🤝 FPO Input Supply & Agri Produce Aggregation — NABARD Financing Model

NABARD's financing model for Farmer Producer Organisation (FPO) input supply centres and agri produce aggregation hubs, covering working capital of ₹22.79 lakh, margin requirements, and SFAC credit guarantee. Critical for exams questions on FPO financing and agribusiness.

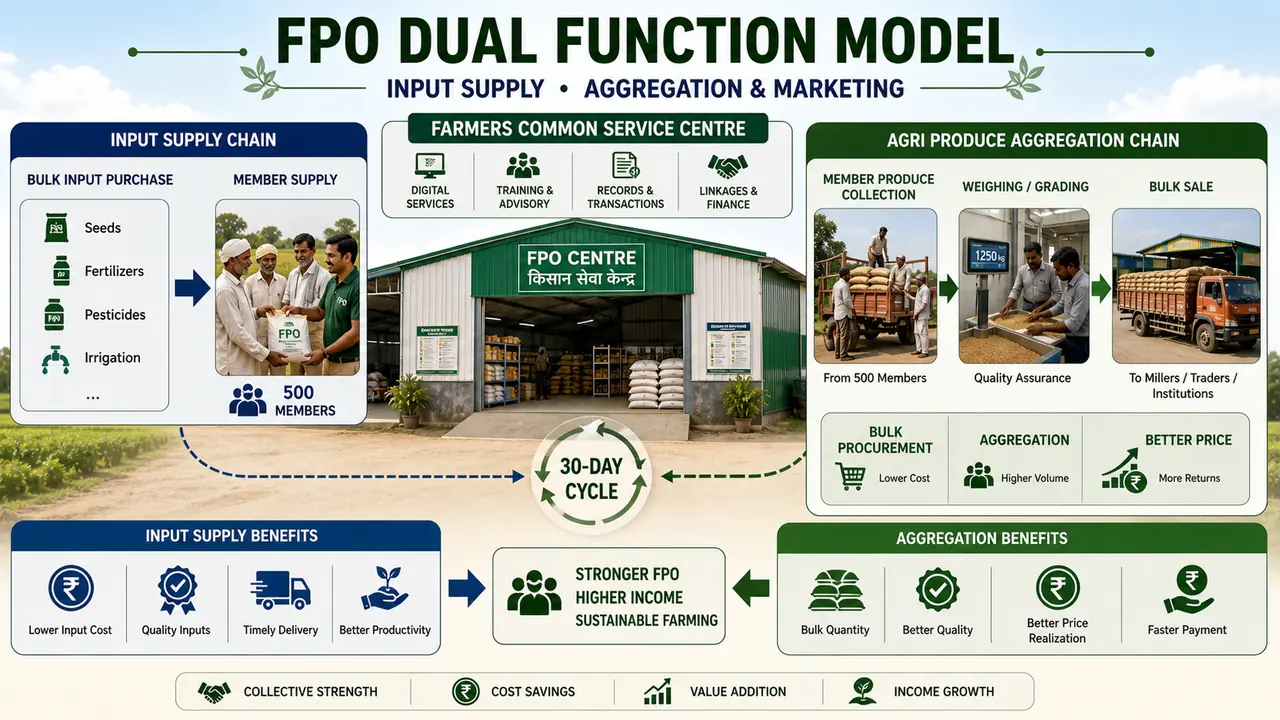

Small and marginal farmers — who own 85% of India's agricultural landholdings — are perpetually exploited at two ends: they overpay for inputs (seeds, fertilisers, pesticides) because they buy in small quantities from local dealers, and they underprice their produce because they sell individually without bargaining power. FPOs directly address both problems by aggregating both ends of the value chain.

- Agri Input Centre: Procures inputs in bulk from manufacturers/distributors → supplies to members at subsidised prices

- Aggregation Centre: Collects produce from members → sells in bulk to processors, exporters, or retail chains

- The two functions are combined in a Farmers Common Service Centre at FPO level

The Aggregation Logic — Why It Matters

When 500 farmers each sell 1 tonne of wheat individually, they face:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Small and marginal farmers — who own 85% of India's agricultural landholdings — are perpetually exploited at two ends: they overpay for inputs (seeds, fertilisers, pesticides) because they buy in small quantities from local dealers, and they underprice their produce because they sell individually without bargaining power. FPOs directly address both problems by aggregating both ends of the value chain.

