Introduced in India w.e.f. 31.03.2008.

Basel III (2010)

Born from the 2008 global financial crisis. Made capital requirements **stricter and higher quality**. Added new concepts like Capital Buffers and Liquidity Ratios. Result of the Pittsburgh G-20 summit.

Why Was Basel III Needed? (The 2008 Story)

The 2008 Global Financial Crisis exposed fatal flaws in Basel II:

| Problem | What Happened | Basel III Solution |

|---|---|---|

| Low quality capital | Banks counted risky instruments as "capital" | Stricter definition of capital (CET1 focus) |

| Not enough capital | 8% was too low to absorb losses | Higher capital requirements (11.5% with buffers) |

| No buffers | Banks had no extra cushion for crisis | Added Capital Conservation Buffer |

| Liquidity crisis | Banks couldn't meet short-term obligations | Introduced LCR and NSFR ratios |

Real Example: Lehman Brothers (USA) had a capital ratio that looked healthy on paper, but much of it was low-quality capital. When the crisis hit, this "capital" evaporated, and the bank collapsed overnight.

Basel III Overview

- Main Objective: To improve the banking sector's ability to absorb shocks arising from financial and economic stress, thereby reducing the risk of spillover from the financial sector to the real economy.

- Officially Called: A global regulatory framework for more resilient banks and banking system.

Key Changes from Basel II

- Quality of Capital ↑ – More focus on equity (CET1)

- Quantity of Capital ↑ – Higher minimum ratios

- Capital Buffers (NEW) – Extra capital for crisis times

- Liquidity Standards (NEW) – LCR and NSFR ratios

- Leverage Ratio (NEW) – Non-risk based backstop

Implementation in India

| Milestone | Date |

|---|---|

| Basel III began | 01.04.2013 |

| Full implementation (including CCB) | 01.10.2021 |

| Timeline | Phased over 8+ years |

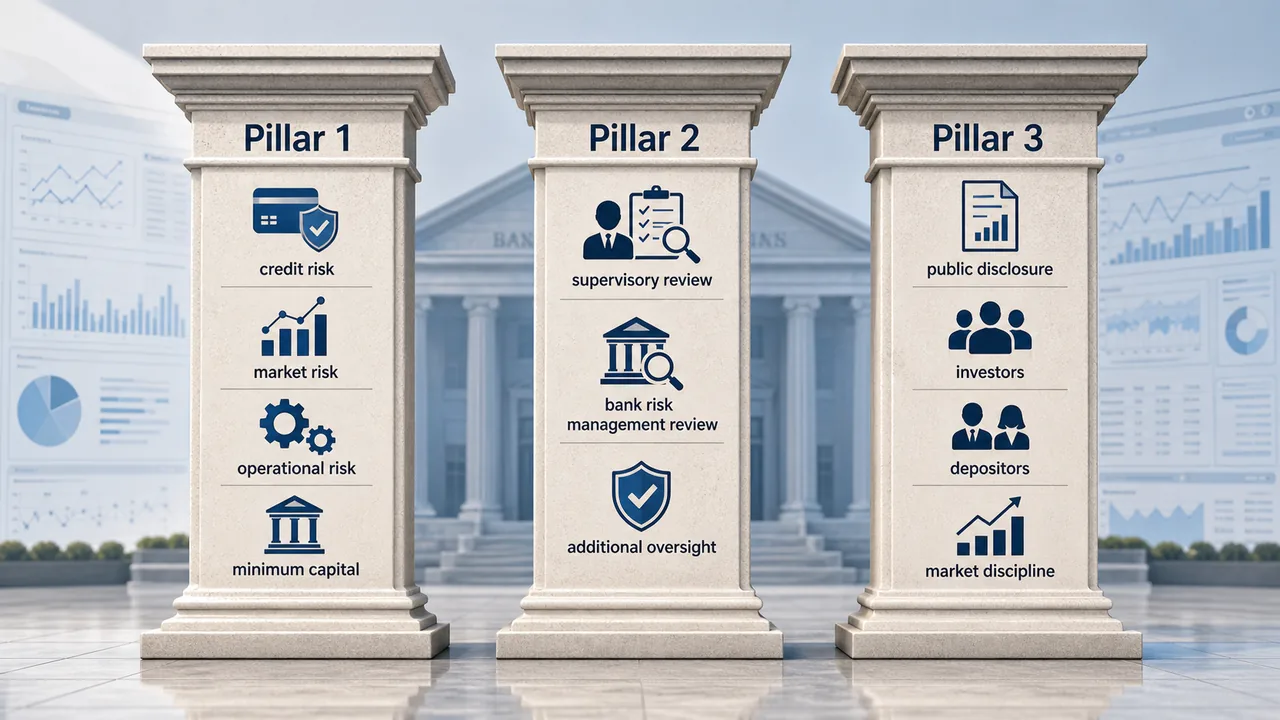

The 3 Pillars Structure

Basel III (like Basel II) is built on three pillars – think of them as three legs of a stool. All three are essential for stability:

