🏦 Capital Adequacy — Basel Framework & Capital Requirements

Complete guide to Capital Adequacy — Basel I, II & III framework, three pillars, capital components (CET1, AT1, Tier 2), credit/market/operational risk, D-SIBs, IRB approach, expected loss, and SREP/ICAAP for banking exams.

Introduction

In 1974, Governors of G10 central banks established the Basel Committee on Banking Supervision (BCBS) due to global financial turbulences, triggered by events like the fall of Herstatt Bank.

- The purpose was to enhance financial stability through improved banking supervision globally and foster cooperation among member countries.

- The Committee aimed to prevent the decline of capital standards in banking systems and promote consistency in measuring capital adequacy.

Evolution of Basel Norms

- The Basel Accord, introduced in 1988, advocated for a minimum capital ratio of 8% by the end of 1992, with India adopting these norms in April 1992.

- To align with BCBS guidelines on capital adequacy, the Reserve Bank of India introduced a risk-based capital ratio system effective from April 1992, requiring banks to maintain minimum capital funds relative to risk-weighted assets.

- This system encompassed both balance sheet assets and off-balance sheet exposures, assigning prescribed risk weights to each category.

- In June 2004, RBI issued guidelines for banks to maintain capital charge for market risks, following the BCBS's 1996 amendment to incorporate market risks into the Capital Accord.

Capital

The capital adequacy framework ensures banks have enough capital to absorb potential losses from unexpected events.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Introduction

In 1974, Governors of G10 central banks established the Basel Committee on Banking Supervision (BCBS) due to global financial turbulences, triggered by events like the fall of Herstatt Bank.

- The purpose was to enhance financial stability through improved banking supervision globally and foster cooperation among member countries.

- The Committee aimed to prevent the decline of capital standards in banking systems and promote consistency in measuring capital adequacy.

Evolution of Basel Norms

- The Basel Accord, introduced in 1988, advocated for a minimum capital ratio of 8% by the end of 1992, with India adopting these norms in April 1992.

- To align with BCBS guidelines on capital adequacy, the Reserve Bank of India introduced a risk-based capital ratio system effective from April 1992, requiring banks to maintain minimum capital funds relative to risk-weighted assets.

- This system encompassed both balance sheet assets and off-balance sheet exposures, assigning prescribed risk weights to each category.

- In June 2004, RBI issued guidelines for banks to maintain capital charge for market risks, following the BCBS's 1996 amendment to incorporate market risks into the Capital Accord.

Capital

The capital adequacy framework ensures banks have enough capital to absorb potential losses from unexpected events.

- Capital is categorised into Tier 1 and Tier 2, reflecting the quality of instruments.

- Tier 1 capital consists mainly of share capital and disclosed reserves, offering the highest loss absorption capacity.

- Tier 2 capital includes specific reserves and subordinated debt, with lower loss absorption capacity compared to Tier 1.

Capital Components Summary

| Common Equity Tier 1 (CET 1) | Additional Tier 1 (AT 1) |

|---|---|

| Paid-up equity capital | Perpetual non-cumulative preference shares (PNCPS) |

| Retained earnings | Stock surplus from PNCPS issuance |

| Revaluation reserves from consolidation performance | Debt capital instruments |

| Capital reserves representing surplus from sale | Any other instrument notified by RBI |

| Balance in P&L account at end of previous FY | |

| Reserve in P&L account at end of previous FY |

Domestic Systemically Important Banks (D-SIBs)

- RBI introduced the Framework for Domestically Systemically Important Banks (D-SIBs) in July 2014.

- D-SIB framework mandates disclosure of D-SIB names annually starting from 2015.

- Additional common equity requirements are applied based on the bucket parameters.

- Foreign banks operating in India designated as Global Systemically Important Banks (G-SIBs) must maintain additional CET1 capital surcharge in India.

- The surcharge is proportional to their Risk Weighted Assets (RWAs) in India relative to their global RWAs.

- Systemically important banks provide assistance to businesses in need with difficulty, increasing credit risk.

