₹ Cost Concepts in Economics & Farm Management

Understand all cost concepts — fixed, variable, marginal, opportunity, and CACP cost structures (A1 to C3) — with agricultural examples, tables, and exam tips.

Why Costs Matter in Agriculture

Imagine a wheat farmer in Punjab deciding whether to grow wheat or mustard this season. She must consider the price of seeds, fertilizer, labour, tractor hire, and even the rent she could earn by leasing her land. Every rupee spent — and every rupee not earned from the alternative crop — is a cost. Understanding these costs is the foundation of smart farming and sound economics.

This lesson walks you through every cost concept, from the simplest to the most exam-critical, with agricultural examples at every step.

1. Basic Cost Types

Nominal Cost (Money Cost)

The cost of production measured at current market prices, with no adjustment for inflation.

Example: A farmer spends Rs 5,000 on DAP fertilizer in 2025. That Rs 5,000 is the nominal cost — the actual cash paid today.

Real Cost

The cost of production expressed at constant (base-year) prices, removing the effect of inflation.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

Charged once for one year · ₹1188 total

Save ₹100/month vs ₹2388/year launch price

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure one-time yearly payment via Razorpay · No hidden fees

Why Costs Matter in Agriculture

Imagine a wheat farmer in Punjab deciding whether to grow wheat or mustard this season. She must consider the price of seeds, fertilizer, labour, tractor hire, and even the rent she could earn by leasing her land. Every rupee spent — and every rupee not earned from the alternative crop — is a cost. Understanding these costs is the foundation of smart farming and sound economics.

This lesson walks you through every cost concept, from the simplest to the most exam-critical, with agricultural examples at every step.

1. Basic Cost Types

Nominal Cost (Money Cost)

The cost of production measured at current market prices, with no adjustment for inflation.

Example: A farmer spends Rs 5,000 on DAP fertilizer in 2025. That Rs 5,000 is the nominal cost — the actual cash paid today.

Real Cost

The cost of production expressed at constant (base-year) prices, removing the effect of inflation.

Example: DAP cost Rs 3,000 in 2015 and Rs 5,000 in 2025. After adjusting for inflation, the real cost may have risen by only 20%, not 67%. Real cost reveals the true change in resource burden.

| Basis | Nominal Cost | Real Cost |

|---|---|---|

| Price basis | Current market prices | Constant (base-year) prices |

| Inflation | Included | Removed |

| Use | Day-to-day accounting | Comparing costs across years |

Deflated Cost

Costs adjusted by a general price index to remove inflation — essentially the same idea as real cost applied in practice.

Example: If the wholesale price index (WPI) doubled over 10 years, deflated cost = nominal cost / price index.

2. Opportunity Cost (Alternate Cost)

Definition: The value of the return sacrificed from the next best alternative use of a resource.

Example: A farmer grows paddy instead of maize on his 2-hectare plot. If maize would have earned Rs 80,000, then the opportunity cost of choosing paddy is Rs 80,000 — regardless of what paddy actually costs to grow.

Key points:

- Introduced by J.S. Mill

- Opportunity cost of free goods (sunlight, air) = Zero

- Opportunity cost of unlimited/abundant resources = Zero

- Farmers don't pay cash for family labour or owned bullocks, but their opportunity cost is still counted in economic analysis

Exam Tip: "Who introduced opportunity cost?" — J.S. Mill. "Opportunity cost of free goods?" — Always zero.

3. Economic Cost = Explicit + Implicit

| Type | Also Called | What It Includes | Agricultural Example |

|---|---|---|---|

| Explicit Cost | Paid-out cost, Cash cost | All actual cash payments | Wages to hired labour, purchased seeds, fertilizer bills |

| Implicit Cost | Imputed cost | Opportunity cost of own resources | Rental value of owned land, value of family labour, interest on own capital |

Formula: Economic Cost = Explicit (Accounting) Cost + Implicit Cost

- Accounting cost includes only explicit costs (what goes in the account book).

- Economic cost is always greater than or equal to accounting cost because it adds implicit costs.

Example: A farmer pays Rs 50,000 in cash expenses (explicit). He also uses his own land (could rent for Rs 20,000) and family labour (worth Rs 15,000). Economic cost = 50,000 + 20,000 + 15,000 = Rs 85,000.

4. Social Cost (Externalities)

Definition: Costs imposed on society beyond the private costs borne by the producer.

- Term coined by Ronald Coase

- Private cost = explicit + implicit costs borne by the firm

- Social cost = private cost + external costs to society

Example: A pesticide factory pollutes a river. The factory's private cost is its production expense, but the village downstream bears health costs and fishery losses — these are social costs.