📊 Pillar 1

Minimum Capital Standard

**Quantitative requirement** – How much capital a bank must hold. This is the "mathematical" pillar that calculates required capital ratios.

🔍 Pillar 2

Supervisory Review (SREP)

**Qualitative oversight** – RBI reviews each bank's internal risk management. Can demand additional capital if needed. Catches risks not covered in Pillar 1.

📢 Pillar 3

Market Discipline

**Transparency** – Banks must publicly disclose their risk exposure and capital. Allows public, investors, and analysts to assess bank health.

Analogy: Think of buying a car. Pillar 1 = The car must have airbags (mandatory safety equipment). Pillar 2 = A mechanic inspects the car for hidden issues. Pillar 3 = The car's safety ratings are published for all to see.

Pillar 1: Minimum Capital Standards (Deep Dive)

Under Pillar 1, banks must maintain a minimum capital ratio to cover three types of risks:

The Three Risks Covered

| Risk Type | What It Covers | Example |

|---|---|---|

| Credit Risk | Borrowers defaulting on loans | A company takes a loan but goes bankrupt |

| Market Risk | Losses from price movements | Bank holds bonds, interest rates rise, bond prices fall |

| Operational Risk | Fraud, system failures, human error | Employee commits fraud; server crashes during trading |

Understanding Risk-Weighted Assets (RWAs)

Key Concept: Not all assets are equally risky. A loan to the Government is safer than a loan to a startup. So we "weight" assets by their risk.

Example of Risk Weights:

- Cash and Government Securities: 0% risk weight (safest)

- Home loans (up to ₹75 lakhs): 35% risk weight (secured by house)

- Personal loans (unsecured): 100% risk weight (no collateral)

- Equity investments: 125% risk weight (high volatility)

Calculation Example: If a bank has ₹100 crore in personal loans (100% RW) and ₹100 crore in home loans (35% RW):

- Personal loans RWA = ₹100 cr × 100% = ₹100 cr

- Home loans RWA = ₹100 cr × 35% = ₹35 cr

- Total RWA = ₹135 cr (not ₹200 cr)

Regulatory Capital Ratios

1. Common Equity Tier 1 (CET1) Ratio

What it measures: The proportion of a bank's highest quality capital (equity) relative to its risk-weighted assets.

Why it matters: CET1 is the purest form of capital – it's shareholders' money that can absorb losses immediately. A higher CET1 ratio means the bank can survive bigger shocks without failing.

| Requirement | India 🇮🇳 | BCBS 🌍 |

|---|---|---|

| Minimum CET1 Ratio | 5.5% | 4.5% |

Note: India was conservative and implemented higher requirements than BCBS minimum, learning from the global crisis.

Example: If a bank has CET1 Capital of ₹5,500 crore and Total RWAs of ₹100,000 crore:

- CET1 Ratio = 5,500 / 100,000 = 5.5% (just meets India's minimum)

2. Tier 1 Capital Ratio

What it measures: The proportion of a bank's going concern capital (CET1 + Additional Tier 1) relative to its risk-weighted assets.

Why it matters: Tier 1 capital includes both CET1 and AT1 instruments. This is capital available to absorb losses while the bank continues to operate. It's the first line of defense.

| Requirement | India 🇮🇳 | BCBS 🌍 |

|---|---|---|

| Minimum CET1 Ratio | 5.5% | 4.5% |

| Minimum AT1 Ratio | 1.5% | 1.5% |

| Minimum Tier 1 Ratio | 7.0% | 6.0% |

Eligible Tier 1 Capital = CET1 Capital + Additional Tier 1 Capital (AT1)

Example: If a bank has CET1 of ₹5,500 cr, AT1 of ₹1,500 cr, and RWAs of ₹100,000 cr:

- Tier 1 Capital = 5,500 + 1,500 = ₹7,000 cr

- Tier 1 Ratio = 7,000 / 100,000 = 7.0% (meets India's minimum)

3. Capital to Risk-Weighted Assets Ratio (CRAR)

What it measures: The proportion of a bank's total regulatory capital (Tier 1 + Tier 2) relative to its risk-weighted assets.