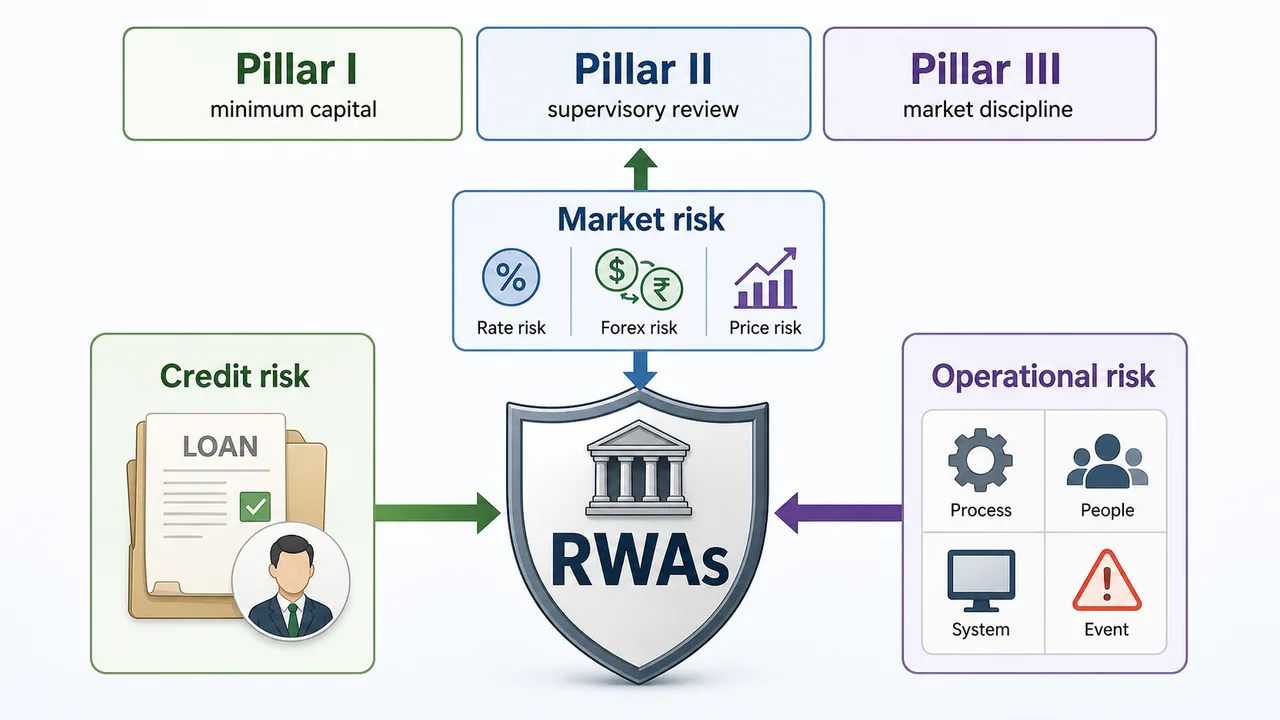

Credit Risk

- Credit risk refers to potential losses a bank may face due to a borrower's failure to meet financial obligations.

- It includes the risk of reduced value of a bank's assets or actual losses from defaulting borrowers.

- Credit risk is a primary concern for banks and is often the largest source of risk in banking operations.

- Effective credit risk management involves assessing and mitigating the risk of non-repayment of loans.

- Major banks allocate over 60% of their risk-weighted assets to credit risk.

Market Risk

- Market risk refers to potential losses a bank may face due to fluctuations in market-driven factors.

- It includes changes in interest rates, exchange rates, stock prices, and commodity prices.

- The Bank for International Settlements (BIS) defines market risk as adverse effects on the value of on or off balance sheet positions.

- Market risk affects the earnings and capital of banks.

Operational Risk

- Operational risk is related to people and structure as a key aspect of their risk management system.

- Operational risk encompasses risks arising from inadequate or failed internal processes, people, and systems.

- A breakdown of operations can result in misrepresentation of an institution's financial position and significant losses.

- Management of operational risk involves identifying, assessing, monitoring, and controlling/mitigating this risk.

- It involves risks such as legal risks and compliance risks.

- Operational risk management encompasses the bank's internal processes, people, systems, and external events.

- Capital requirements are calculated based on specific methodologies (BIA, Standardised, AMA).

- Primary objective of operational risk management: to prevent losses due to inadequate internal processes and external events.

Basel II Framework

- BCBS released the "International Convergence of Capital Measurement and Capital Standards: A Revised Framework — Comprehensive Version" document in June 2006.

- Basel II introduced capital charge for Operational Risk (OR) in addition to capital for Credit Risk and Market Risk.

