💰 FPO Working Capital & Term Loan — NABARD Illustrated Financing Models

NABARD's illustrated cash-flow based financing models for FPO working capital (₹33 lakh) and combined term loan (₹26.9 lakh) + working capital (₹53 lakh) covering appraisal methodology, DSCR, and bullet repayment structure. Key for exams credit appraisal questions.

FPO credit is fundamentally different from individual borrower credit. An FPO's creditworthiness cannot be assessed using a standard factory or farm appraisal — it depends on the collective business plan of 500+ diverse farmers operating in an unpredictable agricultural environment. NABARD's guidelines provide two illustrated models showing bankers exactly how to assess and structure FPO loans.

- Model 1 (Annexure I): Pure working capital assessment using cash flow method

- Model 2 (Annexure II): Combined term loan + working capital for capital-intensive FPO businesses

- Both models use ABC FPC Ltd. as the illustrative FPO name in NABARD's document

Why FPO Appraisal Is Unique

Banks must recognise several structural differences when appraising FPO credit:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

FPO credit is fundamentally different from individual borrower credit. An FPO's creditworthiness cannot be assessed using a standard factory or farm appraisal — it depends on the collective business plan of 500+ diverse farmers operating in an unpredictable agricultural environment. NABARD's guidelines provide two illustrated models showing bankers exactly how to assess and structure FPO loans.

- Model 1 (Annexure I): Pure working capital assessment using cash flow method

- Model 2 (Annexure II): Combined term loan + working capital for capital-intensive FPO businesses

- Both models use ABC FPC Ltd. as the illustrative FPO name in NABARD's document

Why FPO Appraisal Is Unique

Banks must recognise several structural differences when appraising FPO credit:

| Challenge | Why It Matters |

|---|---|

| No individual guarantor | FPO is a collective entity; no personal net worth to fall back on |

| Agriculture is volatile | Weather, policy, price shocks make cash flows erratic |

| Multiple licences required | Delays in getting fertiliser/seed/mandi licences disrupt business |

| Seasonal cash flows | Working capital need peaks at sowing/harvest; banks must allow revolving credit |

| Limited credit history | Most FPOs are 2–5 years old with sparse financial records |

NOTE

NABARD explicitly states FPO business models are unique to location, farming practices, and socio-economic conditions — no two FPOs are identical. This means case-by-case appraisal is mandatory; no standard template can replace cash flow analysis. This principle is directly tested in exam questions on credit appraisal.

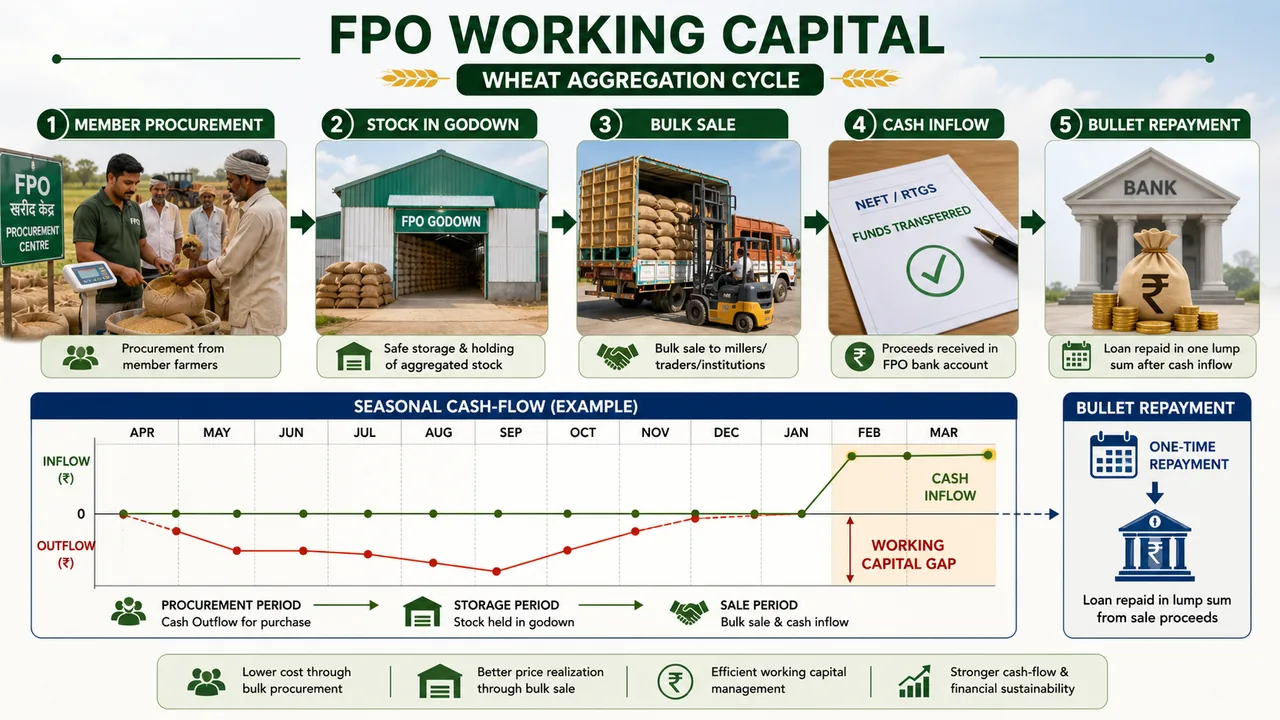

Model 1 — Working Capital Only (Illustrative)

