📊 RAROC, RARORAC, RORWA & Risk Weighted Assets

Complete guide to Risk Adjusted Return on Capital (RAROC), RORAC, RARORAC, RORWA, Risk Weighted Assets, MCLR, external benchmarks, and RWA norms for banking exams.

Introduction

Lending rates, reflecting the cost of credit, significantly impact economic activity:

- Lower interest rates tend to stimulate economic growth, while higher rates can dampen spending and investment.

- Fair pricing affects the profitability aspects of a bank, including capital adequacy, asset quality, management efficiency, earnings, and liquidity.

- Policymakers focus on improving the transmission of monetary policy through interest rate channels.

- Initially, the banking industry, following the 2007-2008 financial crisis, acknowledged the importance of risk-adjusted pricing for sustainable profitability.

Importance of Risk Adjusted Return on Capital

- Fair pricing of credit is crucial for both banks and borrowers, directly impacting growth and savings.

- Pricing within a generous perspective returns to the lender considering Return on Equity (ROE) and Return on Assets (ROA).

- Loan pricing affects the profitability aspects of a bank, including capital adequacy, asset quality, management efficiency, earnings, and liquidity.

- Pricing decisions are influenced by the minimum desired profitability and the inherent risk in a transaction.

- For customer relationships with high profit potential, pricing may be adjusted to break-even levels temporarily.

- RBI introduced the use of external benchmarks for credit pricing, with banks determining their own spread adjustments.

- Spread adjustments may occur based on credit risk charges and operating costs at periodic intervals.

- Pricing of floating rate loans involves adding a spread to the benchmark rate, influenced by competition, credit risk, and business strategy.

- Additional factors like competition, customer relationships, and business strategy also influence the final lending rate.

- Parameters such as future business potential, relationship value, and business strategy are additional factors in determining lending rates beyond risk-based pricing.

- Price discrimination among customers is not acceptable within banking regulatory frameworks, regardless of the pricing method used.

- Base rate remains stable despite policy rate changes, as it's based on historical costs of funds.

- Pricing differences may occur due to factors like competition, credit risk, and the cost of funds, reflecting different risk profiles and market conditions.

- The financial market must avoid discriminatory pricing in credit to gain market share or win business.

- Pricing adjustments also consider the regulatory and compliance framework.

MCLR (Marginal Cost of Funds Based Lending Rate)

- The Marginal Cost of Funds Based Lending Rate (MCLR) was introduced in April 2016 to help borrowers realise various benefits (including home loans) from the Reserve Bank of India's (RBI) rate cut (Repo Rate).

- It replaced the base rate structure.

- This new rate system ensures that your lender cannot charge you interest rates beyond the margin prescribed by RBI.

- MCLR is the minimum interest rate that a bank can lend at. Under the MCLR regime, banks are free to offer all categories of loans on fixed or floating interest rates.

- At actual lending rates for loans of different categories and tenures are determined by adding the components of spread to MCLR.

- MCLR is a tenor-linked internal benchmark, which means the rate is determined internally by the bank depending on the period left for the repayment of a loan.

Four Major Elements of MCLR

- Tenor Premium

- Marginal Cost of Funds

- Negative Carry on CRR

- Operating Cost

Key Points about MCLR

- It is the premium charged by the banks for the risk associated with lending the higher-duration loans.

- Tenor is the amount of time left for repayment of the loan.

- Higher the duration of the loan, higher will be the risk. In order to cover the risk, the bank will shift the load to the borrowers by charging an amount in the form of premium.

- Tenor premium is not specific to a loan class or borrower, but is uniform across all types of loans.

- Banks incur various expenses for raising funds, opening branches, paying salaries and so on.

- All operating costs associated with providing loan products are included except recovery expenses.

- However, cost of providing services, which are recovered by way of service charges, are not included.

External Benchmark Linked Lending Rate (EBLR)

An Internal Study Group of RBI recommended the move over to an External Benchmark based Lending rate system from MCLR.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Introduction

Lending rates, reflecting the cost of credit, significantly impact economic activity:

- Lower interest rates tend to stimulate economic growth, while higher rates can dampen spending and investment.