Three Pillars of Basel II/III

| Pillar | Focus |

|---|---|

| Pillar I | Minimum Capital Requirements |

| Pillar II | Supervisory Review (SREP & ICAAP) |

| Pillar III | Market Discipline |

Basel III Implementation in India

- Reserve Bank issued guidelines on capital regulation based on Basel III reforms on May 2, 2012.

- Implementation of Basel III capital regulation began in India from April 1, 2013, in phases.

- Full implementation was achieved by March 31, 2019, with some exceptions.

- Basel III regulations maintain the same three pillars as Basel II: minimum capital requirements, supervisory review of capital adequacy, and market discipline.

Pillar I: Minimum Capital Requirements

- Reserve Bank of India issued guidelines on capital adequacy.

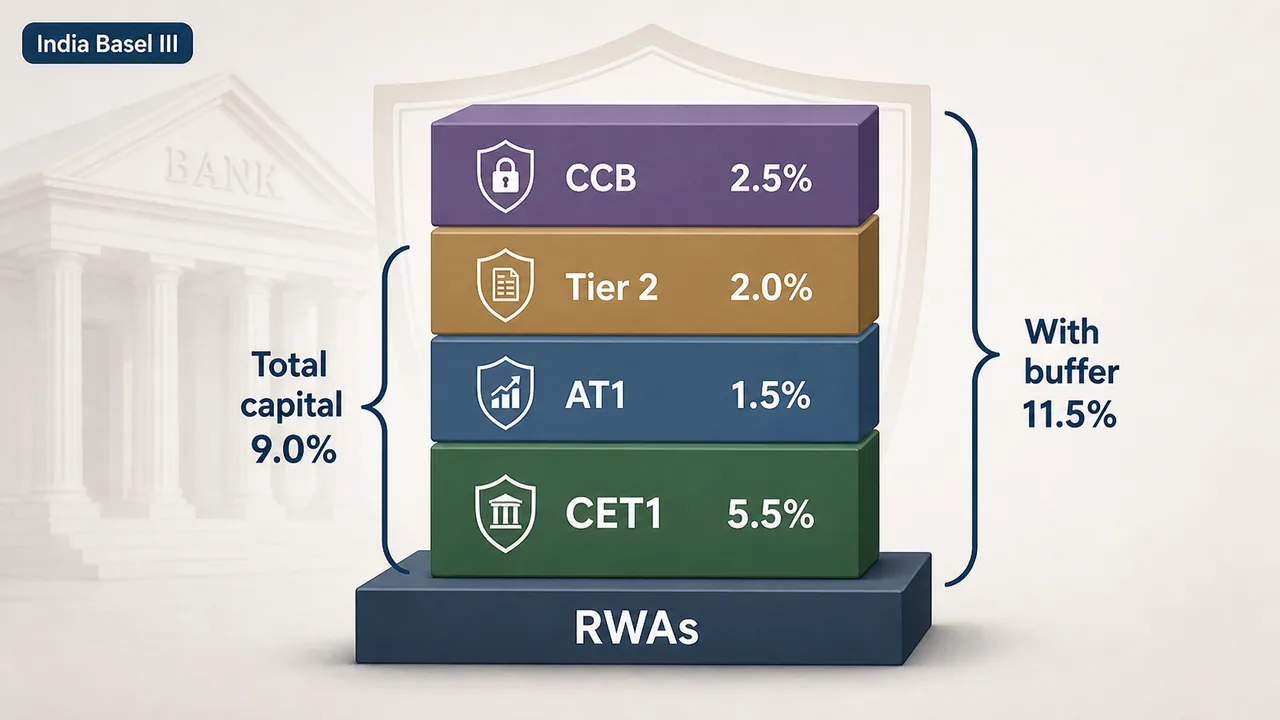

- Banks are required to maintain a minimum Pillar 1 Capital to Risk-weighted Assets Ratio (CRAR) of 9%.

- The CRAR excludes capital conservation buffer and countercyclical capital buffer.

- RBI considers relevant risk factors and internal capital adequacy assessments of each bank.

- Capital held by a bank should align with its overall risk profile.

- Effectiveness of the bank's risk management systems is evaluated for identifying, assessing, and monitoring risks.

- Reserve Bank evaluates banks' risk management systems for various risks, including credit risk in the banking book, liquidity risk, concentration risk, and residual risk.

- Higher minimum capital ratios may be prescribed for banks under the Basel II framework based on their risk profiles.

