🛫 Farm Planning & Budgeting: Blueprint for Profitable Agriculture

Master farm planning types, budgeting techniques (enterprise, partial, complete, cash flow), and the systematic steps to build a profitable whole farm plan.

Starting Point: Why Do Farmers Need a Plan?

Imagine a wheat farmer in Punjab with 5 hectares of land, two family labourers, and Rs. 2 lakh in savings. Should he grow only wheat? Add mustard? Raise a buffalo? How much fertilizer should he buy? Without a plan, he relies on guesswork. With a plan, every rupee, every acre, and every working hour is directed toward maximum profit. That is the power of farm planning and budgeting.

Farm planning becomes easier when the student sees the farm as one connected system: land, labour, capital, enterprise choice, calendar, and expected returns all have to fit together before the season starts.

What is Farm Planning?

Farm planning is a programme of total farm activity drawn up in advance -- a blueprint that outlines what a farmer intends to do before actual operations begin.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Starting Point: Why Do Farmers Need a Plan?

Imagine a wheat farmer in Punjab with 5 hectares of land, two family labourers, and Rs. 2 lakh in savings. Should he grow only wheat? Add mustard? Raise a buffalo? How much fertilizer should he buy? Without a plan, he relies on guesswork. With a plan, every rupee, every acre, and every working hour is directed toward maximum profit. That is the power of farm planning and budgeting.

Farm planning becomes easier when the student sees the farm as one connected system: land, labour, capital, enterprise choice, calendar, and expected returns all have to fit together before the season starts.

What is Farm Planning?

Farm planning is a programme of total farm activity drawn up in advance -- a blueprint that outlines what a farmer intends to do before actual operations begin.

A good farm plan covers:

- Which crops to grow and which livestock to raise

- How much labour to hire and what equipment to use

- How much capital to invest and when to invest it

Farm planning enables the farmer to achieve objectives (profit maximization or cost minimization) in an organized manner. It ensures every resource -- land, labour, capital, and management skill -- is used to its fullest potential.

IMPORTANT

Farm planning is not a theoretical exercise. Studies show that farmers who plan systematically earn significantly more than those who rely solely on experience and tradition.