- Negative externality = social costs outweigh social benefits (e.g., groundwater depletion from excessive bore-well irrigation)

5. Other Cost Classifications

Separable vs Common Costs

| Type | Definition | Example |

|---|---|---|

| Separable Cost | Can be traced to a specific product | Cost of cotton seeds — applies only to the cotton crop |

| Common (Joint) Cost | Shared across multiple products, cannot be separated | Irrigation canal serving wheat, mustard, and gram fields simultaneously |

Historical vs Replacement Costs

| Type | Definition | Example |

|---|---|---|

| Historical Cost | Original purchase price of a durable asset | Tractor bought in 2015 for Rs 1,50,000 |

| Replacement Cost | Difference between current price and original price | Same tractor now costs Rs 2,50,000; replacement cost = Rs 1,00,000 |

Exam Tip: Historical cost is used in accounting records; replacement cost matters for capital planning — knowing how much you need to replace worn-out equipment.

Establishment Costs (First Phase Costs)

One-time costs incurred before production begins — construction of farm buildings, installation of tube wells, purchase of machinery.

Example: A dairy farmer builds a cattle shed for Rs 3,00,000 before starting milk production. This is an establishment/first phase cost.

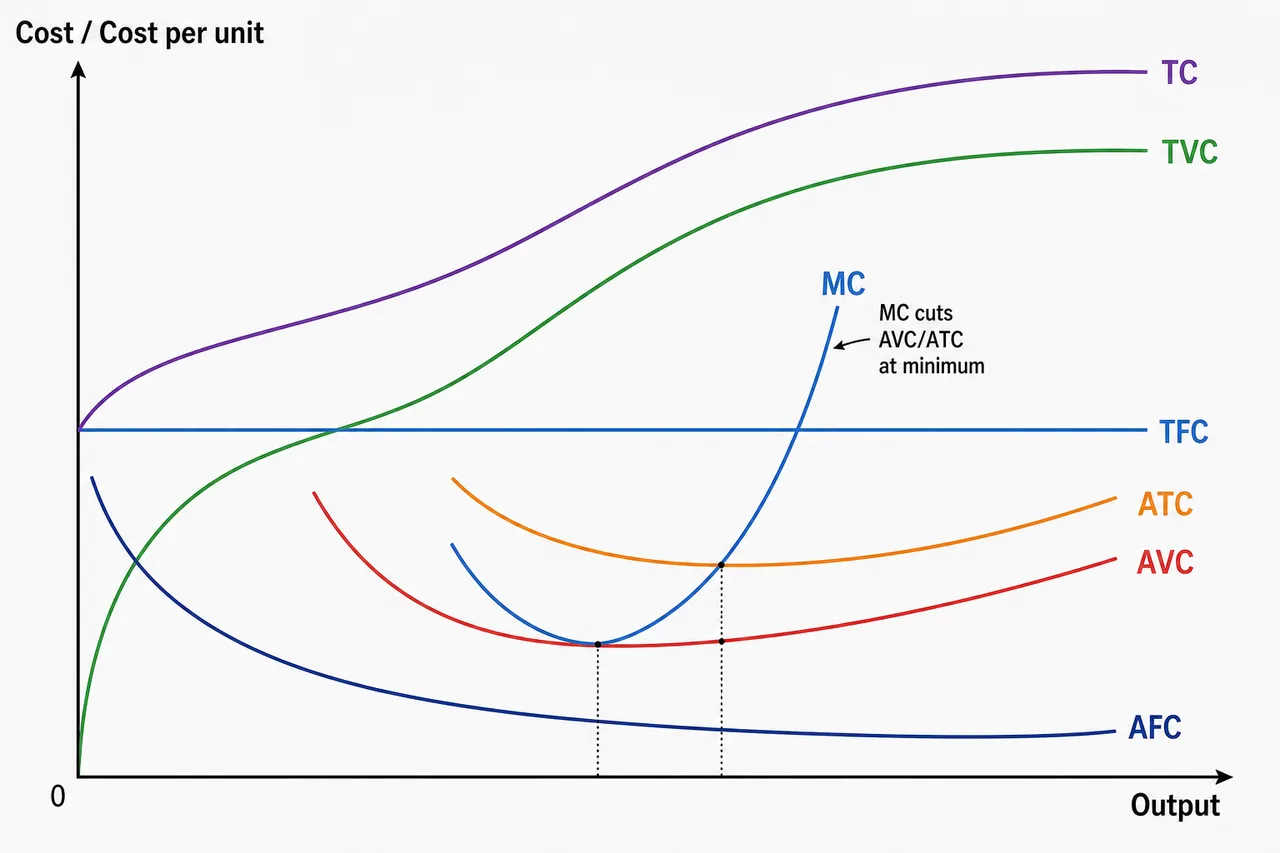

6. Short-Run Cost Curves

Cost is a function of output. In the short run, some inputs are fixed (land, machinery); in the long run, all inputs can be varied (no fixed costs exist).

Mnemonic — "FOSS": Fixed in Short run, Only variable in long run → no fixed costs in the Long run.