Components of Capital

| Total regulatory capital consists of | Tier 1 Capital (going-concern capital) + Tier 2 Capital (gone-concern capital) |

| Tier 1 Capital | Common Equity Tier 1 + Additional Tier 1 |

Regulatory Capital Requirements (As % of RWAs)

| Regulatory Capital Component | As % of RWAs |

|---|---|

| Minimum Common Equity Tier 1 Ratio | 5.5 |

| Capital Conservation Buffer | 2.5 |

| Minimum CET 1 Ratio + CCB | 8.0 |

| Additional Tier 1 Capital | 1.5 |

| Minimum Tier 1 Capital Ratio | 7.0 |

| Tier 2 Capital | 2.0 |

| Minimum Total Capital Ratio (MTC) | 9.0 |

| MTC + Capital Conservation Buffer | 11.5 |

Limits and Minimum Total Capital

- Common Equity Tier 1 (CET 1) capital should be at least 5.5% of RWAs.

- Tier 1 capital should be at least 7% of RWAs, with Additional Tier 1 capital capped at 1.5% of RWAs.

- Total Capital (Tier 1 Capital plus Tier 2 Capital) should be at least 9% of RWAs, with Tier 2 capital capped at 2%.

Quick Note on Excess Capital

- Excess Additional Tier 1 capital can be used to meet the requirement of 4.5% or 5% of RWAs if the bank complies with minimum CET 1 and Tier 1 capital ratios.

- Banks must also maintain a Capital Conservation Buffer (CCB) in addition to the minimum CET 1 capital requirement of 2.5% of RWAs.

Common Equity Tier 1 Capital — Indian Banks

Elements of CET 1 Capital

- Common shares (paid-up equity capital) that meet classification criteria

- Stock surplus (share premium) from common shares issuance

- Retained earnings

- Common shares issued and held by consolidated subsidiaries of the bank (if minorities don't exceed 20%)

- Common shares from consolidated subsidiaries held by third parties (minority interest)

- Balance in Profit & Loss Account from the previous financial year and any balance in the current period's P&L account after provision for bonus, dividend, and tax

- Foreign currency translation reserve from the translation of financial statements of foreign operations (where not in India, only under specific conditions)

- Negative adjustments/deductions applied in the calculation of Common Equity Tier 1 capital (where CET1 related to accumulated losses and other gains and losses)

These adjustments are subtracted from the sum of items (i) to (x) in the calculation process.

Elements of CET 1 Capital — Foreign Banks' Branches

- Interest-free funds from Head Office kept in a separate account for meeting capital and reserve requirements.

- Statutory reserves held in Indian books.

- Remittable surplus retained in Indian books, non-repatriable as long as the bank functions in India.

- Interest-free funds remitted from abroad for property acquisition, held in a separate account (non-repatriable).

- Capital reserve from asset sale in India, held in a separate account, non-repatriable.

- Foreign currency translation reserve from foreign operations' financial statements.

- Deductions for regulatory adjustments and Common Tier Assets (DTAs) associated with accumulated losses, subtracted from the total above.

Additional Tier 1 Capital

Elements — Indian Banks

- Perpetual Non-Cumulative Preference Shares (PNCPS) meeting regulatory requirements.

- Stock surplus (share premium) from issued instruments in Additional Tier 1 capital.

- Debt capital instruments meeting regulatory requirements for Additional Tier 1 capital inclusion.

- Any other instrument notified by the Reserve Bank for Additional Tier 1 capital inclusion.

- Tier 1 capital instruments issued by consolidated subsidiaries and held by third parties, meeting inclusion criteria.

- Deductions for regulatory adjustments applied in Additional Tier 1 capital calculation.

Elements — Foreign Banks' Branches

- Head Office borrowings in foreign currency by foreign banks operating in India meeting regulatory requirements for Additional Tier 1 capital inclusion.

- Any other item permitted by the Reserve Bank for Additional Tier 1 Capital.

- Deductions for regulatory adjustments applied in Additional Tier 1 capital calculation.

Tier 2 Capital

Under Basel III, there will be a single set of criteria governing all Tier 2 debt capital instruments.

