🛡️ Risk Weighted Assets & Capital Buffers

Calculating Risk Weighted Assets (RWA), Capital Adequacy Ratio (CAR), and understanding Capital Buffers.

Risk Weighted Assets (RWA)

Calculation of RWA involves aggregating risk across three main categories. The approaches for calculation range from simple standardized methods to advanced internal models:

💳 Credit Risk

- Standardized Approach

- Internal Rating Based (IRB) Approach (Foundation & Advanced)

📈 Market Risk

- Standardized Approach (Maturity & Duration Method)

- Internal Risk Management Model

⚠️ Operational Risk

- Basic Indicator Approach

- Standardized Approach

- Advanced Measurement Approach

1. Risk Weight for Credit Risk

A. Standard Risk Weights

In the Standardized Approach, risk weights are assigned based on the type of borrower and asset quality:

| Asset / Exposure | Risk Weight |

|---|---|

| Cash balance, balance with RBI | 0% |

| Central & State Govt. Claims, Loans guaranteed by Central Govt (DICGC, CGTMSE) | 0% |

| Loans guaranteed by State Govt. / ECGC | 20% |

| Secured staff loans | 20% |

| Long term loans to domestic corporate or PDs with AAA rating | 20% |

| Claims on Domestic Banks with 100% Capital Compliance | 20% |

| Personal loans, Consumer loans | 125% |

| Capital Market Exposure | 125% |

| Credit Cards | 150% |

B. Off-balance sheet items

For items like Bank Guarantees or Letters of Credit, the risk is calculated in a 2-stage process:

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Risk Weighted Assets (RWA)

Calculation of RWA involves aggregating risk across three main categories. The approaches for calculation range from simple standardized methods to advanced internal models:

💳 Credit Risk

- Standardized Approach

- Internal Rating Based (IRB) Approach (Foundation & Advanced)

📈 Market Risk

- Standardized Approach (Maturity & Duration Method)

- Internal Risk Management Model

⚠️ Operational Risk

- Basic Indicator Approach

- Standardized Approach

- Advanced Measurement Approach

1. Risk Weight for Credit Risk

A. Standard Risk Weights

In the Standardized Approach, risk weights are assigned based on the type of borrower and asset quality:

| Asset / Exposure | Risk Weight |

|---|---|

| Cash balance, balance with RBI | 0% |

| Central & State Govt. Claims, Loans guaranteed by Central Govt (DICGC, CGTMSE) | 0% |