- Fair pricing affects the profitability aspects of a bank, including capital adequacy, asset quality, management efficiency, earnings, and liquidity.

- Policymakers focus on improving the transmission of monetary policy through interest rate channels.

- Initially, the banking industry, following the 2007-2008 financial crisis, acknowledged the importance of risk-adjusted pricing for sustainable profitability.

Importance of Risk Adjusted Return on Capital

- Fair pricing of credit is crucial for both banks and borrowers, directly impacting growth and savings.

- Pricing within a generous perspective returns to the lender considering Return on Equity (ROE) and Return on Assets (ROA).

- Loan pricing affects the profitability aspects of a bank, including capital adequacy, asset quality, management efficiency, earnings, and liquidity.

- Pricing decisions are influenced by the minimum desired profitability and the inherent risk in a transaction.

- For customer relationships with high profit potential, pricing may be adjusted to break-even levels temporarily.

- RBI introduced the use of external benchmarks for credit pricing, with banks determining their own spread adjustments.

- Spread adjustments may occur based on credit risk charges and operating costs at periodic intervals.

- Pricing of floating rate loans involves adding a spread to the benchmark rate, influenced by competition, credit risk, and business strategy.

- Additional factors like competition, customer relationships, and business strategy also influence the final lending rate.

- Parameters such as future business potential, relationship value, and business strategy are additional factors in determining lending rates beyond risk-based pricing.

- Price discrimination among customers is not acceptable within banking regulatory frameworks, regardless of the pricing method used.

- Base rate remains stable despite policy rate changes, as it's based on historical costs of funds.

- Pricing differences may occur due to factors like competition, credit risk, and the cost of funds, reflecting different risk profiles and market conditions.

- The financial market must avoid discriminatory pricing in credit to gain market share or win business.

- Pricing adjustments also consider the regulatory and compliance framework.

MCLR (Marginal Cost of Funds Based Lending Rate)

- The Marginal Cost of Funds Based Lending Rate (MCLR) was introduced in April 2016 to help borrowers realise various benefits (including home loans) from the Reserve Bank of India's (RBI) rate cut (Repo Rate).

- It replaced the base rate structure.

- This new rate system ensures that your lender cannot charge you interest rates beyond the margin prescribed by RBI.

- MCLR is the minimum interest rate that a bank can lend at. Under the MCLR regime, banks are free to offer all categories of loans on fixed or floating interest rates.

- At actual lending rates for loans of different categories and tenures are determined by adding the components of spread to MCLR.

- MCLR is a tenor-linked internal benchmark, which means the rate is determined internally by the bank depending on the period left for the repayment of a loan.

Four Major Elements of MCLR

- Tenor Premium

- Marginal Cost of Funds

- Negative Carry on CRR

- Operating Cost

Key Points about MCLR

- It is the premium charged by the banks for the risk associated with lending the higher-duration loans.

- Tenor is the amount of time left for repayment of the loan.

- Higher the duration of the loan, higher will be the risk. In order to cover the risk, the bank will shift the load to the borrowers by charging an amount in the form of premium.

- Tenor premium is not specific to a loan class or borrower, but is uniform across all types of loans.

- Banks incur various expenses for raising funds, opening branches, paying salaries and so on.

- All operating costs associated with providing loan products are included except recovery expenses.

- However, cost of providing services, which are recovered by way of service charges, are not included.

External Benchmark Linked Lending Rate (EBLR)

An Internal Study Group of RBI recommended the move over to an External Benchmark based Lending rate system from MCLR.

- 1 April 2019: RBI mandated that all new floating rate personal or retail loans (housing, auto, etc.) and floating rate loans to MSMEs to an External Benchmark from MCLR.

- Banks are free to choose one of the several benchmarks:

- RBI's Repo Rate (most popular)

- Government of India 3-Months Treasury Bill published by the FBIL

- Government of India 6-Months Treasury Bill published by the FBIL

- Any other benchmark market interest rate published by the FBIL

Key Rules

- Banks are free to select any external benchmark linked loans to other types of borrowers as well.