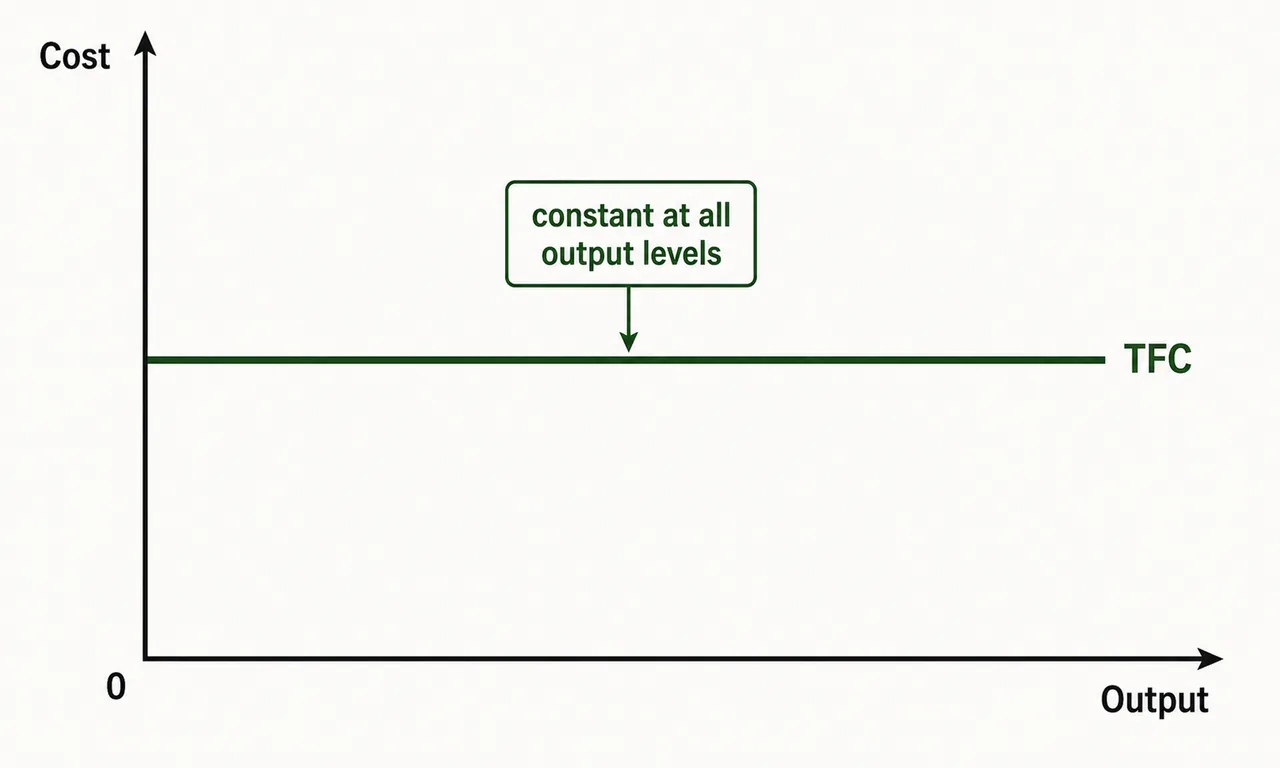

Fixed Cost (FC)

- Does not change with output level

- Incurred even at zero production

- Also called: Overhead Cost, Sunk Cost, Indirect Cost

| Cash Fixed Costs | Non-Cash Fixed Costs |

|---|---|

| Land taxes | Depreciation on machinery |

| Insurance premiums | Cost of family labour |

| Interest on loans | Interest on owned fixed capital |

| Annually hired labour | Management costs |

TFC curve: Horizontal straight line parallel to the X-axis.