Elements — Indian Banks

- General Provisions and Loss Reserves

- Debt Capital instruments issued by banks

- Preference Share Capital Instruments (PCPS/RNCPS/RCPS)

- Stock surplus (share premium) from issued instruments in Tier 2 capital

- Tier 2 capital instruments issued by consolidated subsidiaries meeting criteria for inclusion

- Revaluation reserves (if not considered as CET 1) at a discount of 55%

- Other instruments notified by the Reserve Bank for Tier 2 capital inclusion

- Regulatory adjustments/deductions applied in Tier 2 capital calculation

Elements — Foreign Banks' Branches

- General Provisions and Loss Reserves

- Head Office (HO) borrowings in foreign currency for Tier 2 debt capital

- Revaluation reserves (if not considered as CET 1) at a discount of 55%

- Regulatory adjustments/deductions applied in Tier 2 capital calculation

Minority Interest

- Minority interest in non-bank subsidiaries excluded from regulatory capital.

- Total capital instruments from fully consolidated subsidiaries not meeting Tier 1 or Tier 2 criteria excluded from regulatory capital.

Regulatory Adjustments/Deductions

- Goodwill and intangible assets

- Deferred tax assets (DTAs)

- Cash flow hedge reserve

- Shortfall of provisions to expected losses

- Gain-on-sale related to securitisation transactions

- Cumulative gains and losses from changes in own credit risk on fair valued financial liabilities

- Defined benefit pension fund assets and liabilities

- Investments in own shares (treasury stock)

- Investments in the capital of banking, financial, and insurance entities

Pillar II: Supervisory Review and Evaluation Process (SREP) and Internal Capital Adequacy Assessment Process (ICAAP)

- SREP ensures banks have enough capital to cover their risks and encourages better risk management.

- Banks need a clear Internal Assessment Process to show RBI they have enough capital for their risks.

- The ICAAP document should include capital adequacy assessment and future capital requirement estimates.

- Annual ICAAP review is a regulatory requirement, and the Board-approved ICAAP should be submitted to RBI by June 30 each year.

Pillar III: Market Discipline

- Banks must have a board-approved disclosure policy outlining what information they will disclose.

- Disclosures should cover the scope of application, capital, risk exposures, risk assessment processes, and capital adequacy.

- These disclosures help market participants assess key information about the bank's operations and financial health.

Calculation of Minimum Capital Requirement

| For credit risk, options | For operational risk | For market risk |

|---|---|---|

| Standardised Approach | Basic Indicator Approach (BIA) | Standardised Duration Approach |

| Foundation IRB Approach | Standardised Approach | |

| Advanced IRB Approach | Advanced Measurement Approach (AMA) |

Capital for Credit Risks

Standardised Approach (SA)

- Risk-weighted assets in the Standardised Approach are calculated by multiplying exposures with prescribed risk weights based on external credit ratings or fixed categories.

- Banks may apply reduced risk weights where specific conditions (such as insurance or sovereign guarantees on external credit enhancements) are met.

- Ratings assigned by eligible external credit rating agencies support the measure of credit risk.

- RBI has identified external credit rating agencies meeting eligibility criteria.

- Banks may rely on ratings assigned by these agencies for assigning risk weights for capital adequacy purposes.

- Banks can use lower risk weights for unrated exposures based on ratings available for specific sovereign or central bank claims.

- Conditions include parity or seniority to specific rated debt and matching maturities.

- ECAIs must disclose banks and corresponding credit facilities rated by them.

- RBI circular dated October 10, 2022, reiterates that loan ratings lacking disclosure by ECAIs are ineligible for capital computation.

- Such exposures are treated as unrated, and applicable risk weights are assigned as per the Master Circular on Basel III capital regulations dated April 1, 2022.

Claims Included in the Regulatory Retail Portfolio

- Claims treated as a retail claim carry a risk weight of 75% except for non-performing assets.

- Excluded from regulatory retail portfolios.

Qualifying Criteria for Regulatory Retail

- Product Criterion: Exposure to individual or small business and turnover < INR 5 crore.

- Orientation Criterion: Exposures to individuals, small businesses, trusts, private and public limited companies, and so on.

- Granularity Criterion: Aggregate exposure not exceeding 0.2% of overall portfolio. Maximum turnover for small businesses is INR 50 crore.

- Low Value of Individual Exposures: Maximum aggregated retail exposure to one counterpart should not exceed ₹7.5 crore.

Internal Ratings Based (IRB) Approach

Foundation IRB Approach

- Uses bank's own estimates of PD (Probability of Default)

- LGD and EAD provided by supervisor

- DPR Approved: Further details TBA

Advanced IRB Approach

- Uses bank's own estimates for PD, LGD, and EAD

- IRB Approach allows banks (subject to RBI approval) to use internal estimates for key risk components

Key IRB Concepts

- IRB Approach calculates capital requirement based on unexpected losses (UL) and expected losses (EL).