- For transparency, standardisation, and ease of understanding of loan products by borrowers, a bank must adopt a uniform external benchmark within a loan category. In other words, the adoption of multiple benchmarks by the same bank is not allowed within a loan category.

- Banks are free to decide the spread over the external benchmark. However, credit risk premium may undergo change only when borrower's credit assessment undergoes a substantial change, as agreed upon in the loan contract.

- Further, other components of spread including operating cost could be altered once in three years.

- The interest rate under external benchmark shall be reset at least once in every 3 months.

- Existing loans and credit limits linked to the MCLR/Base Rate/BPLR shall continue till repayment or renewal, as the case may be.

- When the floating rate advances are linked to an internal benchmark rate, banks shall determine their actual lending rates by adding the components of spread to the internal benchmark rate.

- Interest rates on fixed rate loans of tenor below 3 years shall not be less than the benchmark rate for similar tenor.

EBLR vs MCLR

- EBLR is one of the External Benchmark linked lending rate and now widely adopted by various banks. This is directly linked with RBI's Repo rate.

- EBLR = Repo rate + Margin charged by the bank

- The transmission rate is faster in EBLR, as the Repo rate is revised immediately a customer is benefited out of it.

- As it is linked to Repo rate hence it is revised in every 3 months.

- MCLR is primarily an internal benchmark of the bank as its own cost of funds will determine the MCLR of the bank.

- However, in the case of EBLR which is externally linked, the bank's own cost of funds does not have a direct impact when the repo rate goes up or comes down.

Theory of Interplay Between Return, Capital and Risk

- The concept was introduced by Dan Borge, a corporate designer at Bankers Trust, in the late 1970s.

- Bankers Trust engaged in ambitious and risky fixed-income trading of products and derivatives, resulting in the development of RAROC.

- Other banks followed suit, developing their own versions such as RORAC and RARORAC.

- Despite variations, RAROC remains the most widely accepted and referenced.

- Risk pricing models are built on three key elements: return, capital, and risk.

Risk-Adjusted Performance Measures (RAPMs)

- RAPMs aim to improve traditional evaluation methods for business units or portfolios by accounting for associated risk factors.

- They enable comparison of risk-adjusted profitability and performance across different centres for similar industries or variations in implementation.

- Despite similarities, different RAPMs vary in their approach, user base, and institutional preferences.

- Micro analysis reveals variations in the unit, user, and destination of different RAPMs.