| Loans guaranteed by State Govt. / ECGC | 20% |

| Secured staff loans | 20% |

| Long term loans to domestic corporate or PDs with AAA rating | 20% |

| Claims on Domestic Banks with 100% Capital Compliance | 20% |

| Personal loans, Consumer loans | 125% |

| Capital Market Exposure | 125% |

| Credit Cards | 150% |

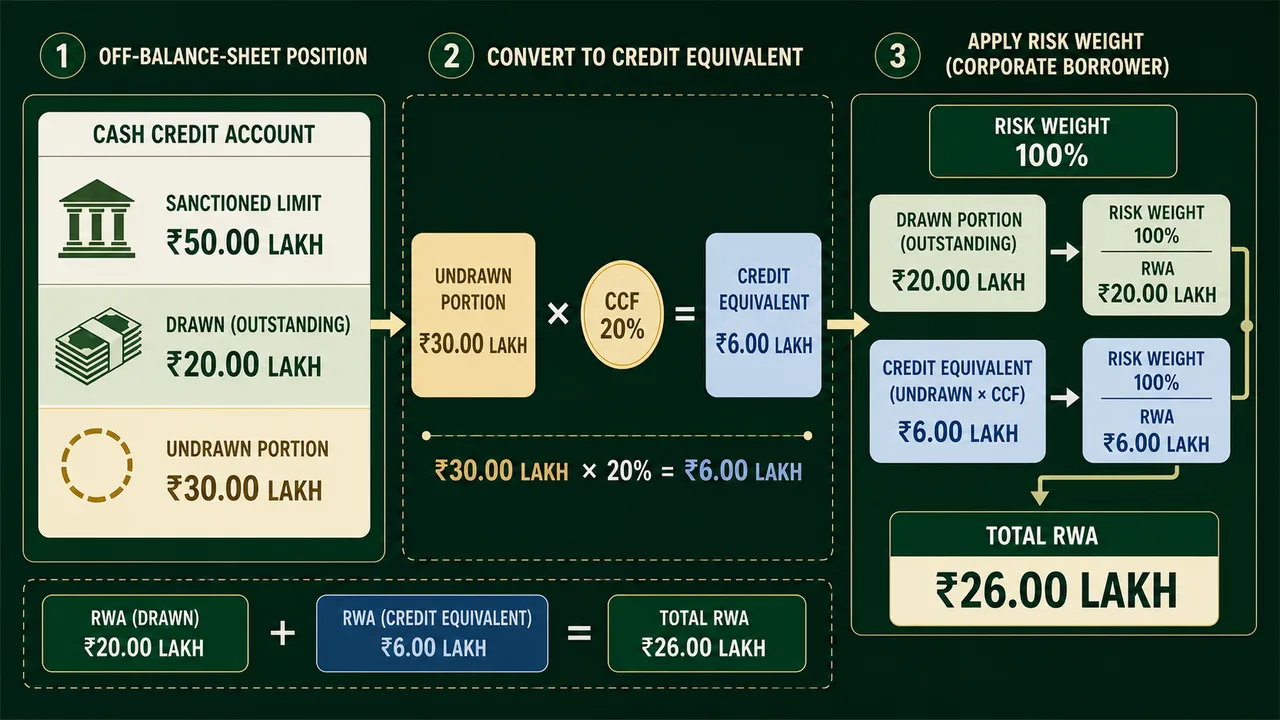

B. Off-balance sheet items

For items like Bank Guarantees or Letters of Credit, the risk is calculated in a 2-stage process:

- Step 1: Convert the Notional amount into a Credit Equivalent Amount using a Credit Conversion Factor (CCF).

- Step 2: Multiply the Credit Equivalent by the Risk Weight of the counterparty.

Common CCFs:

- 100% for direct credit substitute (e.g., Bank Guarantee, Standby LC).

- 20% for undrawn portion of Cash Credit.

Example Calculation:

A company (XYZ) has a sanctioned Cash Credit limit of ₹50 lakh. It has used ₹20 lakh. The undrawn portion is ₹30 lakh.

- Step 1 (Convert): ₹30 lakh (Undrawn) × 20% (CCF) = ₹6 lakh (Credit Equivalent)

- Step 2 (Risk Weight): If XYZ has a risk weight of 100%:

- Drawn Portion RWA: ₹20 lakh × 100% = ₹20 lakh

- Undrawn Portion RWA: ₹6 lakh × 100% = ₹6 lakh

- Total RWA = ₹26 lakh

2. Capital for Operational Risk

What is Operational Risk? It is the risk of loss resulting from inadequate or failed internal processes, people, and systems or from external events.

- Examples: Employee fraud (People), Server crash (System), Fire at a branch (External), Wrong transaction processing (Process).

Unlike Credit Risk (borrower defaults) or Market Risk (stock prices fall), this risk is "internal" to the bank's functioning.

How is Capital Calculated? Banks can choose one of three approaches, depending on their sophistication:

A. Basic Indicator Approach (BIA)

- Who uses it? Small banks with simple operations.

- Logic: "Higher Income = Higher Risk".

- Calculation: Bank must hold capital equal to 15% (Alpha factor) of the average positive annual gross income over the previous three years.

- Formula:

B. The Standardized Approach (TSA)

- Who uses it? Medium-sized banks.

- Logic: Different business lines have different risks. Retail banking is safer than Stock Trading.

- Calculation: The bank's activities are divided into 8 Business Lines. Each line has a specific "Beta factor" (capital requirement) ranging from 12% to 18%.

| Business Line | Beta Factor (Capital Charge) | Risk Level |

|---|---|---|

| Retail Banking, Asset Management | 12% | Low |

| Commercial Banking, Agency Services | 15% | Medium |

| Trading & Sales, Payment & Settlement | 18% | High |

Analogy: Think of BIA as a "Flat Tax" (everyone pays 15%). Think of TSA as "GST" (different rates for different goods - 12%, 18% etc.).

C. Advanced Measurement Approach (AMA)

- Who uses it? Large, sophisticated international banks.

- Logic: "We understand our risks better than a generic formula."

- Calculation: Banks use their own internal statistical models to estimate potential losses based on historical data. Requires RBI approval.

Overall Capital Adequacy Ratio (CAR)

The Capital Adequacy Ratio (also called CRAR) measures whether a bank has enough capital to cover its total risks.

{" "} × 100Calculation Steps

- For Credit Risk: Calculate RWA directly using risk weights (e.g., Asset × 100%).