Why it matters: CRAR is the most comprehensive capital ratio. It includes all forms of capital – both going concern (Tier 1) and gone concern (Tier 2). This is the headline ratio that banks report and RBI monitors closely.

| Requirement | India 🇮🇳 | BCBS 🌍 |

|---|---|---|

| Minimum CET1 Ratio | 5.5% | 4.5% |

| Minimum AT1 Ratio | 1.5% | 1.5% |

| Minimum Tier 1 Ratio | 7.0% | 6.0% |

| Minimum Tier 2 Ratio | 2.0% | 2.0% |

| Minimum CRAR | 9.0% | 8.0% |

| With CCB | 11.5% | 10.5% |

Eligible Total Capital = Tier 1 Capital + Tier 2 Capital

Example: If a bank has Tier 1 of ₹7,000 cr, Tier 2 of ₹2,000 cr, and RWAs of ₹100,000 cr:

- Total Capital = 7,000 + 2,000 = ₹9,000 cr

- CRAR = 9,000 / 100,000 = 9.0% (meets India's minimum)

Note: CRAR stands for Capital to Risk-weighted Asset Ratio. This is the main ratio that banks must maintain and is reported in quarterly results.

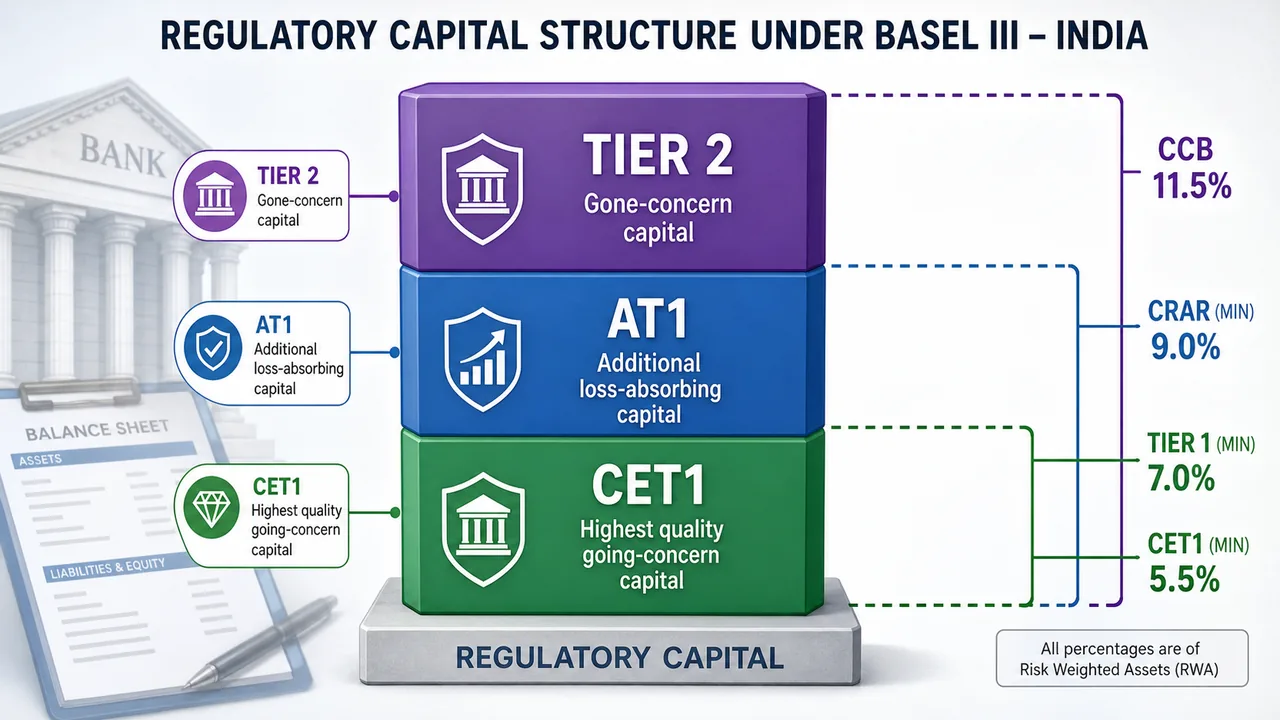

Components of Regulatory Capital

Why Different Tiers?