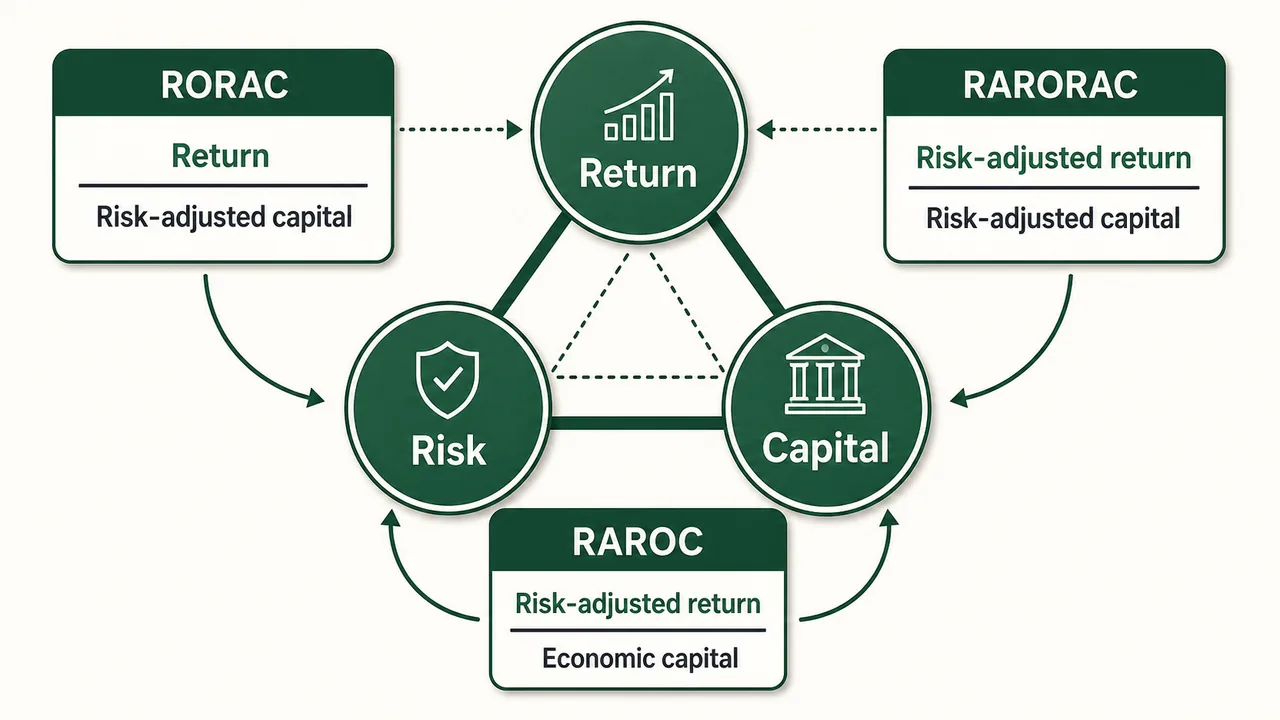

RORAC (Return on Risk Adjusted Capital)

- Return On Risk Adjusted Capital (RORAC) is a profitability metric used in assessing the profitability of a project or investment relative to the risk-adjusted capital employed.

- RORAC allows for easier comparison of projects with different risk profiles by providing a unified measure of return per unit of risk.

- Unlike Internal Rate of Return (IRR), RORAC accounts for risk in its calculation.

- RORAC = Operating Profit / Risk Capital

- RORAC is typically applied to long-term projects with significant capital investment, where the risk is well-defined and quantifiable.

- RORAC adjusts the denominator (capital) to reflect the risk of a project, making it a refined metric that accounts for risk.

RARORAC (Risk Adjusted Return on Risk Adjusted Capital)

- RARORAC adjusts both the numerator (return) and the denominator (capital) to account for risk, making it a comprehensive profitability metric.

- RARORAC blends RORAC and RAROC by accounting for both risk-adjusted profitability and risk capital allocation.

- It supports capital allocation among different business lines or investment alternatives to achieve optimal equity-to-assets proportions.

- RARORAC facilitates cost-benefit analysis of ventures based on their risk influence and target returns.

- It serves as a benchmark for comparing performance perspectives across different risk categories.

- According to Prof. Dr. Hans Peter Burger of University of Innsbruck: RARORAC is the Profit – (Rate of risk capital costs × Risk Capital) / Risk Capital

- RARORAC measures productivity in value creation relative to risk by considering both risk-adjusted profitability and risk capital allocation.

- Primary objective: to measure productivity in value creation relative to risk.

RAROC (Risk Adjusted Return on Capital)

- Western's banking developed an increased interest in 2012, promoting RAROC in overall regulatory compliance.

- This model, known as RAROC, features risk measures from basic adjusted-risk, compounded returns with variations in its risk-adjusting methodology.

- Regulatory parameters include credit, operational risk, and market risk components, although the approach may vary among institutions.

- RAROC measures the value-producing capacity of assets or businesses as a ratio, allowing comparisons between assets of different sizes and risk levels.

- It considers observable asset prices and volatility to determine the capital to be held, following a mark-to-market concept.

- RAROC allocates capital based on the maximum expected loss over one year at a 99% confidence level, considering credit, market, and other risks.

- It estimates the asset value in the worst-case scenario and sets the capital cushion accordingly.

- RAROC enables comparison between businesses with different risk profiles by assessing their risk-return trade-offs.

- Lenders can use RAROC to set target pricing based on expected rates of return, considering the risk involved.

- While not all assets have market price distribution, RAROC serves as a starting point to evaluate an institution's entire balance sheet on a mark-to-market basis.