- Risk-weighted asset amounts derived from IRB functions are multiplied by a factor of 1.06.

- Total risk-weighted asset amount is determined by summing risk-weighted amounts for UL for all IRB asset classes.

- Banks categorise banking book exposures into six broad asset classes: Corporate, Sovereign, Bank, Retail, Equity, and Others.

Calculation of Expected Loss

- Advanced IRB approach allows banks to use internal instruments for key drivers of credit risk — in capital calculation.

- Expected Loss (EL) = PD × LGD × EAD

- EAD is calculated using Credit Conversion Factors (drawn amounts + future drawdowns)

- LGD represents the percentage of EAD bank might lose if borrower defaults; LGD = 1 − Recovery Rate

- EL is calculated as 1 minus the recovery rate.

- Risk measures are fundamental to both risk management and regulatory capital.

- Expected Loss (EL) for credit risk is calculated as EL = PD × EAD × LGD

- Parameters describe bank's exposure to its own credit risk for a particular borrower.

Transverse Dimension

- Transverse Dimension: Shocks impacting one institution can spread rapidly to others, causing systemic threats.

- Common exposures like joint lending and herd lending are breeding grounds for such shocks.

- Analysis of system-wide PDs can indicate vulnerabilities and concentration of risk in certain sectors, serving as a tool for supervisory analysis.

- Risk concentration may reveal common vulnerability but may not reveal interconnectedness of risk across lenders.

- Analysis of system-wide PDs can be approached in two ways: assessing individual borrower risk associated with individual borrower behaviour and considering independent institutions or individual portfolios.

Longitudinal Dimension

- Longitudinal Dimension: Systemic risk's procyclical nature relates to how collective risk evolves over time in sync with the economic cycle.

- System-wide PDs are correlated with aggregate economic variables to assess systemic risk over time.

- Basel II proposed capital requirement assessment based on Expected Loss calculation adjusted for uniform characteristics over a one-year horizon.

- System-wide PD estimates serve as benchmarks for validating Internal Rating Based models.

- Analysis of longitudinal models reveals system-wide risk dependencies and vulnerabilities.

- Individual bank risk pricing practices can be compared with expected loss estimations for risk-return analyses across banks and within portfolios.

- Price differentiation across banks is evident based on the risk profile of the population.

Quick Notes for Exam

- BCBS was established in 1974 by Governors of G10 central banks to enhance financial stability through improved banking supervision.

- Purpose of Basel III: to enhance financial stability through improved banking supervision — NOT to decrease capital requirements or encourage risky lending.

- Two categories of capital: Tier 1 and Tier 2 — NOT Core Capital and Supplementary Capital (old terminology), NOT Tier A and Tier B.

- Primary objective of operational risk management: to prevent losses due to inadequate internal processes and external events.

- Three pillars of Basel II/III: Minimum Capital Requirements, Supervisory Review, Market Discipline — NOT Credit Risk/Market Risk/Operational Risk.

- Capital Conservation is NOT a component of Basel III framework (it's a buffer, not a pillar).

- Expected Loss (EL) = PD × LGD × EAD — this is the formula for credit risk.

- Primary purpose of Basel III capital regulations: to enhance the resilience of banks and promote financial stability.

- Market Risk is defined as potential losses due to fluctuations in market-driven factors — interest rates, exchange rates, stock prices.

- D-SIBs framework: to provide additional capital requirements for systemically important banks.

- Element of CET 1 Capital for Indian Banks: Goodwill and intangible assets — these are actually deductions, NOT elements. Stock surplus from Tier 2 instruments is NOT CET1.

- Additional Tier 1 Capital includes: Preference Share Capital Instruments (PNCPS) — NOT investments in own shares or revaluation reserves.

- Orientation Criterion determines the orientation of exposures for qualifying under Standardised Approach for credit risk.

- Granularity Criterion aims to ensure: aggregate exposure not exceeding 0.2% of overall portfolio. Maximum turnover ₹50 crore for small businesses.

- Maximum aggregated retail exposure under Low Value criterion: ₹7.5 crore.

- RORAC differs from RAROC: RORAC adjusts rate of return for risk, while RAROC adjusts capital for risk.