Capital is classified into tiers based on quality – how easily it can absorb losses:

| Tier | Quality | Loss Absorption | When Used |

|---|---|---|---|

| CET1 | Highest | First to absorb losses | While bank is operating (going concern) |

| AT1 | High | Absorbs losses before Tier 2 | Can be converted to equity if bank struggles |

| Tier 2 | Medium | Last resort | When bank is being wound up (gone concern) |

1. Common Equity Tier 1 (CET1) Capital

Called: Going Concern Capital or Core Capital – available to absorb losses while the bank continues operating.

This is the HIGHEST QUALITY capital because:

- It's permanent (no maturity date)

- No fixed dividend obligation

- First to absorb losses

- Owners bear the risk, not depositors

Components of CET1:

| Item | Explanation |

|---|---|

| 1. Common shares (paid-up equity) | Money shareholders actually paid for shares |

| 2. Share premium | Extra amount paid above face value (e.g., paid ₹100 for ₹10 share, so ₹90 is premium) |

| 3. Statutory reserves | Reserves required by law (e.g., 25% of profits to reserve fund) |

| 4. Capital reserves | Profit from selling assets (not from regular business) |

| 5. Other disclosed free reserves | Any other reserves available for losses |

| 6. Previous year P&L balance | Accumulated profit retained in the business |

| 7. Revaluation reserve @ 55% discount | If land is revalued upward, only 45% counts (conservative approach) |

| 8. Forex Translation Reserves @ 25% discount | Gains from foreign currency translation, only 75% counts |

| 9. Current year profit (completed quarter) | Only counts after the quarter ends and is audited |

Why Discounts? Revaluation gains and forex gains are unrealized – the bank hasn't actually sold the asset. So regulators say "don't count all of it, be conservative."

2. Additional Tier 1 (AT1) Capital

Hybrid instruments – between equity and debt. They can absorb losses, but not as well as CET1.

Key Instruments:

- Perpetual Non-Cumulative Preference Shares (PNCPS) – No fixed maturity, and if dividend is skipped one year, it's gone forever (non-cumulative)

- Perpetual Debt Instruments (PDIs) – Like a bond but never matures

Limits in AT1:

- PNCPS: Maximum 1.5% of RWAs

- Total AT1: Maximum 1.5% of RWAs (India) or difference to reach 7% T1

Yes Bank AT1 Wipe-off (2020): When Yes Bank was struggling, RBI wrote off ₹8,415 crore of AT1 bonds to zero. Investors lost everything. This is the "loss absorption" feature in action – painful for investors, but it saved depositors.

3. Tier 2 Capital Funds

Called: Gone Concern Capital – used only when the bank is being shut down/resolved.

Components:

| Item | Details |

|---|---|

| 1. General Provisions & Loan Loss Reserves | Money set aside for expected loan losses. Max 1.25% of RWAs (under Internal Ratings Based Approach: max 0.6%) |

| 2. Tier-2 Debt Instruments | Subordinated debt with minimum 5-year maturity |

| 3. Preference Shares | Perpetual Cumulative, Redeemable Non-Cumulative, or Redeemable Cumulative |

| 4. Stock Surplus | Share premium from preference share issuance |

Worked Example:

- Given: General Provisions = Rs. 1950 cr; RWAs = Rs. 100,000 cr.

- Question: How much can be included in Tier-2?

- Solution: Max limit = 1.25% of RWAs = 100,000 × 1.25% = ₹1250 cr

- Since 1950 > 1250, only Rs. 1250 cr can be included. The excess ₹700 cr doesn't count.

Minimum Capital Requirements Table (As % of RWAs)

| Requirements | India 🇮🇳 | BCBS (Global) 🌍 | Difference |

|---|---|---|---|

| 1. Min CET1 Ratio | 5.5% | 4.5% | +1.0% |

| 2. Additional Tier 1 Ratio | 1.5% | 1.5% | Same |

| 3. Min Tier 1 Ratio (1+2) | 7.0% | 6.0% | +1.0% |

| 4. Tier 2 Capital Ratio | 2.0% | 2.0% | Same |

| 5. Min Total Capital (CRAR) (3+4) | 9.0% | 8.0% | +1.0% |

| 6. Capital Conservation Buffer (CCB) | 2.5% | 2.5% | Same |

| 7. Min Capital + CCB (5+6) | 11.5% | 10.5% | +1.0% |

| 8. Min CET1 + CCB (1+6) | 8.0% | 7.0% | +1.0% |

Why is India Stricter? After the 2008 crisis, RBI decided to be more conservative. Indian banks are also more exposed to sectors like agriculture and MSMEs which can be volatile. The extra 1% buffer provides additional safety.