- Primary objective of RAROC: to measure the risk-adjusted profitability of a product or portfolio.

RBI Working Group on RAROC

The RBI WG (chaired by Shri Anand Sinha) suggested two options for pricing of credit: RAROC or alternatively RORAC. The WG defined RORAC as:

(Loan price − cost of funds) × volume + income from credit products + fees − operating expenses / Risk Adjusted Capital

In effect: RORAC = Operating Profit / Risk Capital

The RAROC was defined by the RBI WG as: Risk Adjusted Return / Economic Capital

RAROC Formula (Anthony Saunders & Linda Allen)

- Obviously, the WG formula had Risk Adjusted Return at the numerator and Economic Capital at the denominator. These were the most discussed and most confused ones in working model.

- Anthony Saunders and Linda Allen, in their book "Credit Risk Measurement — New Approaches to Value at Risk and Other Paradigms" made a deeper insight:

- Numerator = Adjusted Income = (Spread + Fees − Operating Costs) × (1 − Marginal Tax Rate)

- Denominator = Duration of the Loan × Risk Amount or loan exposure × Expected discount (change in the credit premium or risk factor on the loan × Capital at Risk or Economic Capital)

SBI Formula

Like the franchises of Anthony Saunders and Linda Allen, SBI, the largest lender of the country developed the following formula for RAROC:

RAROC = (Interest Income + Processing Fee + Insurance Income − Interest Expenditure − Provision − Expected Loss − Operating Expenses) / (Credit Risk Capital + Operational Risk Capital)

Where:

- Credit risk capital = Average Utilisation × CCF (%) × Risk weight (%) × CRAR (%)

Application of RAROC

- Risk pricing is fundamental in risk management, where borrowers with data-proven risk perspectives are segregated as high risk should be priced accordingly.

- Banks must develop logical methods to price credit risk, considering the estimated probability of default, loss given default, and exposure at default.

- Pricing of loans should be linked to the rating of a credit quality, taking into account prospective risk factors such as future business potential and relationship value.

- A proper model should be established for working prices based on changes in economic conditions and business factors.

- Inconsistencies have compounded RAROC structures for loan pricing, requiring standardised risk-adjusted approaches.

- Under the RAROC framework, banks charge an interest margin to cover expected credit losses, operating costs, and a return commensurate with the risk.

- Pricing should be streamlined, but fails for increased business without delivering fair risk-adjusted returns.

- A holistic RAROC framework should give due consideration to improving risk detection.

- Loans should only be made if the RAROC exceeds the bank's hurdle rate.

- RAROC enables capital allocation among different business lines or investment alternatives to achieve optimal equity-to-assets proportions.

- Factors considered in the application of RAROC: future business potential and portfolio exposure.