Types of Farm Plans

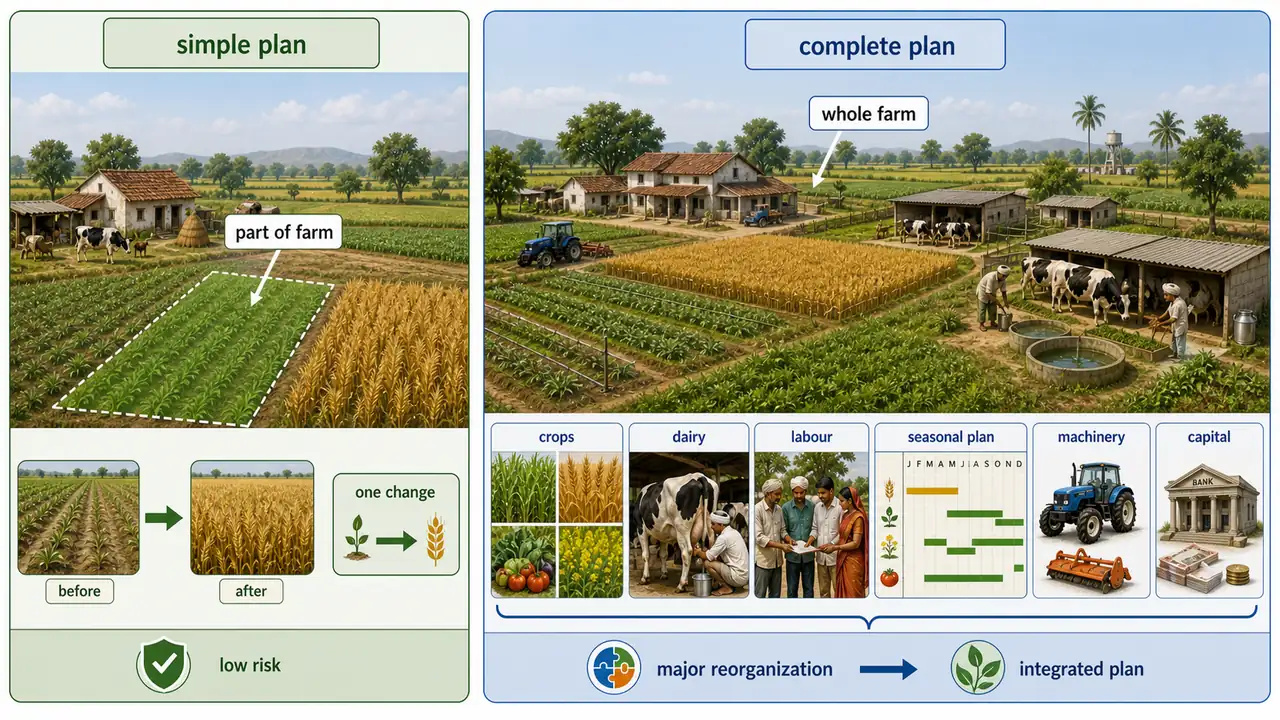

1. Simple Farm Plan

Adopted for a part of the land, one enterprise, or to substitute one resource for another.

Agricultural example: A groundnut farmer in Gujarat decides to replace manual weeding with herbicide application on 2 of his 8 acres. He tests the change on a small area first, observes the outcome, and then decides whether to extend it.

Simple plans are the starting point for change -- they minimize risk and build confidence before larger reorganizations.

2. Complete (Whole) Farm Plan

Planning for the entire farm as a single integrated unit. Every acre, every labour hour, and every rupee of capital is considered simultaneously.

Agricultural example: A farmer in Madhya Pradesh inherits additional land and wants to shift from purely crop-based farming to a mixed farming system (soybean + wheat rotation + dairy). A complete farm plan is needed to reorganize the entire operation.

| Feature | Simple Farm Plan | Complete Farm Plan |

|---|---|---|

| Scope | Part of farm or one enterprise | Entire farm |

| When used | Minor adjustments | Major reorganization |

| Complexity | Low | High |

| Risk | Minimal | Requires careful analysis |

| Example | Switching from manual to machine sowing | Adding dairy to a crop farm |