ABC FPC Ltd. — Wheat Aggregation

| Parameter | Value |

|---|---|

| Purpose | Working capital for wheat procurement from members |

| Loan amount | ₹33,00,000 (₹33 lakh) |

| Repayment | Bullet repayment after 13 months |

| Method | Cash flow based (month-wise inflow/outflow) |

How the cash flow method works:

- Map month-wise cash inflows (wheat sales to buyers) and outflows (wheat procurement from farmers)

- Identify peak deficit month → that is the working capital requirement

- Structure repayment as bullet after the selling season ends

NOTE

Working capital for FPOs is assessed using the cash flow method, NOT the traditional turnover method or MPBF (Maximum Permissible Bank Finance) method. The cash flow method captures seasonality — which is why it is mandated for agricultural lending. This is a critical distinction tested in banking exams.

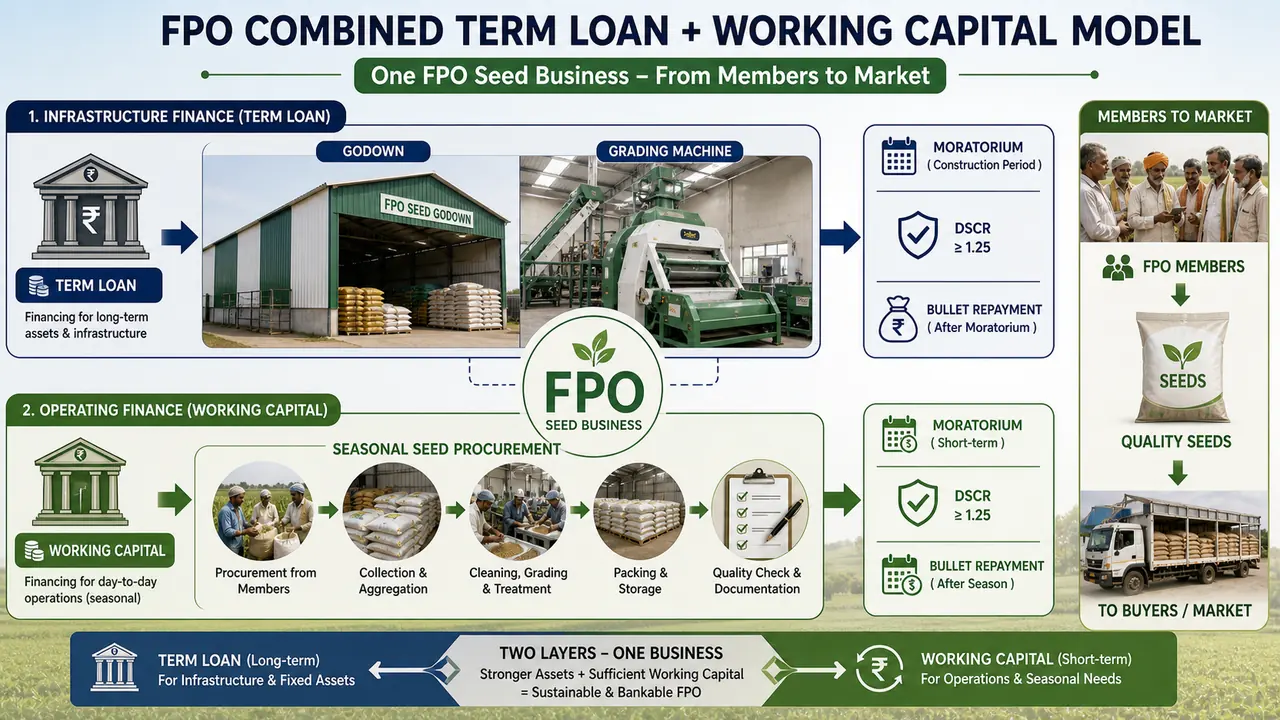

Model 2 — Combined Term Loan + Working Capital

ABC FPC Ltd. — Seed Trading with Godown

| Parameter | Value |

|---|---|

| Purpose (term loan) | Construction of 627 MT godown + grading machine |

| Term loan amount | ₹26,90,000 (₹26.9 lakh) |

| Purpose (working capital) | Procurement of seeds from members |

| Working capital loan | ₹53,00,000 (₹53 lakh) |

| Term loan repayment | 5 years (54 monthly instalments after 6-month moratorium) |

| Working capital repayment | Bullet after 12 months |

Project Cost Breakdown (Term Loan Component):

| Item | Amount (₹) |

|---|---|

| Godown construction (627 MT) | 19,16,035 |

| Land (0.3 acre) | 6,00,000 |

| Subtotal civil works | 25,16,035 |

| Grading machine | 6,51,000 |

| Fire protection unit | (included) |

| Total project cost | ~₹35+ lakh |

Financial Appraisal Methodology

For term loans, NABARD prescribes evaluation through:

| Indicator | What It Measures | Threshold |

|---|---|---|

| BCR (Benefit Cost Ratio) | Total discounted benefits vs costs | > 1.0 |

| IRR (Internal Rate of Return) | Return on investment over project life | > 15% |

| DSCR (Debt Service Coverage Ratio) | Annual surplus vs loan repayment obligation | > 1.5 |