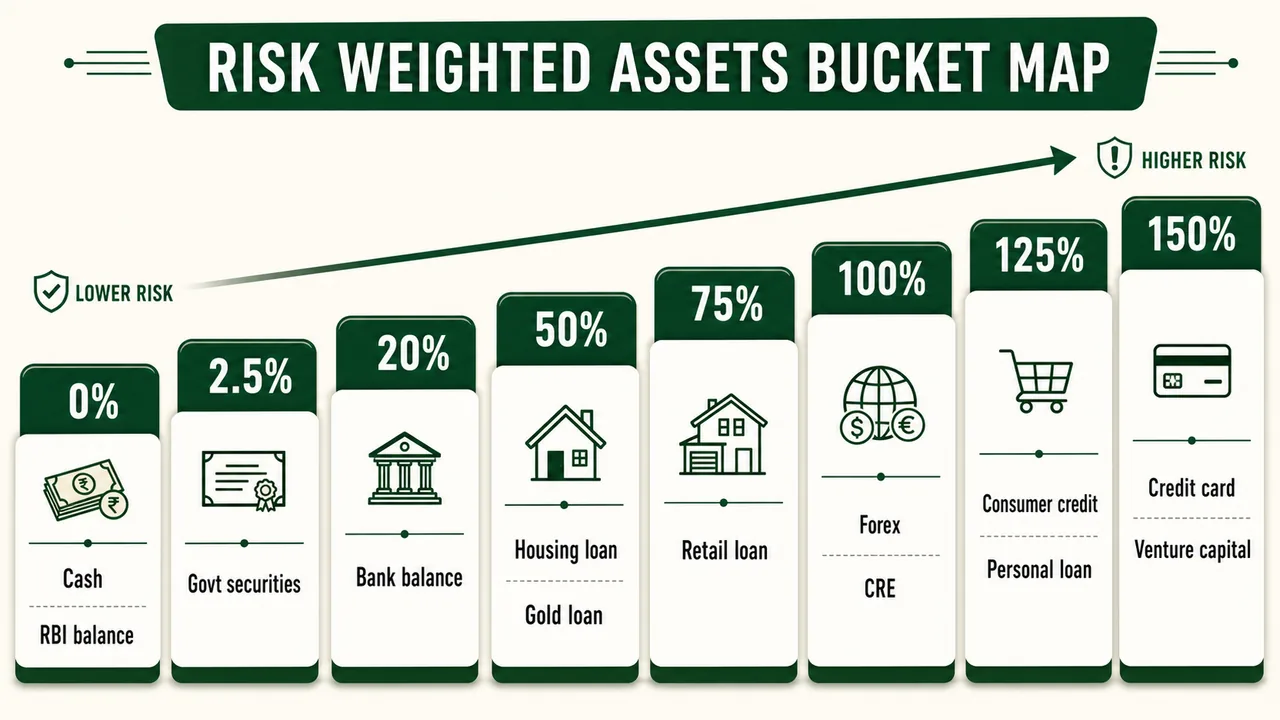

Risk Weighted Assets (RWA)

Each asset of a bank is assigned with a risk weight.

- Definition: RWA represents the assets of a bank weighted by credit risk, market risk, and operational risk.

- Purpose: To determine the minimum capital required to protect against the risks of its investments.

- Calculation: Each asset is assigned a risk weight percentage, which determines the effective capital requirement.

- Regulatory Requirement: Banks must maintain minimum Capital to Risk-Weighted Assets Ratio (CRAR) against their RWAs.

New RWA Norms

RBI changed the RWA norms on 16th November 2023.

| Assets | Risk Weight |

|---|---|

| Cash, Balance with RBI, Govt/CGF guaranteed advances up to guaranteed amount, Loan against FD/LIC | 0% |

| Government approved Securities | 2.5% |

| Balance with Banks other than RBI which maintain 9% CRAR, Secured Loan to staff | 20% |

| Housing Loans, Gold Loan, Loan Guaranteed by ECGC | 50% |

| House loan above 75L, Retail Loan up to 5 Cr | 75% |

| Forex, Loan to PSU, Commercial Real Estate, Educational loan | 100% |

| Consumer Credit, Personal Loans, Capital Market Exposure | 125% |

| Credit Card & Investment in Venture Capital | 150% |

Changes in Risk Weights (November 2023)

| Category | Existing Risk Weight | Increased Risk Weight |

|---|---|---|

| Commercial Banks (Consumer Credit) | 100% | 125% |

| NBFCs (Consumer Credit) | 100% | 125% |

| SCBs (Credit Card Receivables) | 125% | 150% |

| NBFCs (Credit Card Receivables) | 100% | 125% |

| SCBs (Bank Credit to NBFCs) | As per external rating | +25% if below 100% |

Key RWA Concepts

- Average utilisation considers the higher value between the average outstanding balance at each quarter end or the outstanding balance at the year end, adjusted for eligible financial collaterals.

- The Capital to Risk Weighted Assets Ratio (CRAR %) represents the minimum regulatory requirement.

- Operational risk capital is set at 15% of gross income, calculated as interest income minus interest expenses plus non-interest income.

- Credit Conversion Factor (CCF) determines the credit risk exposure by multiplying the face value of each item by specific percentages (0.5 CC and 1 CC). Non-fund based items like guarantees typically carry a CCF of 15%. Undrawn portions of certain credit facilities attract different CCF percentages.

