💳 Public Revenue: Sources, Taxation & Agricultural Income

Understand government revenue sources, types of taxes, canons of taxation, GST, and agricultural income exemptions — with agricultural examples and exam-focused mnemonics.

Why Public Revenue Matters for Agriculture

Imagine a farmer in Madhya Pradesh whose village gets a new irrigation canal, a soil testing laboratory, and a subsidised seed distribution centre. Who pays for all this? The government — using money collected from the public. This money is called public revenue.

Public revenue refers to all the income and receipts that the government collects to finance its expenditure on public goods, services, and welfare programmes — including agricultural subsidies, rural infrastructure, and farmer welfare schemes like PM-KISAN.

Sources of Revenue

The government needs funds for defence, education, health, industry, and — critically for us — agriculture. These funds come from two broad categories:

| Category | Sources | Nature |

|---|---|---|

| Major Sources | Taxes, Prices | Generate bulk of revenue |

| Minor Sources | Fees, Special Assessment, Rates, Escheat, Grants, Gifts, Donations, Tributes & Indemnities | Supplementary revenue |

Major Sources

1. Tax

A tax is a mandatory, compulsory payment levied by the government on individuals and businesses. Key features:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

Charged once for one year · ₹1188 total

Save ₹100/month vs ₹2388/year launch price

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure one-time yearly payment via Razorpay · No hidden fees

Why Public Revenue Matters for Agriculture

Imagine a farmer in Madhya Pradesh whose village gets a new irrigation canal, a soil testing laboratory, and a subsidised seed distribution centre. Who pays for all this? The government — using money collected from the public. This money is called public revenue.

Public revenue refers to all the income and receipts that the government collects to finance its expenditure on public goods, services, and welfare programmes — including agricultural subsidies, rural infrastructure, and farmer welfare schemes like PM-KISAN.

Sources of Revenue

The government needs funds for defence, education, health, industry, and — critically for us — agriculture. These funds come from two broad categories:

| Category | Sources | Nature |

|---|---|---|

| Major Sources | Taxes, Prices | Generate bulk of revenue |

| Minor Sources | Fees, Special Assessment, Rates, Escheat, Grants, Gifts, Donations, Tributes & Indemnities | Supplementary revenue |

Major Sources

1. Tax

A tax is a mandatory, compulsory payment levied by the government on individuals and businesses. Key features:

- Compulsory — you cannot choose not to pay it

- No direct benefit — revenue is used for the general welfare of society

- A farmer paying income tax on non-agricultural business income gets no specific service in return

2. Price

A price is a voluntary payment for a service of business character. You only pay if you choose to use the service.

- Examples: Railway freight charges for transporting grain, electricity charges for running tube wells, bus fare to the mandi

- Unlike a tax, you can avoid a price by not purchasing the service

| Feature | Tax | Price |

|---|---|---|

| Nature | Compulsory | Voluntary |

| Benefit | No direct benefit | Specific service received |

| Avoidable? | No | Yes |

| Agricultural example | Income tax on agri-business | Electricity for irrigation pump |

Minor Sources

1. Fee

A fee is a compulsory payment made only by those who receive a specific service from the government. It covers part of the cost of the service.

- Examples: Court fees, land registration fees, APMC market fee, seed certification fee

- A licence fee (e.g., pesticide dealer licence) may exceed the cost of the service rendered

Exam Tip: Fee = Specific service in return. Tax = No specific service. This is the key difference.

2. Special Assessment

A compulsory contribution levied on property owners who benefit disproportionately from a specific public improvement.

- Agricultural example: If the government builds a canal or a rural road, nearby farmland appreciates in value. The State can levy a special assessment on those landowners to recover part of the construction cost.

3. Rates

Levied by local bodies (municipalities, panchayats, district boards) for local services such as street lighting, sanitation, water supply, and road maintenance.

- Agricultural example: A gram panchayat levying a rate on property to maintain village drainage and water supply systems

4. Escheat

When a person dies intestate (without a will) and has no legal heirs, their property reverts to the State. A minor but noteworthy source of revenue.