- For Market & Operational Risk: You are usually given the "Capital Charge". To convert this to RWA:

(Why 9%? Because in India, for every ₹100 of RWA, banks must hold ₹9 capital. So, RWA = Capital / 9%)

Detailed Example

Given:

- Credit RWA = ₹100,000 cr

- Capital Charge for Market Risk = ₹1,800 cr

- Capital Charge for Operational Risk = ₹1,260 cr

- Total Capital Funds Available = ₹15,000 cr

Step 1: Convert Capital charges to RWA

- Market Risk RWA = 1,800 / 9% = ₹20,000 cr

- Operational Risk RWA = 1,260 / 9% = ₹14,000 cr

Step 2: Aggregate Total RWA

- Total RWA = 100,000 (Credit) + 20,000 (Market) + 14,000 (Ops) = ₹134,000 cr

Step 3: Calculate CAR

× 100 = **11.19%**Pillar 2: Supervisory Review Process

Objective: To ensure banks have adequate capital to support all risks (including those not captured in Pillar 1) and to encourage better risk management.

4 Principles of Supervisory Review (SREP)

- ICAAP (Internal Capital Adequacy Assessment Process): Banks must have their own process to assess how much capital they need.

- SREP (Supervisory Review & Evaluation Process): RBI reviews the bank's ICAAP to check if it's realistic.

- Capital above Minimum: RBI expects banks to hold capital above the minimum regulatory ratios to cover uncertainties.

- Early Intervention: RBI will intervene early to prevent capital from falling below minimum levels (e.g., via Prompt Corrective Action or PCA).

Pillar 3: Market Discipline

Objective: To use "market pressure" to ensure banks behave safely.

- Complements Pillar 1 and Pillar 2.

- Disclosures: Banks must disclose key information (Capital, Risk Exposures, NPAs) to the public.

- Frequency: At least quarterly or half-yearly.

- Impact: Helps depositors and investors make informed decisions, forcing banks to stay healthy to attract funds.

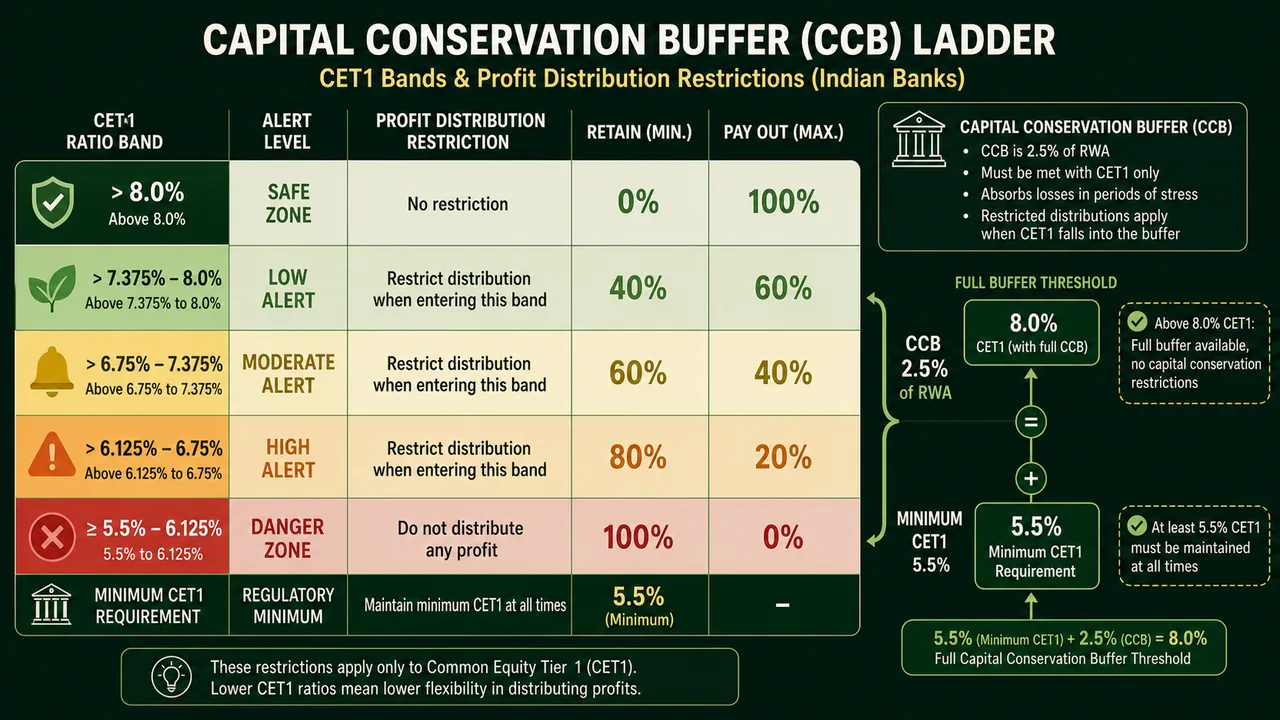

Capital Conservation Buffer (CCB)

Analogy: Think of CCB as a "Rainy Day Fund" or an extra savings account.