Risk Weight Determination

- Risk weights are determined based on long-term ratings by External Credit Assessment Institutions (ECAIs), with variations for foreign entities and foreign rating agencies.

- All unrated claims attract a risk weight of 100%.

- Bank exposures exceeding INR 200 crore from the banking system will attract a risk weight of 150%.

- Exposures exceeding INR 100 crore, previously rated but now unrated, also attract a risk weight of 150%.

- Risk weights for real estate exposure vary based on size and sector, impacted at the rating.

Guarantees and Risk Weights

In addition to the above sovereign guarantees, credit guarantee cover and underlying also impacts risk weight as follows:

| Type of Guarantee | Risk Weight (%) |

|---|---|

| Central Govt. Guarantee | 0 |

| State Govt. Guarantee | 20 |

| CGTMSE covered | 0 |

| NPA (loss discovered) CC | 0 |

RORWA (Return on Risk Weighted Assets)

- RORWA measures a lender's net earnings on different risk-weighted assets.

- It indicates the risk-weighted profitability of a product, portfolio, unit, or institution.

- RORWA adjusts Return On Assets (RoA) to reflect the risks involved in generating those returns.

- RoA is the net income expressed as a percentage of total assets.

- RORWA considers the risks taken to achieve returns, providing a more accurate measure of profitability.

- RORWA = (Net Income / Risk Weighted Assets) × 100

Application of RORWA

- RORWA can be calculated for individual products, portfolios, units, clusters, or regions.

- If the RORWA of a specific unit is lower than the bank's RORWA, it indicates underperformance.

- Underperformance means that returns from other units are compensating for inefficiencies in that unit.

- Banks can use RORWA to compare their performance with industry benchmarks.

- This comparison helps banks identify if they are underperforming or outperforming the broader market.

- The goal is to achieve higher profitability and risk-adjusted returns compared to industry standards.

- The denominator in RORWA calculation is Risk Weighted Assets.

Quick Notes for Exam

- RAROC measures the risk-adjusted profitability of a product or portfolio — NOT capital adequacy or liquidity risk.

- RAPMs aim to improve traditional evaluation methods by accounting for associated risk factors with business units or portfolios.

- RORAC adjusts the denominator (risk capital) to reflect the risk of a project.

- RARORAC assists in capital allocation among different business lines or investment alternatives to achieve optimal equity-to-assets proportions.

- RARORAC measures productivity in value creation relative to risk by considering both risk-adjusted profitability and risk capital allocation.

- RORWA measures risk-adjusted profitability of a product or portfolio — denominator is Risk Weighted Assets.

- Risk Weighted Assets is used as the denominator in RORWA calculation.

- How RORAC differs from RAROC: RORAC adjusts the rate of return for risk, while RAROC adjusts the capital for risk.

- How RAROC differs from RARORAC: RAROC adjusts capital for risk, while RORAC adjusts returns for risk; RARORAC adjusts both.

- How RAROC differs from RORAC: RAROC adjusts returns for risk, while RORAC focuses on market risk.

- RAROC formula (Saunders & Allen): Spread + Fees − Operating Costs / Duration of Loan × Risk Amount.

- Loan guaranteed by State Government does NOT attract 0% risk weight — it attracts 20%.

- Consumer credit including personal loans attracts 125% risk weight.

- The goal of RAPMs: to improve traditional evaluation methods by accounting for risk factors.

- RBI WG on credit pricing was chaired by Shri Anand Sinha — recommended transparent credit pricing policies.

- RORWA's primary objective is to measure the risk-adjusted profitability of a product or portfolio.

- RAROC model was developed by Bankers Trust (Dan Borge) in the late 1970s.

- MCLR four elements: Tenor Premium, Marginal Cost of Funds, Negative Carry on CRR, Operating Cost.

- EBLR is reset at least once in every 3 months.

- EBLR = Repo rate + Margin charged by bank.

- Factors in RAROC application: future business potential and portfolio exposure.