5. Tributes and Indemnities

- Tributes — paid by conquered countries

- Indemnities — compensation for war damage

These are historically significant but rare in modern times.

6. Grants, Gifts, and Donations

| Type | Meaning | Agricultural Example |

|---|---|---|

| Grants | Funds from apex bodies to subordinate organisations | ICAR grants to State Agricultural Universities (SAUs) |

| Gifts | Funds from foreign countries during calamities | Foreign aid after a severe drought or flood |

| Donations | Funds from individuals for specific purposes | A philanthropist funding a Krishi Vigyan Kendra building |

Tax — Core Concepts

Seligman defines tax as a compulsory contribution from a person to the state to defray expenses incurred in the common interest of all, without reference to special benefit conferred.

Impact vs. Incidence of Tax

Two critical concepts every exam tests:

| Concept | Meaning | Example |

|---|---|---|

| Impact | Falls on the person who initially pays the tax | A fertiliser manufacturer pays excise duty |

| Incidence | Falls on the person who ultimately bears the burden | The farmer pays a higher price for fertiliser |

Exam Tip — Mnemonic: "Impact = Initial payer. Incidence = In the end (ultimate bearer)."

Impact and incidence may or may not fall on the same person.

Methods of Taxation (Simple to Complex)

1. Proportional Tax

The same rate or percentage of tax is charged regardless of income level.

- Example: A 10% agricultural cess — a farmer earning Rs. 1,00,000 pays Rs. 10,000; a farmer earning Rs. 10,00,000 pays Rs. 1,00,000

- Simple to administer but ignores differences in ability to pay

2. Progressive Tax

The rate of tax increases as income increases. Based on the principle: "Higher the income, higher the tax."

- Grounded in the law of diminishing marginal utility of money — as income rises, each additional rupee provides less satisfaction, so higher earners can afford a higher tax rate with less hardship

- Example: India's income tax slabs — a small agri-business owner earning Rs. 5 lakhs pays 5%, while one earning Rs. 15 lakhs pays 30% on the highest slab

- India's income tax system is the prime example of progressive taxation

3. Regressive Tax

The tax burden falls more heavily on the poor than on the rich. The poor pay a larger proportion of their income.

- Opposite of progressive tax

- Most indirect taxes (like GST on essential goods) tend to be regressive — a marginal farmer and a wealthy landowner both pay the same Rs. 5 tax on a packet of seeds

- Agricultural example: A flat-rate market cess on all produce sold at APMC hits small farmers harder proportionally

4. Degressive Tax

A tax that is progressive up to a certain limit, beyond which a uniform rate is charged.

- Example: A state agricultural income tax that is progressive up to Rs. 10 lakhs but charges a flat 15% above that

- Fails to achieve full equity in taxation

| Method | Rate Pattern | Equity | Agricultural Example |

|---|---|---|---|

| Proportional | Same % for all | Low | Flat 10% cess on all farm income |

| Progressive | Rate rises with income | High | Income tax slabs on agri-business |

| Regressive | Burden heavier on poor | Very Low | Flat market cess on APMC sales |

| Degressive | Progressive then flat | Moderate | Progressive up to Rs. 10L, flat above |

Exam Tip — Mnemonic: "P-P-R-D" — Proportional (same), Progressive (rises), Regressive (reverse), Degressive (dies out).