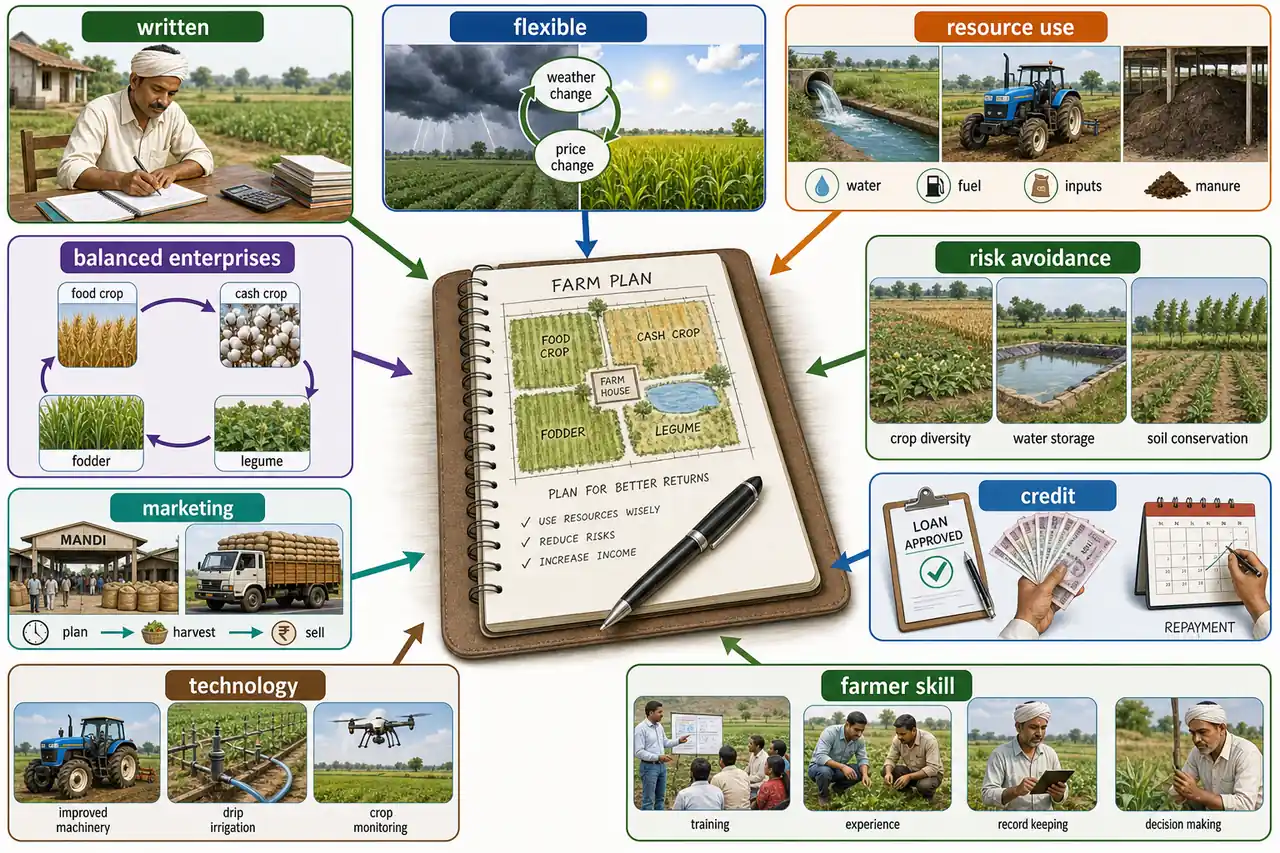

Characteristics of a Good Farm Plan

A good farm plan is not just a list of activities. It is a carefully balanced document:

- Written -- serves as a reference that can be reviewed and shared with lenders or extension workers.

- Flexible -- adaptable to changing weather, market prices, and new technology. Must include contingency provisions.

- Efficient resource use -- every unit of land, labour, and capital put to its most productive use.

- Balanced enterprise combination ensuring:

- Production of food, cash, and fodder crops

- Soil fertility maintenance through legume-based rotations

- Year-round employment of labour, power, and water

- Risk avoidance -- diversification so that failure in one enterprise does not ruin the whole farm.

- Farmer's knowledge -- matches the farmer's skills, experience, and preferences.

- Efficient marketing -- considers when and where to sell for best prices.

- Credit planning -- realistic borrowing, usage, and repayment strategy.

- Latest technology -- adopts proven, locally suitable modern techniques.

TIP

Exam mnemonic -- "WFEB-RMCL": Written, Flexible, Efficient resource use, Balanced enterprises, Risk avoidance, Marketing, Credit planning, Latest technology.