Quick Memory Tips 🧠

For CET1 Requirements (India):

- CET1 alone: 5.5% (remember: "5.5 is the CET1 MIN")

- With CCB: 8.0% (5.5 + 2.5 = 8%)

For Total Capital (India):

- CRAR minimum: 9% (remember: "9 lives of a bank")

- With CCB: 11.5% (9 + 2.5 = 11.5%)

Tier Structure:

- CET1 = Core (highest quality)

- AT1 = Additional (still Tier 1, but lesser quality)

- Tier 2 = Gone concern (for resolution only)

Key Takeaways

- Basel norms exist because bank failures hurt everyone – not just shareholders, but depositors and the entire economy.

- Basel III was born from the 2008 crisis – requiring higher quality and quantity of capital.

- Three Pillars work together: Minimum capital (P1) + Supervision (P2) + Transparency (P3).

- Not all capital is equal: CET1 > AT1 > Tier 2 in terms of quality and loss absorption.

- India is stricter than BCBS minimums by 1% across the board – a conservative approach.

- RWAs make capital requirements risk-sensitive – riskier assets require more capital.

References

- Basel III: A global regulatory framework for more resilient banks and banking systems – Bank for International Settlements (BIS), December 2010 (revised June 2011) – https://www.bis.org/publ/bcbs189.htm

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| BCBS | Basel Committee on Banking Supervision; formed 1974 after Bank Herstatt failure; HQ at BIS, Basel, Switzerland; issues guidelines (not legally binding) adopted by member central banks |

| Basel I (1988) | First global standard; covered Credit Risk only; min capital 8% of Credit RWAs; implemented in India 1993; Market Risk RWA added in 1996 |

| Basel II (2006) | Added Operational Risk; introduced Three Pillar Structure; implemented in India w.e.f. 31.03.2008 |

| Basel III (2010) | Response to 2008 global financial crisis (Pittsburgh G-20 summit); stricter & higher-quality capital; added Capital Buffers, LCR, NSFR, Leverage Ratio |

| Basel III in India | Began 01.04.2013; full implementation (incl. CCB) 01.10.2021 |

| Pillar 1 — Minimum Capital Standard | Quantitative — calculates how much capital a bank must hold against Credit, Market & Operational Risk RWAs |

| Pillar 2 — Supervisory Review (SREP) | Qualitative — RBI reviews each bank's internal risk management; can demand additional capital |

| Pillar 3 — Market Discipline | Transparency — banks must publicly disclose risk exposure and capital adequacy |

| Risk-Weighted Assets (RWAs) | Assets weighted by risk level: Govt. securities 0%, home loans (≤₹75L) 35%, personal loans 100%, equity 125% |

| CET1 Ratio (India) | 5.5% of RWAs (BCBS: 4.5%); CET1 = Common Equity Tier 1 Capital ÷ Total RWAs |

| Tier 1 Ratio (India) | 7.0% (CET1 5.5% + AT1 1.5%); BCBS: 6.0% |

| CRAR / Total Capital Ratio (India) | 9.0% (Tier 1 7% + Tier 2 2%); BCBS: 8.0% |

| With CCB (India) | 11.5% (CRAR 9% + CCB 2.5%); Min CET1 + CCB = 8.0% |

| India vs BCBS | India is +1% stricter across CET1, Tier 1, and CRAR |

| CET1 Capital (Going Concern / Core) | Highest quality; includes paid-up equity, share premium, statutory reserves, capital reserves, free reserves, retained earnings, revaluation reserve @55% discount, forex translation reserve @25% discount, current quarter profit |

| AT1 Capital | Hybrid instruments: PNCPS (Perpetual Non-Cumulative Preference Shares) & PDIs (Perpetual Debt Instruments); max 1.5% of RWAs |

| Yes Bank AT1 (2020) | RBI wrote off ₹8,415 crore AT1 bonds — loss-absorption feature in action |

| Tier 2 Capital (Gone Concern) | Used when bank is wound up; includes General Provisions (max 1.25% of RWAs), subordinated debt (min 5-yr maturity), preference shares, stock surplus |

| Capital quality hierarchy | CET1 (highest) > AT1 > Tier 2 (lowest) |

| Capital Conservation Buffer (CCB) | 2.5% of RWAs; same for India and BCBS |

Lesson Doubts

Ask questions, get expert answers