Classification of Tax

By Basis of Levy

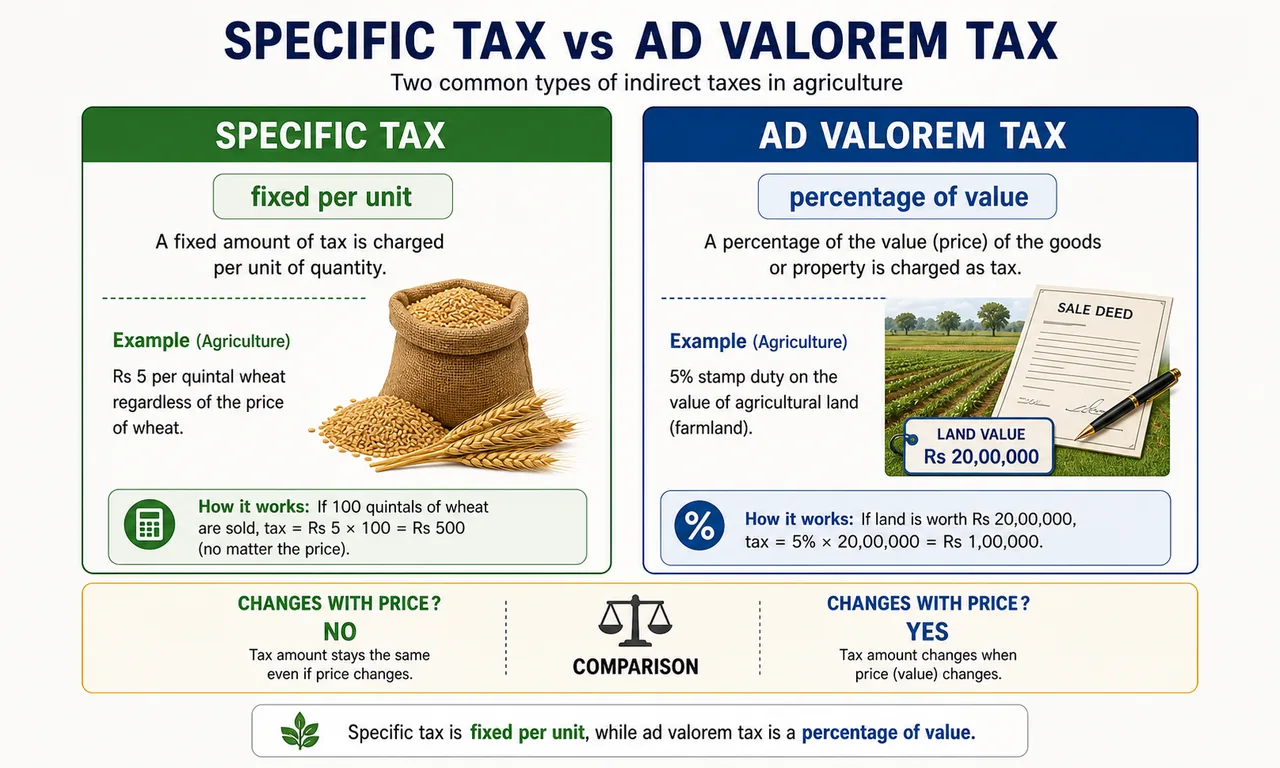

Specific Tax

A fixed amount charged per unit of a commodity, regardless of its price.

- Agricultural example: A tax of Rs. 5 per quintal on wheat arriving at the mandi — whether the wheat is priced at Rs. 2,000 or Rs. 2,500 per quintal, the tax remains Rs. 5

Ad Valorem Tax

A tax based on the value of a commodity. The Latin term means "according to value." The tax amount increases as the price increases.

- Agricultural example: Stamp duty on farmland purchase — if stamp duty is 5%, a plot worth Rs. 10 lakhs attracts Rs. 50,000, while a plot worth Rs. 20 lakhs attracts Rs. 1,00,000