- Agri Input Centre: Procures inputs in bulk from manufacturers/distributors → supplies to members at subsidised prices

- Aggregation Centre: Collects produce from members → sells in bulk to processors, exporters, or retail chains

- The two functions are combined in a Farmers Common Service Centre at FPO level

The Aggregation Logic — Why It Matters

When 500 farmers each sell 1 tonne of wheat individually, they face:

- High transport cost per unit

- No bargaining power at mandi

- Dependency on local arhatiyas (commission agents) charging 2–5%

- No access to direct buyers (processors, supermarkets, exporters)

When the same 500 farmers aggregate through an FPO:

- 500 tonnes offered as a single lot → attracts processors and retail chains directly

- Transport arranged in truckloads → lower per-unit cost

- Quality grading and standardisation → premium pricing

- Access to government procurement (NAFED, FCI) at MSP

NOTE

FPOs are required to have a minimum membership of 500 shareholders to be eligible for NABARD financing under this model. This is a standard MCQ threshold. The working capital model assumes only 350 of 500 members avail services in a given cycle — a conservative assumption.

Project Structure

The Agri Input and Aggregation Centre requires:

| Component | Details |

|---|---|

| Godown capacity | 250 MT (for input storage and produce aggregation) |

| Land | Provided by FPO (not included in project cost) |

| Roof shed | For weighing and temporary storage of farmer produce |

| Weighing equipment | Electronic weighbridge |

| Basic grading equipment | For quality standardisation |

| Location | Equidistant from 4–5 villages served |

Working Capital Requirement

Working capital is the lifeblood of this model — the FPO buys inputs on credit and sells to members within one month, then collects payment.

| Parameter | Value |

|---|---|

| Membership | 500 shareholders |

| Active members using services | 350 |

| Working capital cycle | 30 days |

| Working capital required | ₹22.79 lakh |

The ₹22.79 lakh covers:

- Input procurement (seeds, fertilisers, pesticides, farm equipment) for one month's supply to 350 members

- Buffer stock for price stability

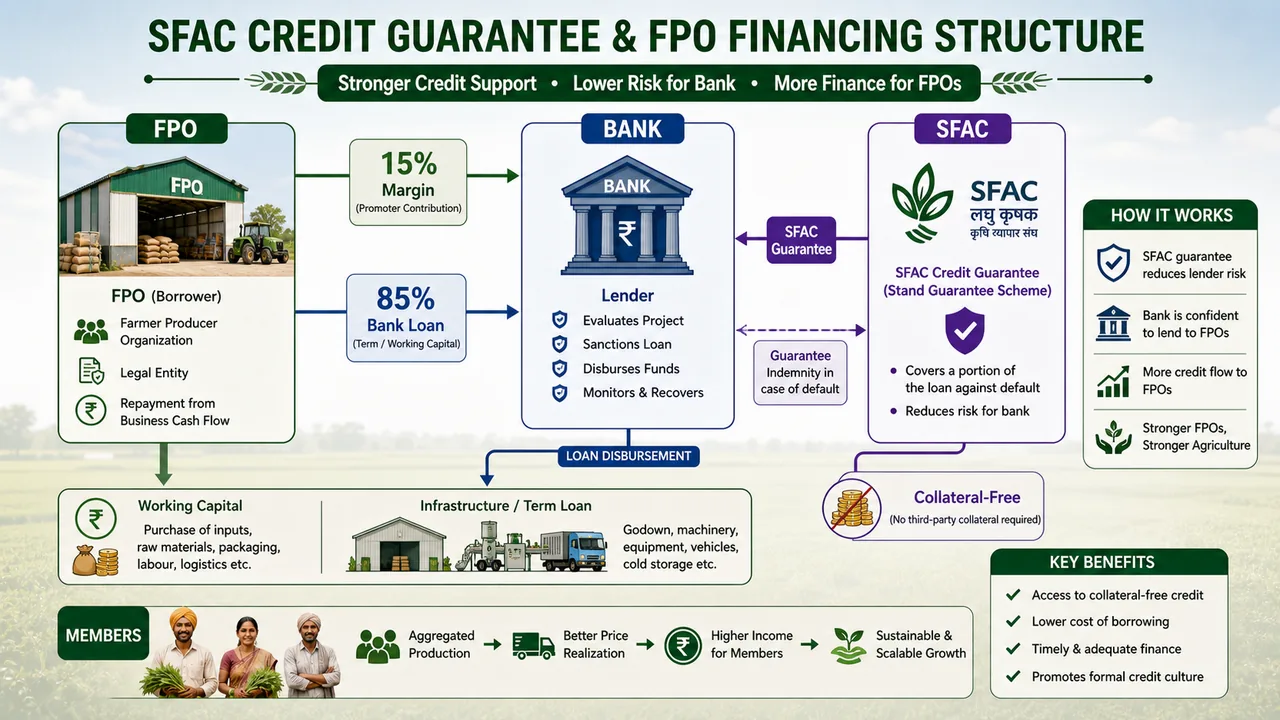

Means of Finance

| Parameter | Value |

|---|---|

| Margin money (FPO contribution) | 15% of project cost |

| Bank loan (working capital) | 85% |

| Interest rate | 11% (model rate; actual determined by bank) |

| Repayment cycle | Revolving credit (30-day cycle) |

NOTE

The margin for FPO financing models is 15% — lower than the 25% for individual food processing entrepreneurs. This reflects the collective nature of FPOs and the availability of credit guarantee cover from SFAC (Small Farmers Agribusiness Consortium) up to 85% of bank loan. With SFAC guarantee, banks can sanction without collateral security.