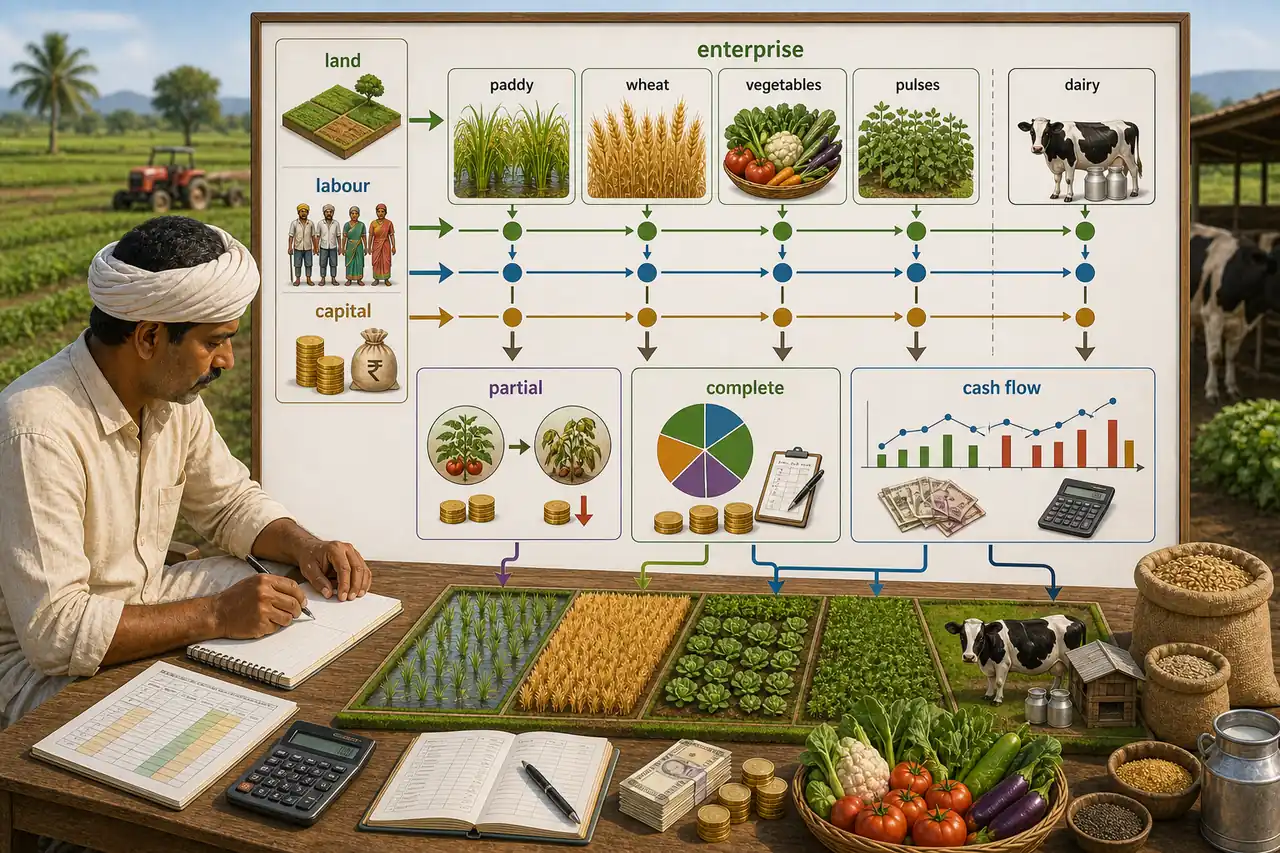

Farm Budgeting

While planning decides "what to do," budgeting determines "whether it will be profitable."

Farm budgeting is a method of estimating expected income, expenses, and profit for a farm business. It tests a new plan before implementation to be sure it will improve profit.

Planning and budgeting are complementary tools -- no plan is complete without a budget, and no budget is meaningful without an underlying plan.