| Type | Basis | Changes with Price? | Agricultural Example |

|---|---|---|---|

| Specific | Per unit (weight/quantity) | No | Rs. 5/quintal on wheat |

| Ad Valorem | Percentage of value | Yes | 5% stamp duty on farmland |

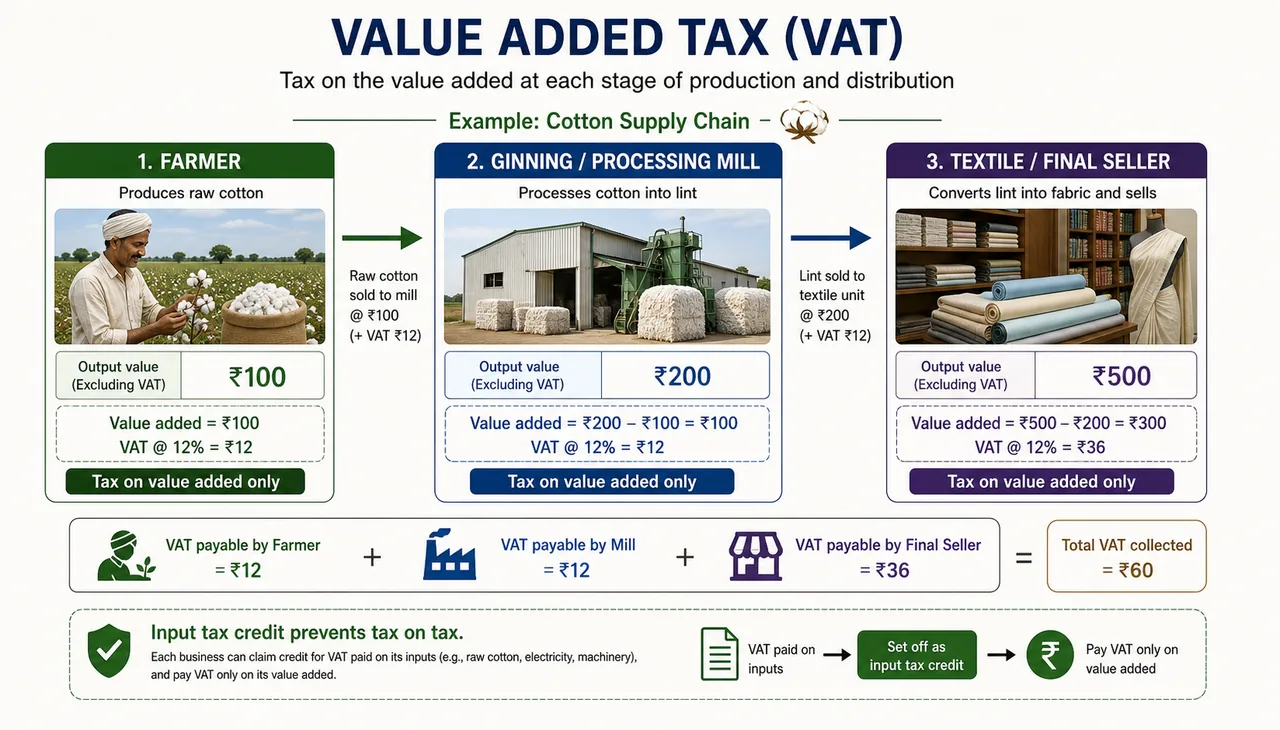

Value Added Tax (VAT)

VAT is levied on the value added at each stage of the production and distribution chain. Credit is given for tax already paid on inputs, avoiding the cascading effect (tax on tax).

- Agricultural example: A cotton farmer sells raw cotton (Stage 1) → Ginning mill processes it (Stage 2) → Textile factory weaves fabric (Stage 3). VAT applies only to the value added at each stage, not the full value.