DSCR formula:

DSCR = Net Cash Accrual ÷ (Principal repayment + Interest)

A DSCR of 1.5 means the FPO generates 1.5 times the cash needed for loan servicing — a comfortable buffer.

Critical Appraisal Checks for FPO Loans

Bankers must examine:

Governance Aspects:

- Minutes of board meetings — frequency, quorum, quality of decisions

- Cash books, vouchers, accounts — quality of financial record-keeping

- Member participation rate — what % of members are actually doing business with FPO? (Low participation = red flag)

- Board of Directors involvement in decision-making

Business Aspects:

- Month-wise cash flow projections

- Quotations for plant/machinery (for term loans)

- Market linkages — who are the buyers? Are there signed contracts?

- Technical and managerial capability of CEO/board to run the business

NOTE

Member participation rate is NABARD's single most important governance indicator for FPOs. An FPO with 500 members but only 50 doing business is financially fragile. MCQs test this as the "most important indicator of FPO efficacy."

Working Capital Scenarios (Wheat Aggregation Example)

The same FPO business can have wildly different working capital needs depending on the procurement model:

| Scenario | Working Capital Need |

|---|---|

| FPO buys on credit, sells quickly | Very low |

| FPO buys cash, stores briefly, then sells | High |

| FPO processes wheat into flour before selling | Very high (longer cycle) |

This is why NABARD insists on cash flow analysis rather than rule-of-thumb estimates — the actual WC requirement depends entirely on the specific business model of each FPO.

Security & Credit Guarantee

- Primary security: Hypothecation of current assets (stock of seeds/inputs/produce)

- Collateral: Mortgage of godown/land (for term loan)

- Credit guarantee: SFAC guarantee up to 85% of bank loan — allows collateral-free sanction

- Insurance: All stocks must be insured against fire, flood, pest damage

NOTE

The 6-month moratorium on the term loan means the FPO pays only interest for the first 6 months before principal repayment begins. This gives the FPO time to complete construction of the godown and start operations before facing full EMI burden. Standard for all infrastructure-creating FPO loans.

Sources & References

Primary source for this lesson is NABARD's official Model Bankable Projects portal.[1] Lesson-specific report copy used for this topic.[2]

References

2 sources • [1] [2]

References

Used for: Official NABARD portal for model bankable project documents and updates.

Financing Models: FPO Approach — Working Capital and Term Loan Models — Full Report (Reference Copy)

ReportUsed for: Reference copy used in this lesson for project parameters and worked figures.

The figures in this lesson reflect the cost norms and technical parameters as published in the NABARD document. Actual costs may vary by state, season, and year of implementation. Always refer to the latest NABARD circular for current norms.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Two NABARD models | Model 1 (Annexure I): pure working capital; Model 2 (Annexure II): term loan + working capital |

| Illustrative FPO name | ABC FPC Ltd. (used in NABARD's document) |

| Model 1 — Working Capital | Wheat aggregation; loan amount ₹33 lakh; repayment: bullet after 13 months |

| Working capital assessment method | Cash flow method (NOT turnover method or MPBF) — mandatory for agriculture to capture seasonality |

| Model 2 — Term Loan | Seed trading with godown; term loan ₹26.9 lakh (627 MT godown + grading machine) |

| Model 2 — Working Capital | Seed procurement; working capital loan ₹53 lakh |

| Term loan repayment | 5 years (54 monthly instalments after 6-month moratorium) |

| Working capital repayment (Model 2) | Bullet after 12 months |

| Moratorium purpose | Allows godown construction completion before full EMI burden starts |

| Key appraisal indicators | BCR (>1.0), IRR (>15%), DSCR (>1.5) |

| DSCR formula | Net Cash Accrual ÷ (Principal repayment + Interest) |

| Credit guarantee | SFAC — up to 85% of bank loan; allows collateral-free sanction |

| Primary security | Hypothecation of current assets (stock of seeds/inputs/produce) |

| Collateral | Mortgage of godown/land (for term loan) |

| Most important governance indicator | Member participation rate — % of members actually doing business with FPO (low = red flag) |

| FPO appraisal uniqueness | Case-by-case cash flow analysis mandatory; no standard template applies |

| Key challenges | No individual guarantor, volatile agri cash flows, seasonal peaks, limited credit history, licence delays |

| WC scenarios | Buy-on-credit + quick sale = low WC; cash purchase + storage = high WC; processing before sale = very high WC |

Lesson Doubts

Ask questions, get expert answers