- Normal Capital: Is like your monthly expenses – you need it just to survive.

- CCB: Is like your emergency savings. You build it up when times are good, and dip into it when times are bad.

1. The Core Concept

- Objective: To ensure banks build up extra capital during "good times" so they can absorb losses during "bad times" without failing.

- Requirement: An additional 2.5% of RWA (over and above the minimum capital).

- Composition: Must be met ONLY with Common Equity Tier 1 (CET1) (the highest quality capital).

2. How it Works (The "Penalty" Zone)

If a bank maintains the full buffer (CET1 > 8.0%), it can freely pay dividends to shareholders and bonuses to staff.

BUT, if the bank faces losses and dips into this buffer (CET1 falls below 8.0%), RBI imposes restrictions on distributing profits. The closer the capital gets to the minimum, the stricter the restriction.

Dividend Restriction Table

When CET1 ratio falls into the buffer zone, the bank must RETAIN a portion of its profits instead of paying them out.

| CET1 Ratio Range (Buffer Zone) | Status | Minimum Retention Requirement | Max Dividend Allowed |

|---|---|---|---|

| 5.5% - 6.125% | 🚨 Danger Zone (Severe) | 100% | 0% |

| > 6.125% - 6.75% | ⚠️ High Alert | 80% | 20% |

| > 6.75% - 7.375% | 🔸 Moderate Alert | 60% | 40% |

| > 7.375% - 8.0% | 🔹 Low Alert | 40% | 60% |

| > 8.0% | ✅ Safe Zone | 0% | 100% |

Key Rule: The moment a bank touches the buffer, it cannot pay full dividends. This forces the bank to "conserve" capital to get back to safety.

Counter-cyclical Capital Buffer (CCCB)

- Objective: To protect the banking sector from periods of excess aggregate credit growth (bubbles) that have often been associated with the build-up of system-wide risk.

- Range: 0% to 2.5% of RWA.

- Current Status: Currently 0% in India. RBI decides when to activate it based on credit-to-GDP gaps.

- Activation: RBI gives a lead time of 4 quarters before it comes into effect.

Practice Questions

**Q1: Calculation of RWA for Off-Balance Sheet Item**

A bank has issued a financial guarantee of ₹100 crore for a corporate client (Risk Weight 100%). What is the RWA?

Answer:

- CCF for Financial Guarantee: 100%

- Credit Equivalent: ₹100 cr × 100% = ₹100 cr

- RWA: ₹100 cr (Credit Eq) × 100% (Risk Weight) = ₹100 crore

**Q2: Capital Charge to RWA Conversion**

A bank's Operational Risk capital charge is ₹900 crore. What is the equivalent RWA?

Answer:

- RWA = Capital Charge / 9%

- RWA = 900 / 0.09 = ₹10,000 crore

**Q3: Function of Pillar 2**

What is the main purpose of the Supervisory Review Process (Pillar 2)?

Answer: It allows the regulator (RBI) to evaluate the bank's internal capital adequacy assessment (ICAAP) and require the bank to hold additional capital for risks not fully captured under Pillar 1 (like concentration risk or reputational risk).

Summary Cheat Sheet

| Concept | Key Details | Formula / Value |

|---|---|---|

| RWA Logic | Assets weighted by risk (Govt=0%, Unsecured=100%). | |

| Off-Balance Sheet | Guarantees/LCs converted to "Credit Equivalent". | |

| Operational Risk | Income-based capital (BIA approach). | |

| CAR (Total) | Cap Adequacy Ratio (Tier 1 + 2). | |

| Pillar 2 (SREP) | Supervisory review of internal capital assessment (ICAAP). | - |

| Buffer (CCB) | "Rainy day fund". Common Equity Only. | 2.5% of RWA |

| Dividend Limit | Restrictions apply if CET1 dips into buffer. | 100% stop if |

References

- Master Circular on Basel III Capital Regulations – RBI (2023)

- BCBS Framework for RWA and Capital Buffers

Lesson Doubts

Ask questions, get expert answers