By Ability to Shift

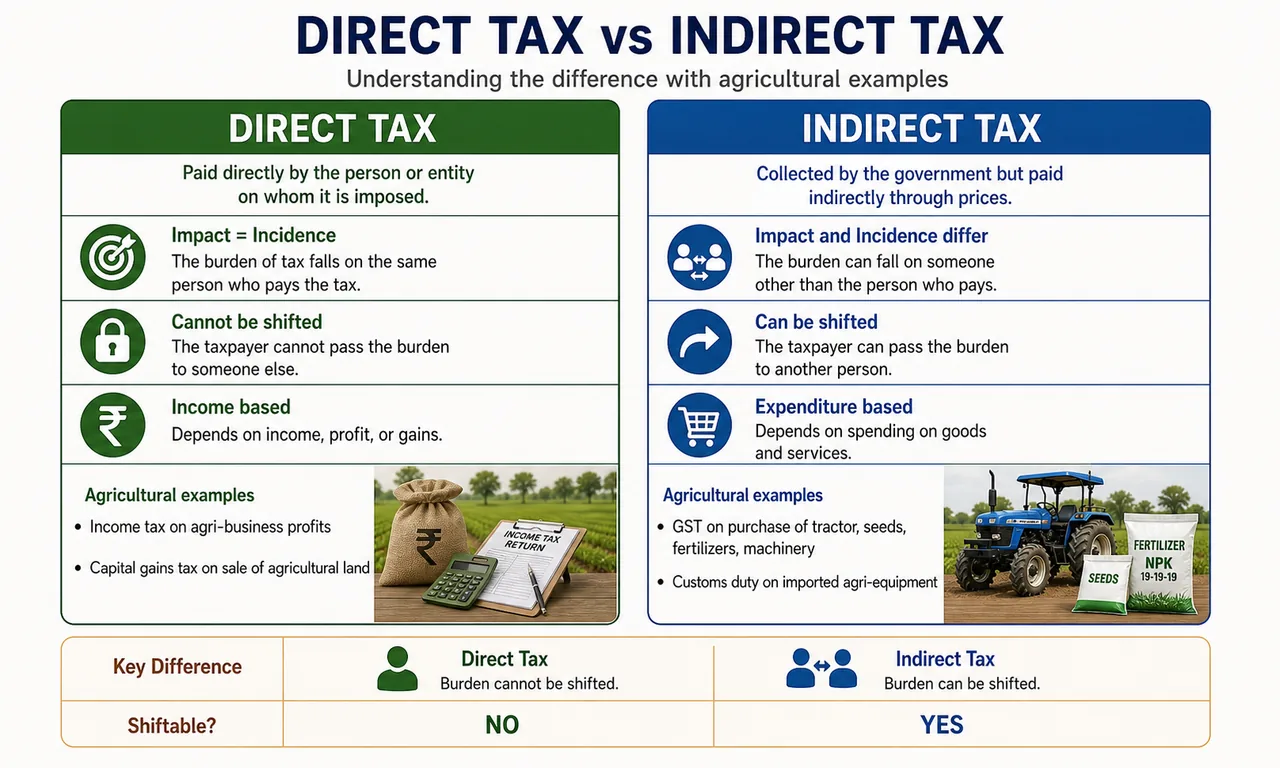

Direct Tax

A tax where the impact and incidence fall on the same person — the tax cannot be shifted to someone else.

- Paid on income levels

- Generally progressive and considered more equitable (based on ability to pay)

- Examples: Income tax, wealth tax, capital gains tax on sale of non-agricultural land

Indirect Tax

A tax where the impact and incidence fall on different persons. The seller pays the tax to the government (impact) but passes the burden to the consumer through higher prices (incidence).

- Paid on expenditure/outlay levels

- Examples: Sales tax, excise duty, customs duty, GST

| Feature | Direct Tax | Indirect Tax |

|---|---|---|

| Impact & Incidence | Same person | Different persons |

| Basis | Income | Expenditure |

| Shiftable? | No | Yes |

| Nature | Usually progressive | Often regressive |

| Agricultural example | Income tax on agri-business | GST on tractor purchase |

Key types of indirect tax:

- Excise Duty: Levied on manufacture, sale, or use of domestically produced goods (e.g., tobacco, alcohol). Charged at the point of production.

- Custom Duty: Levied on export and import of goods. Serves two purposes — raising revenue and protecting domestic industries (e.g., import duty on cheap foreign pulses to protect Indian dal farmers).

Exam Tip — Mnemonic: "Direct = Doesn't shift. Indirect = It shifts."

Agricultural Income — Tax Exemption

Agricultural income is exempt under the Indian Income Tax Act, 1961. The Constitution gives exclusive power to tax agricultural income to the State Legislature (not the Centre). Most states have chosen not to tax agricultural income to protect farmers' interests.