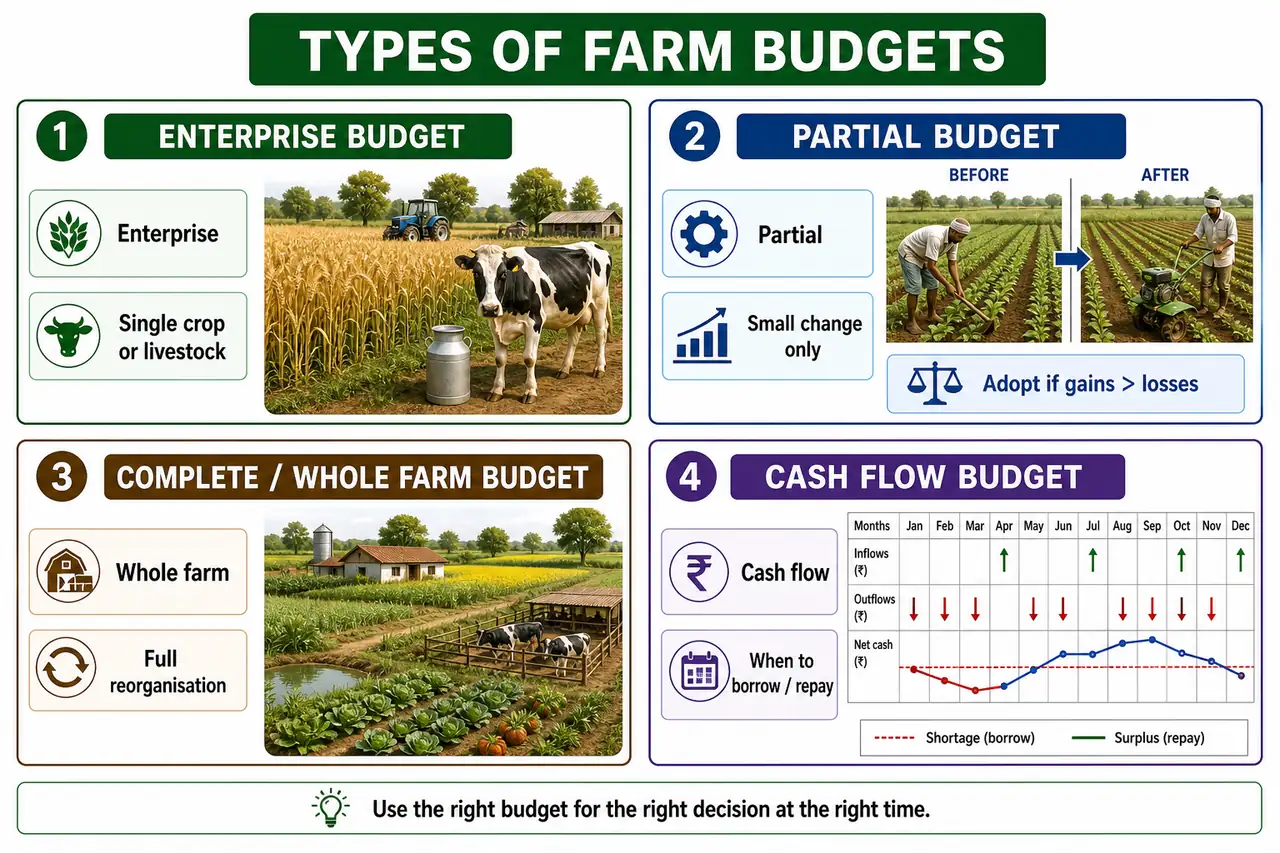

Types of Farm Budgets

1. Enterprise Budget

An enterprise budget estimates all income and expenses associated with a single crop or livestock commodity and its profitability.

- Developed per standard unit: one hectare for crops, one head for livestock

- Organized in three sections: income, variable costs, and fixed costs

- Allows direct comparison of competing enterprises

Agricultural example: Enterprise budget for paddy (1 hectare) vs. sugarcane (1 hectare) helps a farmer in Karnataka decide which crop to grow.

Steps to develop an enterprise budget:

- Estimate total production (average yield under normal conditions)

- Estimate expected output price (realistic average)

- Calculate variable costs (seed, fertilizer, labour, pesticides)

- Calculate fixed costs (depreciation, land rent, interest on fixed capital)

- Compute profit = Total Income - (Variable Costs + Fixed Costs)

2. Partial Budget

Used to calculate the expected change in profit for a proposed, relatively small change in the farm plan. Only marginal costs and marginal returns are estimated.

Three types of changes analyzed:

| Type of Change | Example | Question Answered |

|---|---|---|

| Enterprise substitution | Replacing groundnut with sunflower | Will switching crops increase profit? |

| Input substitution | Using tractor instead of bullock plough | Is the new input more cost-effective? |

| Scale change | Renting 2 additional acres for wheat | Is expansion financially worthwhile? |

Four components of a partial budget:

- Additional costs -- new inputs required (e.g., sunflower seeds, new pesticides)

- Reduced income -- income lost from the replaced enterprise (e.g., groundnut revenue forgone)

- Additional income -- income gained from the new enterprise (e.g., sunflower revenue)

- Reduced costs -- costs saved from the replaced enterprise (e.g., saved groundnut input costs)

IMPORTANT

Partial Budget Decision Rule: If (Additional Income + Reduced Costs) > (Additional Costs + Reduced Income), the proposed change is profitable and should be adopted. Otherwise, reject it.

3. Complete (Whole Farm) Budget

A cost-and-return analysis of the whole farm as a single unit. Both variable and fixed costs are included.

When needed:

- Before starting farming on a new farm

- Comparing alternative farm plans (e.g., crop-only vs. mixed farming)

- During drastic reorganization (new rotation, new production methods)

Agricultural example: A farmer in Haryana wants to compare Plan A (wheat-paddy rotation) with Plan B (wheat-potato rotation + dairy). A complete budget for each plan reveals which maximizes net farm income.

4. Cash Flow Budget

A summary of cash inflows and outflows over a given time period. Its primary purpose is to estimate future borrowing needs and loan repayment capacity.

Agricultural example: A kharif paddy farmer earns income only after harvest (November-December), but incurs expenses from June onward. A cash flow budget shows exactly when to borrow, how much, and when to repay.

TIP

Cash flow budgets are especially important for farmers taking seasonal crop loans (Kisan Credit Card). They help plan borrowing and repayment to avoid unnecessary interest charges.