Cheat Sheet

| # | Topic | Key Point |

|---|---|---|

| 1 | RAROC Origin | Developed by Bankers Trust (Dan Borge) in late 1970s |

| 2 | RAROC Purpose | Measure risk-adjusted profitability of product/portfolio |

| 3 | RAROC Formula (RBI WG) | Risk Adjusted Return / Economic Capital |

| 4 | RORAC Formula | Operating Profit / Risk Capital |

| 5 | RORAC Adjusts | Denominator (capital) for risk |

| 6 | RARORAC | Adjusts BOTH numerator (return) and denominator (capital) |

| 7 | RARORAC Measures | Productivity in value creation relative to risk |

| 8 | RORWA Formula | (Net Income / Risk Weighted Assets) × 100 |

| 9 | RORWA Denominator | Risk Weighted Assets |

| 10 | RAPMs Purpose | Improve traditional evaluation by accounting for risk |

| 11 | RBI WG Chair | Shri Anand Sinha |

| 12 | RBI WG Options | RAROC or alternatively RORAC for credit pricing |

| 13 | SBI RAROC | (Income − Expenses − Provision − EL − OpEx) / (Credit + Op Risk Capital) |

| 14 | MCLR Introduced | April 2016 |

| 15 | MCLR Replaced | Base rate structure |

| 16 | MCLR Nature | Minimum interest rate, tenor-linked internal benchmark |

| 17 | MCLR Elements | Tenor Premium, Marginal Cost of Funds, Negative Carry on CRR, Operating Cost |

| 18 | Tenor Premium | Uniform across all loan types, not borrower-specific |

| 19 | Operating Cost | Excludes recovery expenses and service charge income |

| 20 | EBLR Mandate | 1 April 2019 for personal/retail and MSME floating rate loans |

| 21 | EBLR Benchmark | Most common: RBI Repo Rate |

| 22 | EBLR Formula | Repo rate + Margin charged by bank |

| 23 | EBLR Reset | At least once every 3 months |

| 24 | Multiple Benchmarks | Not allowed within a loan category for same bank |

| 25 | Spread Change | Operating cost component can be altered once in 3 years |

| 26 | Fixed Rate Loans | Tenor below 3 years — rate not less than benchmark |

| 27 | Price Discrimination | Not acceptable within banking regulatory framework |

| 28 | Risk Pricing Elements | Return, Capital, and Risk |

| 29 | RAROC Confidence | 99% confidence level for max expected loss over 1 year |

| 30 | RAROC Hurdle Rate | Loans should only be made if RAROC exceeds hurdle rate |

| 31 | RWA Definition | Assets weighted by credit, market, and operational risk |

| 32 | RWA Norms Changed | 16th November 2023 |

| 33 | RW: Cash/RBI/Govt Gtd | 0% |

| 34 | RW: Govt Securities | 2.5% |

| 35 | RW: Banks (9% CRAR) | 20% |

| 36 | RW: Housing/Gold/ECGC | 50% |

| 37 | RW: Retail up to 5 Cr | 75% |

| 38 | RW: Forex/PSU/CRE/Edu | 100% |

| 39 | RW: Consumer/Personal | 125% |

| 40 | RW: Credit Card/VC | 150% |

| 41 | Unrated Claims RW | 100% |

| 42 | SCB Credit Card RW | Increased from 125% to 150% |

| 43 | NBFC Consumer Credit | Increased from 100% to 125% |

| 44 | CRAR | Capital to Risk Weighted Assets Ratio |

| 45 | Op Risk Capital | 15% of gross income |

| 46 | Non-fund CCF | Guarantees typically 15% |

| 47 | Central Govt Guarantee | 0% risk weight |

| 48 | State Govt Guarantee | 20% risk weight |

| 49 | CGTMSE Covered | 0% risk weight |

| 50 | Exposures >200 Cr | 150% risk weight from banking system |

| 51 | ECAI | External Credit Assessment Institutions for ratings |

| 52 | Mark-to-Market | RAROC follows this concept for capital determination |

Lesson Doubts

Ask questions, get expert answers