What Counts as Agricultural Income?

| Source | Example |

|---|---|

| Rent from agricultural land | Rent from land used for cultivation of crops, horticulture, or allied activities |

| Income from agricultural operations | Sale of crops, including basic processing — threshing, drying, cleaning, grading — to make produce market-ready |

| Income from a farm house | A farm house on or near agricultural land, used for agricultural purposes |

| Income from nursery operations | Growing and selling saplings, seedlings (clarified by Finance Act 2008) |

Partial Integration Method

Although agricultural income itself is not taxed by the Centre, there is an indirect method called partial integration of agricultural income with non-agricultural income:

- Agricultural income is added to non-agricultural income to determine the applicable tax slab

- Tax on agricultural income alone is then deducted

- This pushes non-agricultural income into a higher tax bracket

- Example: A farmer earns Rs. 3 lakhs from agriculture and Rs. 6 lakhs from a side business. The Rs. 6 lakhs is taxed as if total income were Rs. 9 lakhs, resulting in a higher rate on the non-agricultural portion.

Exam Tip: Remember — the Centre cannot tax agricultural income directly. Only State Legislatures have that power. This is a frequently asked constitutional provision.

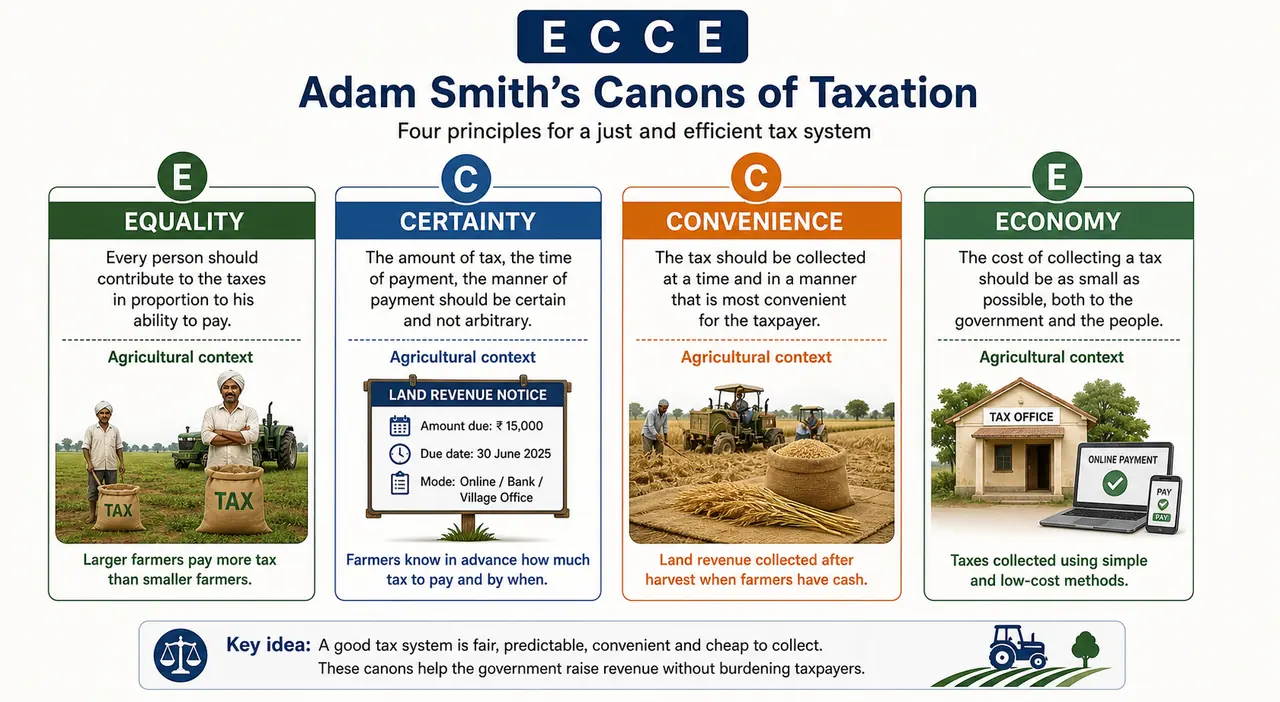

Canons of Taxation

Adam Smith's Original Canons (1776)

In "The Wealth of Nations", Adam Smith laid down fundamental principles for a good tax system. These remain the cornerstone of taxation theory.