Comparison of Budget Types

| Feature | Enterprise Budget | Partial Budget | Complete Budget | Cash Flow Budget |

|---|---|---|---|---|

| Scope | Single crop/livestock | One proposed change | Whole farm | Cash timing |

| Costs included | Variable + Fixed | Only marginal (variable) | Variable + Fixed | Cash inflows & outflows |

| Best used for | Comparing enterprise profitability | Small plan changes | Major reorganization | Planning borrowing & repayment |

| Complexity | Low | Low-Medium | High | Medium |

| Example | Profit from 1 ha paddy | Switching groundnut to sunflower | New farm setup | Monthly cash needs for kharif season |

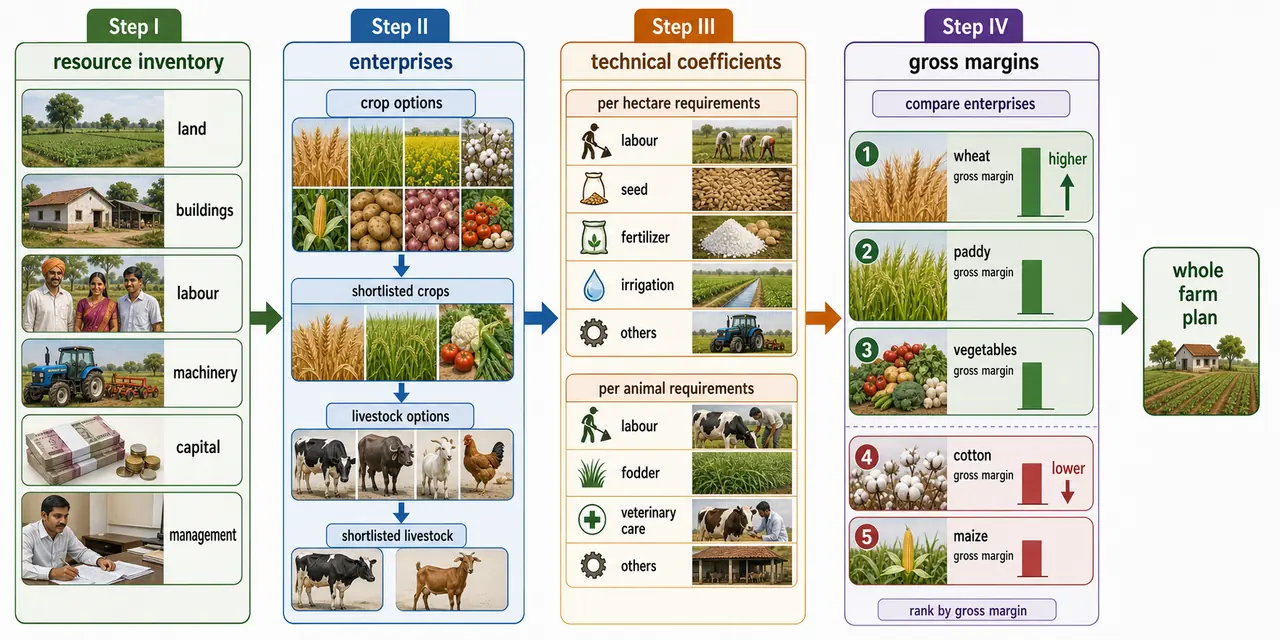

Steps in Farm Planning and Budgeting

The process follows a systematic sequence. Each step builds on the previous one.

Step I: Resource Inventory

A thorough inventory of available resources is the foundation of all farm planning. The type and quality of resources determine which enterprises are feasible.

| Resource | What to Assess | Agricultural Example |

|---|---|---|

| Land | Acres, soil type, fertility, irrigation, drainage, climate | Black cotton soil in Vidarbha suits cotton and soybean |

| Buildings | Size, capacity, potential uses | Cattle shed capacity limits dairy herd size |

| Labour | Quantity (man-days), quality (skills, experience) | Family with dairy experience favours livestock enterprise |

| Machinery | Number, size, capacity | Owning a combine harvester enables timely wheat harvest |

| Capital | Own funds + borrowing capacity | Rs. 5 lakh own + Rs. 3 lakh KCC loan = Rs. 8 lakh available |

| Management | Skills, training, strengths, weaknesses | Farmer trained in IPM can adopt low-pesticide cultivation |

TIP

Exam tip: Land is typically the most limiting resource and provides the starting point for planning. Remember the 6 resources: L-B-L-M-C-M (Land, Buildings, Labour, Machinery, Capital, Management).