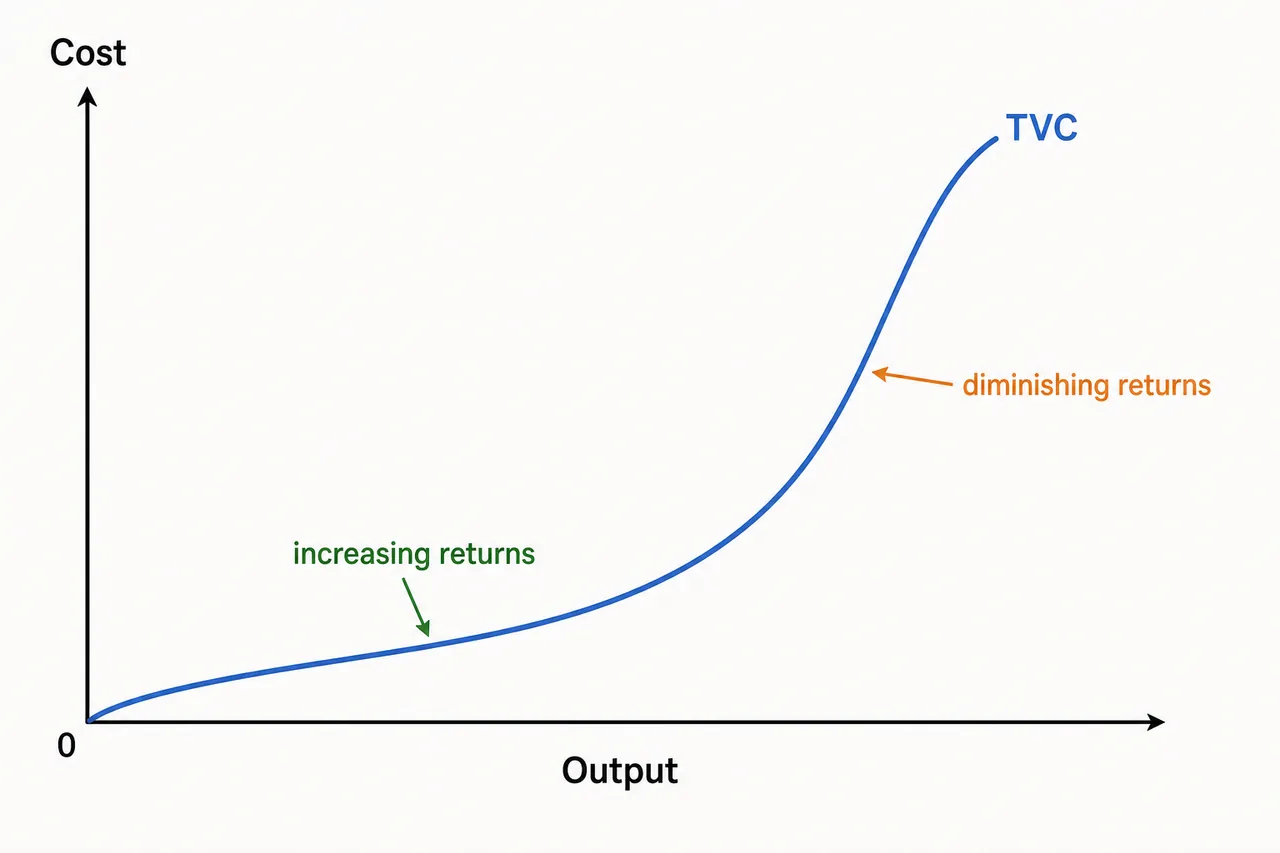

Variable Cost (VC)

- Changes with the level of output

- Falls to zero when production stops

- Also called: Working Cost, Operating Cost, Direct Cost, Prime Cost, Running Cost

- These are second phase costs (incurred during production, unlike establishment costs)

Examples in farming: Seeds, fertilizer, diesel, hired casual labour, feed, irrigation water, pesticides, current repairs.

Farming Expenses = f (farm output)

TVC curve: Inverse S-shape (initially rises slowly due to increasing returns, then rises steeply due to diminishing returns).

Total Cost (TC)

TC = TFC + TVC = Explicit Cost + Implicit Cost

- TC curve has the same shape as TVC, shifted upward by the constant TFC amount.

- At zero output, TC = TFC (fixed costs still apply).