- RARORAC measures productivity in value creation relative to risk.

- RAROC model purpose: to measure profitability of a product or portfolio adjusted for credit risk.

- RAROC formula (Saunders & Allen): Spread + Fees − Operating Costs / Duration × Risk Amount.

- RAROC differs from RORAC: RAROC adjusts capital for risk, while RORAC adjusts returns for risk.

- Factors in RAROC application: future business potential and portfolio exposure.

- Loan guaranteed by State Government attracts 20% risk weight (NOT 0%).

Cheat Sheet

| # | Topic | Key Point |

|---|---|---|

| 1 | BCBS Established | 1974 by G10 central bank Governors |

| 2 | Trigger | Fall of Herstatt Bank, global financial turbulence |

| 3 | Basel Accord | 1988, minimum capital ratio 8% |

| 4 | India Adoption | April 1992 |

| 5 | Basel II Document | June 2006 |

| 6 | Basel II Addition | Operational Risk charge added |

| 7 | Three Pillars | Min Capital Requirements, Supervisory Review, Market Discipline |

| 8 | Basel III Guidelines | May 2, 2012 by RBI |

| 9 | Basel III India Start | April 1, 2013 (in phases) |

| 10 | Full Implementation | March 31, 2019 |

| 11 | Capital Tiers | Tier 1 (going-concern) + Tier 2 (gone-concern) |

| 12 | Tier 1 Components | CET 1 + Additional Tier 1 |

| 13 | Min CET 1 | 5.5% of RWAs |

| 14 | CCB | 2.5% of RWAs |

| 15 | CET 1 + CCB | 8.0% |

| 16 | Additional Tier 1 | 1.5% of RWAs |

| 17 | Min Tier 1 | 7.0% of RWAs |

| 18 | Tier 2 Capital | 2.0% of RWAs |

| 19 | Min Total Capital (MTC) | 9.0% of RWAs |

| 20 | MTC + CCB | 11.5% |

| 21 | D-SIBs Framework | July 2014 |

| 22 | D-SIB Disclosure | Annual from 2015 |

| 23 | Credit Risk | Largest source of risk, >60% of RWA |

| 24 | Market Risk | Interest rates, FX, stocks, commodities |

| 25 | Operational Risk | Internal processes, people, systems, external events |

| 26 | Credit Risk Approaches | Standardised, Foundation IRB, Advanced IRB |

| 27 | Op Risk Approaches | BIA, Standardised, AMA |

| 28 | Market Risk Approach | Standardised Duration Approach |

| 29 | Retail RW | 75% (Standardised Approach) |

| 30 | Product Criterion | Individual or small business, turnover < ₹5 Cr |

| 31 | Granularity | Aggregate exposure ≤ 0.2% of overall portfolio |

| 32 | Low Value Criterion | Max ₹7.5 crore per counterpart |

| 33 | Small Business Turnover | Max ₹50 crore |

| 34 | EL Formula | PD × LGD × EAD |

| 35 | LGD | 1 − Recovery Rate |

| 36 | IRB Multiplier | 1.06 factor on RWA |

| 37 | IRB Asset Classes | 6: Corporate, Sovereign, Bank, Retail, Equity, Others |

| 38 | Foundation IRB | Bank's PD; supervisor's LGD & EAD |

| 39 | Advanced IRB | Bank's own PD, LGD & EAD |

| 40 | CET 1 — Indian Banks | Paid-up equity, share premium, retained earnings, reserves |

| 41 | AT 1 — Indian Banks | PNCPS, stock surplus from PNCPS, debt capital instruments |

| 42 | Tier 2 — Indian Banks | General provisions, debt instruments, PCPS/RNCPS/RCPS |

| 43 | Revaluation Reserve Discount | 55% discount for Tier 2 inclusion |

| 44 | SREP | Supervisory Review and Evaluation Process |

| 45 | ICAAP Submission | Board-approved, to RBI by June 30 each year |

| 46 | Market Discipline | Board-approved disclosure policy |

| 47 | Transverse Dimension | Shocks spreading across institutions (systemic) |

| 48 | Longitudinal Dimension | Procyclical risk evolving with economic cycle |

| 49 | ECAI Disclosure | Oct 10, 2022 circular — ratings without disclosure ineligible |

| 50 | Minority Interest | Non-bank subsidiary interest excluded from regulatory capital |

Lesson Doubts

Ask questions, get expert answers