Step II: Identifying Enterprises

Based on the resource inventory, list all feasible crop and livestock enterprises. Cast a wide net -- do not let custom or tradition restrict options.

Example: A farmer with irrigated black soil, dairy experience, and adequate capital might list: wheat, soybean, chickpea, cotton, onion, buffalo dairy, and poultry as feasible enterprises.

Step III: Estimating Technical Coefficients

Define each enterprise on a standard unit (one hectare for crops, one head for livestock) and estimate the resource requirements per unit.

Example: Paddy (1 ha) requires 80 man-days labour, 120 kg fertilizer, 5 irrigations. Wheat (1 ha) requires 40 man-days, 100 kg fertilizer, 4 irrigations. These coefficients determine the maximum size of each enterprise.

Step IV: Estimating Gross Margins

Gross margin = Total Income - Total Variable Costs (per unit of enterprise).

Gross margin does not include fixed costs, making it ideal for comparing enterprises since fixed costs remain constant regardless of enterprise choice.

Example:

| Enterprise (1 ha) | Yield | Price (Rs./q) | Gross Income | Variable Cost | Gross Margin |

|---|---|---|---|---|---|

| Paddy | 50 q | 2,300 | 1,15,000 | 55,000 | 60,000 |

| Wheat | 45 q | 2,275 | 1,02,375 | 42,000 | 60,375 |

| Soybean | 20 q | 4,600 | 92,000 | 30,000 | 62,000 |

NOTE

The enterprise with the highest gross margin per unit of the most limiting resource should be given priority.

Step V: Developing the Whole Farm Plan

Identify the most limiting resource and allocate it to enterprises with the greatest gross margin per unit of that resource.

Process:

- Start with land (usually the most limiting resource)

- Allocate land to the enterprise with the highest gross margin per hectare

- Check if another resource (e.g., labour, water) becomes more limiting

- Shift emphasis to gross margin per unit of the new limiting resource

- Continue until all resources are optimally allocated

The final plan represents the best possible use of all available resources given the farmer's objectives and constraints.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Farm Planning | Programme of total farm activity drawn up in advance; a blueprint before operations begin |

| Simple Farm Plan | For part of the farm or one enterprise; minor adjustments; low risk |

| Complete (Whole) Farm Plan | For the entire farm as a single integrated unit; major reorganization |

| Good Plan Traits | Written, flexible, efficient resource use, balanced enterprises, risk avoidance, marketing, credit planning, latest technology (WFEB-RMCL) |

| Farm Budgeting | Estimating expected income, expenses, and profit to test a plan before implementation |

| Enterprise Budget | Income and costs for a single crop/livestock on a standard unit (1 hectare for crops, 1 head for livestock) |

| Enterprise Budget Sections | Three sections: Income, Variable Costs, Fixed Costs |

| Partial Budget | Analyses a small change in the farm plan; only marginal costs and returns estimated |

| Partial Budget Rule | If (Additional Income + Reduced Costs) > (Additional Costs + Reduced Income), adopt the change |

| Partial Budget Changes | Enterprise substitution, input substitution, scale change |

| Complete Budget | Whole farm cost-and-return analysis; for new farms or drastic reorganization |

| Cash Flow Budget | Cash inflows and outflows over time; estimates borrowing needs and repayment capacity |

| Step I: Resource Inventory | Assess Land, Buildings, Labour, Machinery, Capital, Management (L-B-L-M-C-M) |

| Most Limiting Resource | Usually land; provides the starting point for planning |

| Step II: Identify Enterprises | List all feasible crop and livestock enterprises based on resource inventory |

| Step III: Technical Coefficients | Resource requirements per standard unit (1 ha or 1 head) for each enterprise |

| Step IV: Gross Margin | Total Income - Variable Costs per unit; excludes fixed costs; used to compare enterprises |

| Step V: Whole Farm Plan | Allocate most limiting resource to enterprise with highest gross margin per unit of that resource |

| Enterprise with Priority | Highest gross margin per unit of the most limiting resource |