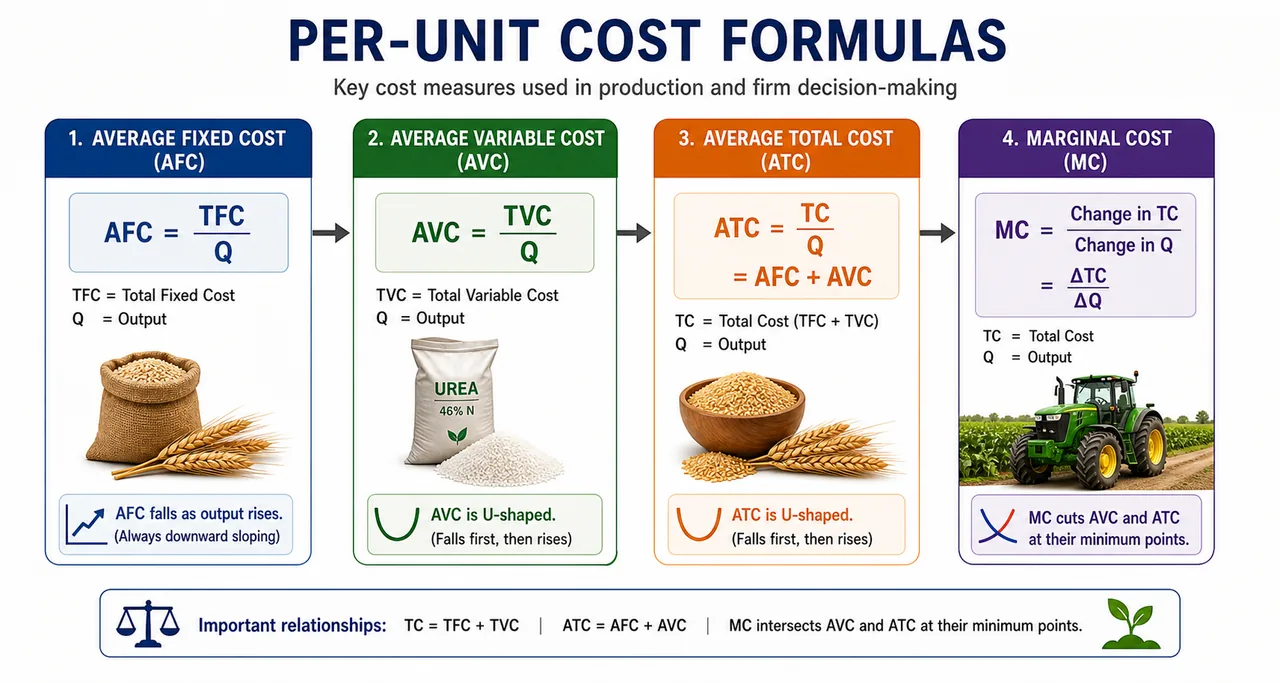

7. Per-Unit Cost Curves

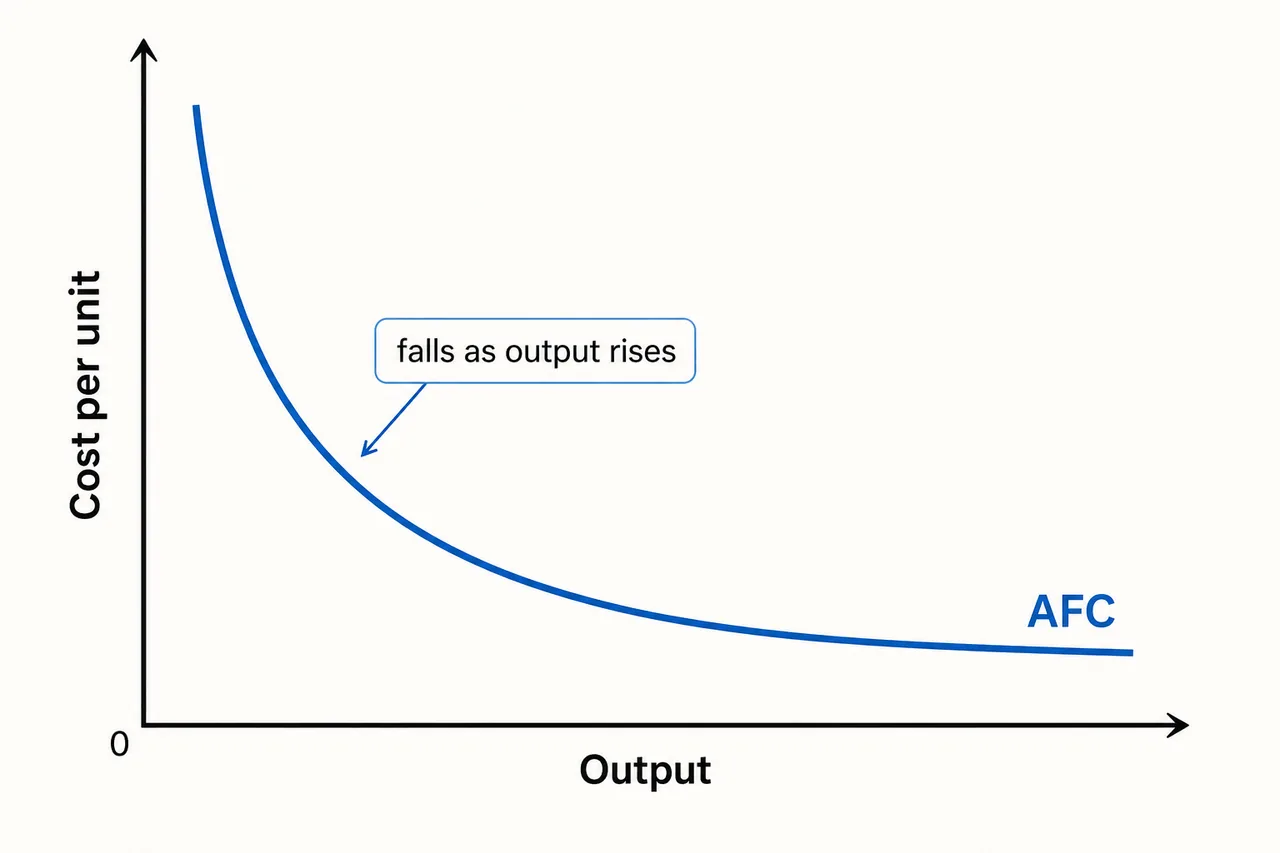

Average Fixed Cost (AFC)

AFC = TFC / Q

- Continuously falls as output increases (same fixed cost spread over more units)

- Shape: Rectangular hyperbola (never touches the X-axis)

Example: A farmer pays Rs 20,000 in land tax (fixed). If she produces 100 quintals, AFC = Rs 200/quintal. If she produces 400 quintals, AFC = Rs 50/quintal.