SFAC Credit Guarantee — Key Exam Fact

Small Farmers Agribusiness Consortium (SFAC) provides:

- Credit guarantee coverage of up to 85% of bank loan for FPOs

- This allows banks to sanction proposals without collateral security

- SFAC is under the Ministry of Agriculture & Farmers' Welfare

- NABARD also provides refinance to banks for FPO lending

NOTE

SFAC (not NCGTC, not CGTMSE) is the credit guarantee provider for FPO loans. CGTMSE covers MSME loans. SFAC covers agribusiness/FPO loans. This distinction is a direct MCQ trap.

Forward & Backward Linkages

The aggregation centre's viability depends on establishing:

Backward linkages (input side):

- Tie-ups with fertiliser companies (Iffco, Kribhco, RCF) for bulk supply at wholesale rates

- Seed companies for certified seed supply

- Pesticide dealers or direct company tie-ups

Forward linkages (produce side):

- Processors (dal mills, rice mills, oil mills)

- Retail chains (BigBasket, Reliance Fresh, DMart)

- Export houses (for commodities like onion, potato, soybean)

- Government procurement (NAFED, state agencies at MSP)

Farmer Interest Groups (FIGs) — The Building Block

FPO membership is organised through:

- FIGs (Farmer Interest Groups): 15–20 farmers at village level

- Multiple FIGs aggregate into the FPO

- Each FIG has a designated leader who coordinates with the FPO centre

This two-tier structure reduces coordination costs and improves last-mile service delivery.

Insurance & Other Requirements

- Crop insurance: FPO should ensure members are covered under PMFBY

- FPO insurance: The FPO entity itself should carry fire/theft insurance on godown

- Stock insurance: Input inventory and aggregated produce should be insured

- Licences: Fertiliser dealer licence, pesticide dealer licence, Mandi licence (state-specific)

NOTE

FPOs require multiple licences — fertiliser licence, pesticide licence, seed licence, and mandi licence — which are often difficult to obtain and are the most common barrier to FPO operations. This is a frequently tested operational challenge in FPO questions.

Sources & References

Primary source for this lesson is NABARD's official Model Bankable Projects portal.[1] Lesson-specific report copy used for this topic.[2]

References

2 sources • [1] [2]

References

Used for: Official NABARD portal for model bankable project documents and updates.

Used for: Reference copy used in this lesson for project parameters and worked figures.

The figures in this lesson reflect the cost norms and technical parameters as published in the NABARD document. Actual costs may vary by state, season, and year of implementation. Always refer to the latest NABARD circular for current norms.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| FPO definition | Farmer Producer Organisation — collective of small/marginal farmers for input procurement + produce aggregation |

| Problem addressed | Small/marginal farmers = 85% of India's landholdings; exploited on both input purchase and produce sale |

| Minimum membership | 500 shareholders for NABARD financing eligibility |

| Active members (model assumption) | 350 of 500 avail services in a given cycle |

| Godown capacity | 250 MT (input storage + produce aggregation) |

| Working capital cycle | 30 days (revolving) |

| Working capital required | ₹22.79 lakh |

| Margin Money | 15% of project cost (FPO contribution) |

| Bank Loan | 85% of working capital |

| Interest rate | 11% (model rate) |

| Credit guarantee | SFAC (Small Farmers Agribusiness Consortium) — covers up to 85% of bank loan |

| SFAC ministry | Ministry of Agriculture & Farmers' Welfare |

| SFAC vs CGTMSE | SFAC → FPO/agribusiness loans; CGTMSE → MSME loans (direct MCQ trap) |

| FIG structure | 15–20 farmers per FIG (Farmer Interest Group); multiple FIGs form FPO |

| Licences needed | Fertiliser licence + pesticide licence + seed licence + mandi licence |

| Backward linkages | Iffco/Kribhco (fertilisers), seed companies, pesticide dealers |

| Forward linkages | Dal/rice/oil mills, retail chains (BigBasket, Reliance Fresh), export houses, NAFED/state MSP procurement |

| Key MCQ fact | 15% margin (not 25%) — lower due to SFAC guarantee covering 85% of loan; no collateral needed |

Lesson Doubts

Ask questions, get expert answers