Exam Tip — Mnemonic for Adam Smith's Canons: "ECCE" — Equality, Certainty, Convenience, Economy.

| Canon | Principle | Agricultural Example |

|---|---|---|

| Equality (Ability to Pay) | Tax in proportion to respective abilities — equal sacrifice, not equal amount | Progressive land revenue — large farmers pay more than marginal farmers |

| Sacrifice | Tax amount should match the taxpayer's capacity to bear the burden | A 5-acre farmer should not be taxed at the same rate as a 500-acre farmer |

| Certainty | Tax amount, time, and manner of payment must be clear — no ambiguity | Land revenue demand notice clearly stating amount, due date, and payment mode |

| Convenience | Tax collected at the time and manner most convenient for the taxpayer | Agricultural cess collected after harvest and marketing — when farmers have cash, not during lean season |

| Economy | Cost of collection should be a small fraction of revenue collected | Using digital payment for mandi cess instead of maintaining physical collection offices |

Additional Canons (by Later Economists)

| Canon | Principle | Agricultural Example |

|---|---|---|

| Fiscal Adequacy / Productivity | Tax system must generate sufficient revenue without discouraging economic activity | Agricultural cess should fund rural development without burdening small farmers so much that they abandon farming |

| Elasticity | Revenue should automatically increase as economy grows | As crop prices rise, ad valorem mandi tax generates more revenue without rate changes |

| Flexibility | Tax system should be adjustable to new conditions | Government waiving agricultural cess during drought years |

| Simplicity | Tax should be plain and intelligible to common people | A simple per-quintal levy at the mandi gate is easier for farmers to understand than a complex formula |

| Diversity | A wise mix of direct and indirect taxes — not too many, not too few | Combining land revenue (direct) with market cess (indirect) for stable agricultural revenue |

| Social & Economic Objectives | Tax should reduce inequality, accelerate growth, and ensure price stability | Progressive land tax that limits land concentration and funds rural employment schemes |

| Neutrality | Tax should not distort economic decisions | A uniform agricultural cess across crops so farmers choose crops based on soil suitability, not tax avoidance |

Exam Tip — Mnemonic for Additional Canons: "FE-FSDN" — Fiscal adequacy, Elasticity, Flexibility, Simplicity, Diversity, Neutrality (+ Social objectives).

Goods and Services Tax (GST)

GST is an indirect tax on the supply of goods and services — one of the most significant tax reforms in India's history. It replaced a complex web of multiple indirect taxes with a single, unified tax.

Key Features of GST

| Feature | Meaning |

|---|---|

| Comprehensive | Subsumed almost all indirect taxes (except a few state taxes) |

| Multi-staged | Imposed at every step in production, refunded at all stages except to the final consumer |

| Destination-based | Collected at the point of consumption, not origin — revenue goes to the consuming state |

GST Tax Slabs

| Slab | Type of Goods | Agricultural Relevance |

|---|---|---|

| 0% | Essential goods | Fresh vegetables, fruits, milk, cereals, fresh agricultural produce |

| 5% | Necessities | Fertilisers, organic manure, seeds, farm machinery parts |

| 12% | Standard goods | Processed food, ghee, fruit juices |

| 18% | Most goods | Tractors, pesticides, irrigation equipment |

| 28% | Luxury/demerit goods | Luxury vehicles, aerated drinks |

Special rates: 0.25% on rough precious stones; 3% on gold; additional cess on items like tobacco and luxury cars.

Not under GST: Petroleum products, alcoholic drinks, electricity (taxed separately by states).