Average Variable Cost (AVC)

AVC = TVC / Q

- U-shaped curve (parabolic)

- AVC is the reciprocal of Average Physical Product (APP)

- AVC is minimum when APP is maximum

- Beyond the optimal point, diminishing returns push AVC upward

Example: When a farmer uses the first few bags of urea on wheat, each bag adds a lot of grain (high APP, low AVC). After optimal dosage, extra urea adds less grain (low APP, high AVC).

Average Total Cost (ATC or AC)

ATC = TC / Q = AFC + AVC

- U-shaped curve

- Initially falls because declining AFC dominates

- Later rises because increasing AVC outweighs declining AFC

- The lowest point = most efficient scale of production

Marginal Cost (MC)

MC = Change in TC / Change in Q

- The cost of producing one additional unit

- Marginal Fixed Cost = always zero (FC does not change with output)

- Therefore MC = Marginal Variable Cost only

- MC is independent of the size of fixed cost

Example: A farmer cultivates vegetables on a fixed plot. Adding one more unit of labour costs Rs 500 and produces 2 more quintals. MC = Rs 250/quintal. The rent paid for the land does not affect this calculation.

Key MC relationships:

- MC is U-shaped — falls first (increasing efficiency), then rises (diminishing returns)

- When MPP is maximum, MC is minimum

- When MPP is zero, MC becomes vertical (infinite cost for zero extra output)

- MC intersects AVC and ATC at their minimum points — below the average, it pulls it down; above the average, it pulls it up

8. Cost Curve Summary

Mnemonic — "H-I-I-R-U-U-U": Remember the curve shapes in order: TFC-TVC-TC-AFC-AVC-ATC-MC

| Cost Curve | Shape | Key Feature |

|---|---|---|

| TFC | Horizontal straight line | Parallel to X-axis, never changes |

| TVC | Inverse S-shape | Reflects increasing then diminishing returns |

| TC | Same as TVC (shifted up) | Starts from TFC level, not origin |

| AFC | Rectangular hyperbola | Always declining, never touches X-axis |

| AVC | U-shaped | Minimum where APP is maximum |

| ATC | U-shaped | Minimum point is to the right of AVC minimum |

| MC | U-shaped | Cuts AVC and ATC at their minimum points |

Critical relationships:

- Vertical distance between ATC and AVC = AFC (narrows as output rises)

- When ATC is falling, MC is below ATC

- When ATC is rising, MC is above ATC

Table of Different Costs (Cost in Rupees)

| Units of Production | FC | VC | TC = FC + VC | AFC = FC/Q | AVC = VC/Q | ATC = TC/Q | MC = ΔVC/ΔQ |

|---|---|---|---|---|---|---|---|

| 0 | 25 | 0 | 25 | ∞ | - | ∞ | - |

| 4 | 25 | 4 | 39 | 6.25 | 1.00 | 7.25 | 1.00 |

| 12 | 25 | 8 | 33 | 2.08 | 0.66 | 2.70 | 0.50 |

| 18 | 25 | 12 | 37 | 1.38 | 0.66 | 2.50 | 0.66 |

| 23 | 25 | 16 | 41 | 1.08 | 0.69 | 1.78 | 0.80 |

| 27 | 25 | 20 | 45 | 0.92 | 0.74 | 1.66 | 1.00 |

| 30 | 25 | 24 | 49 | 0.83 | 0.80 | 1.63 | 1.33 |

| 32 | 25 | 28 | 53 | 0.78 | 0.87 | 1.65 | 2.00 |

| 33 | 25 | 32 | 57 | 0.75 | 0.96 | 0.72 | 4.00 |

Three key observations from the data:

- Fixed costs remain the same at every production level

- Variable costs change with production level

- Total cost and variable cost increase with rising production

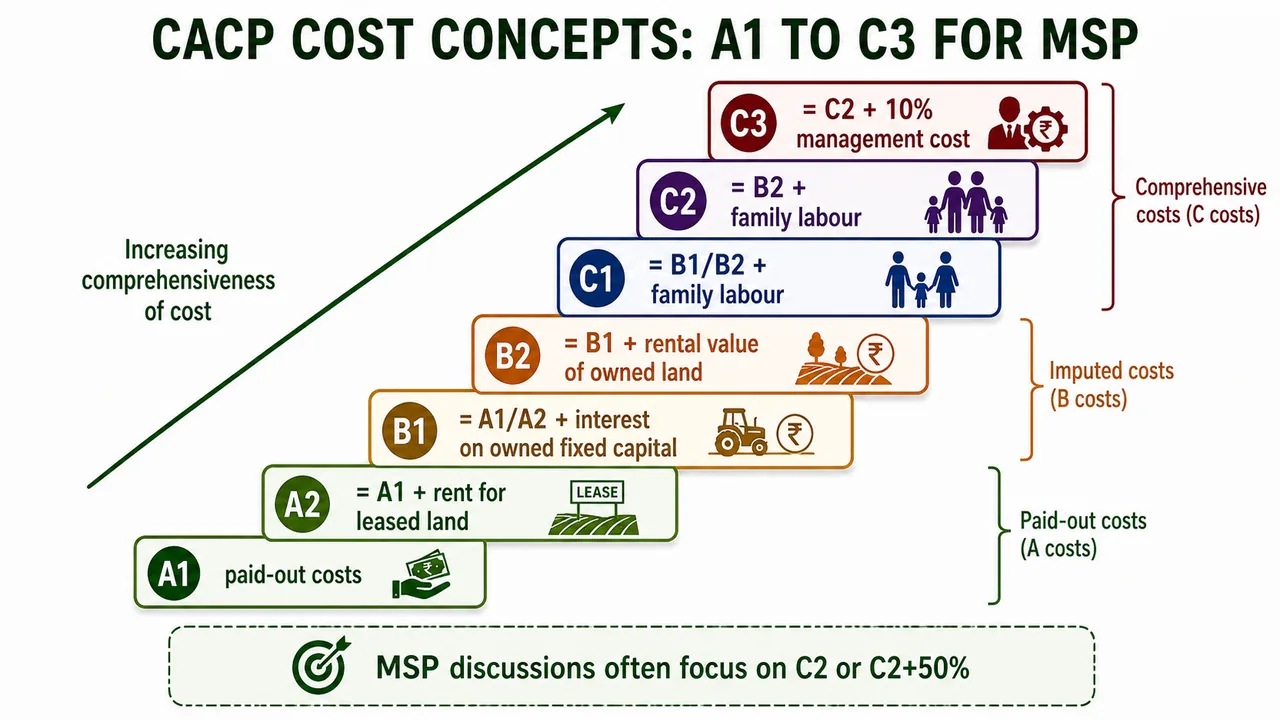

9. CACP Cost Concepts in Farm Management

The Commission for Agricultural Costs and Prices (CACP) developed a standardized cost framework used across India. These cost concepts (A1 through C3) form the basis for Minimum Support Price (MSP) determination.

Exam Alert: CACP cost concepts are among the most frequently asked topics in exams, FCI, NABARD, and exams.

Cost A1 — The 16 Paid-Out Items

Cost A1 includes all actual cash expenses incurred by the farmer:

- Value of hired human labour (permanent & casual)

- Value of owned bullock labour

- Value of hired bullock labour

- Value of owned machinery

- Hired machinery charges

- Value of fertilizers

- Value of manure (farm-produced & purchased)

- Value of seed (farm-produced & purchased)

- Value of insecticides & fungicides

- Irrigation charges (owned & hired tube wells, pumping sets)

- Canal water charges

- Land revenue, cesses, and other taxes

- Depreciation on farm implements

- Depreciation on farm buildings, machinery & irrigation structures

- Interest on working capital

- Miscellaneous expenses (artisan wages, ropes, small repairs)

Mnemonic for remembering A1 has 16 items: "A1 = Sweet 16" — the 16 actual paid-out costs.

Building Up from A1 to C3

| Cost | Formula | What It Adds |

|---|---|---|

| A1 | 16 paid-out cost items | All actual cash expenses |

| A2 | A1 + Rent for leased land | Lease rental |

| B1 | A1 + Interest on owned fixed capital (excl. land) | Opportunity cost of owned equipment |

| B2 | B1 + Rental value of owned land + Rent for leased land | Opportunity cost of owned land |

| C1 | B1 + Imputed value of family labour | Unpaid family work |

| C2 | B2 + Imputed value of family labour | Most comprehensive cost |

| C2* | C2 adjusted for statutory/market wage rate | Labour at minimum wage |

| C3 | C2* + 10% of C2* | Managerial input of farmer |

Exam Tip — "ABC progression":

- A costs = actual paid-out costs

- B costs = A costs + imputed capital costs (no family labour yet)

- C costs = B costs + imputed family labour (the full picture)

Cost C consists of 20 items: Cost A1 (16 items) + Rent for leased land + Imputed value of owned land + Interest on owned fixed capital + Imputed value of family labour

Net Income = Gross Return - Cost C

Cost of Production = Cost C / Output

10. Cost of Production vs Cost of Cultivation

| Measure | Unit | Primary Use |

|---|---|---|

| Cost of Production (CoP) | Rs per quintal | MSP determination |

| Cost of Cultivation (CoC) | Rs per hectare | Comparing investment intensity across crops/regions |

Exam fact (exams 2017): Cost of Cultivation is measured in Rs per hectare.

Memory trick: Production = per Quintal (product output), Cultivation = per Hectare (land area).

Master Summary Table

| Concept | Definition (One Line) | Key Fact for Exams |

|---|---|---|

| Nominal Cost | Cost at current prices | No inflation adjustment |

| Real Cost | Cost at constant prices | Removes inflation effect |

| Opportunity Cost | Value of next best alternative foregone | Introduced by J.S. Mill; zero for free goods |

| Explicit Cost | Actual cash payments | = Accounting cost |

| Implicit Cost | Imputed value of own resources | Rent of own land, family labour |

| Economic Cost | Explicit + Implicit | Always >= Accounting cost |

| Social Cost | Private cost + externalities | Named by Ronald Coase |

| Fixed Cost | Does not vary with output | TFC = horizontal line; also called sunk/overhead cost |

| Variable Cost | Varies with output | TVC = inverse S-shape; also called prime/direct cost |

| AFC | TFC / Q | Rectangular hyperbola, always declining |

| AVC | TVC / Q | U-shaped; minimum at maximum APP |

| ATC | TC / Q = AFC + AVC | U-shaped; minimum to right of AVC minimum |

| MC | Change in TC / Change in Q | U-shaped; cuts AVC & ATC at their minimums |

| Cost A1 | 16 paid-out items | Base for all CACP costs |

| Cost C2 | B2 + family labour | Most comprehensive; basis for MSP |

| Cost C3 | C2* + 10% managerial cost | Highest cost concept |

| CoP | Cost per quintal | Used for MSP |

| CoC | Cost per hectare | Used for regional comparison |

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Nominal Cost | Cost at current market prices, no inflation adjustment |

| Real Cost | Cost at constant (base-year) prices, removes inflation effect |

| Deflated Cost | Nominal cost divided by price index to remove inflation |

| Opportunity Cost | Value of the next best alternative foregone; introduced by J.S. Mill; zero for free goods |

| Explicit Cost | Actual cash payments (hired labour wages, purchased seeds, fertilizer bills); = Accounting cost |

| Implicit Cost | Imputed value of own resources (rental value of owned land, family labour, interest on own capital) |

| Economic Cost | Explicit + Implicit cost; always ≥ Accounting cost |

| Social Cost | Private cost + externalities imposed on society; term coined by Ronald Coase |

| Separable Cost | Traced to a specific product (e.g., cotton seeds for cotton crop) |

| Common (Joint) Cost | Shared across multiple products, cannot be separated (e.g., irrigation canal serving multiple crops) |

| Historical Cost | Original purchase price of a durable asset |

| Replacement Cost | Difference between current price and original price of the asset |

| Establishment Cost | One-time costs incurred before production begins (farm buildings, tube wells) |

| Fixed Cost (FC) | Does not change with output; incurred even at zero production; TFC curve = horizontal line; also called overhead/sunk/indirect cost |

| Variable Cost (VC) | Changes with output; zero when production stops; TVC curve = inverse S-shape; also called prime/direct/working cost |

| Total Cost (TC) | TFC + TVC; same shape as TVC shifted up by TFC amount |

| Average Fixed Cost (AFC) | TFC / Q; continuously falls; shape = rectangular hyperbola (never touches X-axis) |

| Average Variable Cost (AVC) | TVC / Q; U-shaped; minimum when APP is maximum |

| Average Total Cost (ATC) | TC / Q = AFC + AVC; U-shaped; minimum point to the right of AVC minimum |

| Marginal Cost (MC) | ΔTC / ΔQ; U-shaped; intersects AVC and ATC at their minimum points; minimum when MPP is maximum |

| MC & Fixed Cost | Marginal Fixed Cost = always zero; MC = Marginal Variable Cost only; MC is independent of fixed cost size |

| Cost Curve Shapes (H-I-I-R-U-U-U) | TFC=Horizontal, TVC=Inverse-S, TC=Inverse-S shifted, AFC=Rectangular hyperbola, AVC=U, ATC=U, MC=U |

| Cost A1 | 16 paid-out items (hired labour, seeds, fertilizers, depreciation, irrigation, interest on working capital, etc.) — "A1 = Sweet 16" |

| Cost A2 | A1 + Rent for leased land |

| Cost B1 | A1 + Interest on owned fixed capital (excl. land) |

| Cost B2 | B1 + Rental value of owned land + rent for leased land |

| Cost C1 | B1 + Imputed value of family labour |

| Cost C2 | B2 + Imputed value of family labour — most comprehensive cost; basis for MSP |

| Cost C3 | C2 + 10%* of C2* for managerial input — highest cost concept |

| Cost of Production (CoP) | Cost per quintal; used for MSP determination |

| Cost of Cultivation (CoC) | Cost per hectare; used for regional comparison |

| ABC Progression | A = actual paid-out; B = A + imputed capital costs; C = B + imputed family labour |

| Net Income Formula | Gross Return − Cost C |