Important Facts for Exams

- Effective date: 1 July 2017

- Constitutional basis: 101st Amendment — introduced Article 246A giving both Centre and States the power to levy GST

- Governing body: GST Council (finance ministers of Centre + all states) — reflects cooperative federalism

- Key outcome: Interstate travel time dropped by 20% due to removal of check posts

- Pre-GST statutory rate for most goods: ~26.5%. Post-GST: most goods in the 18% range

GST and Agriculture

Fresh agricultural produce is exempt from GST — vegetables, dairy, cereals, and unprocessed farm produce carry 0% GST. This is significant because it:

- Keeps fresh produce affordable for consumers

- Ensures the primary agricultural sector is not burdened by indirect taxes

- Supports farmer livelihoods by not adding tax to their basic output

Exam Tip: "Fresh and unprocessed = 0% GST. Processing begins = GST applies." This is a commonly tested distinction.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Public Revenue | All income and receipts collected by the government to finance expenditure on public goods, services, and welfare programmes |

| Major Revenue Sources | Taxes (compulsory, no direct benefit) and Prices (voluntary payment for a specific service) |

| Minor Revenue Sources | Fees, Special Assessment, Rates, Escheat, Grants, Gifts, Donations, Tributes & Indemnities |

| Tax vs Price | Tax = compulsory, no direct benefit; Price = voluntary, specific service received |

| Fee vs Tax | Fee = compulsory but gives a specific service in return (e.g., APMC market fee); Tax = for general welfare |

| Special Assessment | Levy on property owners who benefit from a specific public improvement (e.g., canal or road construction) |

| Rates | Levied by local bodies (panchayats, municipalities) for local services |

| Escheat | Property of a person who dies intestate with no legal heirs reverts to the State |

| Impact vs Incidence | Impact = person who initially pays; Incidence = person who ultimately bears the burden |

| Proportional Tax | Same rate/percentage for all incomes; simple but ignores ability to pay |

| Progressive Tax | Rate increases with income; based on LDMU of money; India's income tax is the prime example |

| Regressive Tax | Burden falls more heavily on the poor; most indirect taxes tend to be regressive |

| Degressive Tax | Progressive up to a limit, then uniform rate; fails to achieve full equity |

| Specific Tax | Fixed amount per unit regardless of price (e.g., Rs 5/quintal on wheat) |

| Ad Valorem Tax | Tax based on value of commodity ("according to value"); amount increases with price (e.g., stamp duty) |

| VAT | Tax on value added at each stage; avoids cascading effect (tax on tax) |

| Direct Tax | Impact and incidence on same person; cannot be shifted; usually progressive (e.g., income tax, wealth tax) |

| Indirect Tax | Impact and incidence on different persons; shifted from seller to consumer; often regressive (e.g., GST, excise, customs) |

| Excise Duty | Levied on manufacture/production of domestic goods |

| Custom Duty | Levied on import/export of goods; raises revenue and protects domestic industries |

| Agricultural Income Exemption | Exempt under Income Tax Act, 1961; only State Legislature can tax agricultural income (not Centre) |

| Partial Integration | Agri income added to non-agri income to determine tax slab; tax on agri income alone then deducted — pushes non-agri income into higher bracket |

| Adam Smith's Canons (ECCE) | Equality (ability to pay), Certainty (clear amount/time), Convenience (easy payment timing), Economy (low collection cost) — from Wealth of Nations (1776) |

| Additional Canons (FE-FSDN) | Fiscal Adequacy, Elasticity, Flexibility, Simplicity, Diversity, Neutrality + Social objectives |

| GST | Indirect tax on supply of goods/services; comprehensive, multi-staged, destination-based; replaced multiple indirect taxes |

| GST Key Facts | Effective 1 July 2017; 101st Constitutional Amendment; introduced Article 246A; governed by GST Council (cooperative federalism) |

| GST Slabs | 0% (fresh produce, milk, cereals), 5% (fertilisers, seeds), 12% (processed food), 18% (tractors, pesticides), 28% (luxury goods) |

| GST & Agriculture | Fresh agricultural produce exempt (0% GST); processing begins = GST applies |

| Not under GST | Petroleum products, alcoholic drinks, electricity (taxed separately by states) |